#19 H&M - Fashion made in Sweden

#19 H&M - Fashion made in Sweden

Why H&M is an interesting investment case

Dear readers,

thank you for being here and for your interest in my work! If you like this article, if you find this stock watchlist and my deep dives valuable, and if you want to support my work, please feel free to subscribe!

Please read the disclaimer at the end of this article. This is not investment advice!

Thank you for taking the time to read my article. Recent weeks have been particularly hectic at work, limiting the time I could dedicate to writing. However, I'm optimistic that I'll be able to devote more attention to it shortly. This piece focuses on H&M, the prominent fashion conglomerate from Sweden. I've been an investor in this stock for the past year and have been closely monitoring its progress. Despite facing significant challenges, the company harbors considerable potential for margin growth and, consequently, an expansion in its valuation. Let's delve deeper into this intriguing investment opportunity.

About H&M

H&M Hennes & Mauritz AB (publ), headquartered in Stockholm, Sweden, is a global retailer offering a wide range of products for women, men, teenagers, children, and babies. Founded in 1947, the company's portfolio includes clothing, accessories, footwear, cosmetics, home textiles, and homeware. Its diverse product line extends to sportswear, shoes, bags, beauty products, ready-to-wear apparel, and interior products like bed linens, dinnerware, textiles, furniture, and lighting. H&M operates under several brand names, including H&M, H&M HOME, H&M Move, COS, Weekday, Monki, & Other Stories, ARKET, Afound, Singular Society, Creator Studio, and Sellpy, catering to a broad spectrum of consumer needs and preferences worldwide.

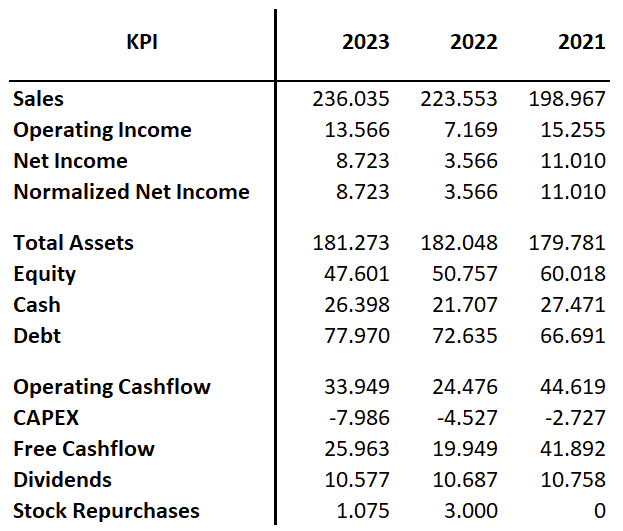

In 2023, H&M achieved total sales of 236 billion SEK (approximately 22.4 billion USD), with an operating income of 8.7 billion SEK. Notably, H&M demonstrated robust cash flow performance, generating 34 billion SEK in operating cash flow and 26 billion SEK in free cash flow, culminating in a free cash flow (FCF) margin of 11%. Below is a table detailing the key financial metrics from the income statement, balance sheet, and cash flow statement over the past three years.

Why H&M is an interesting investment case

Margin sacrificed for growth

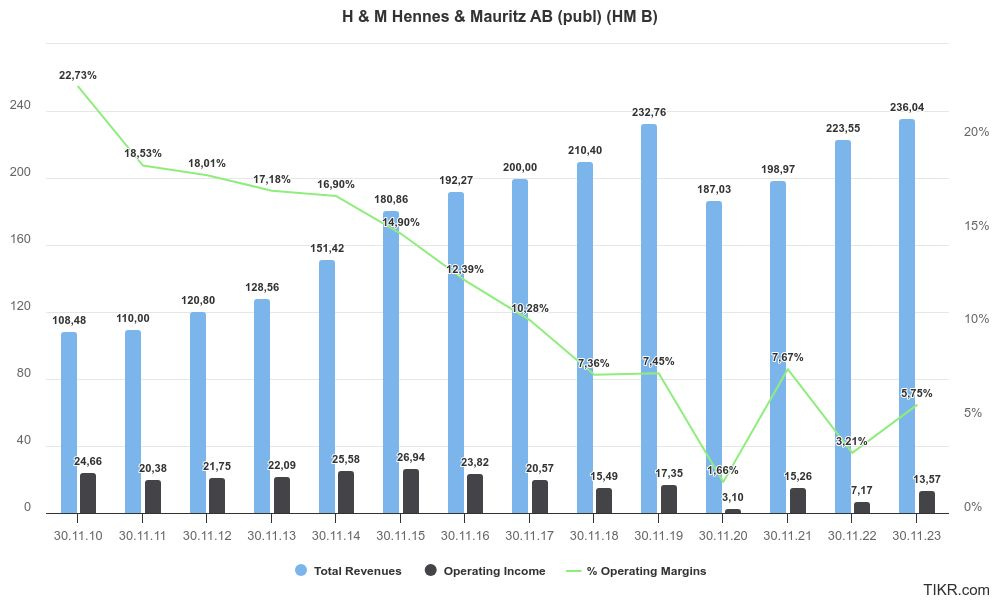

Between 2010 and 2019, preceding the pandemic, H&M Group experienced a Compound Annual Growth Rate (CAGR) in revenue of 8.9%. This growth, however, came at a cost to operating income, which, while relatively stable until 2015, began a downward trajectory thereafter. More notably, the operating margin has been on a consistent decline since 2010, halving by 2016 and continuing to decrease to approximately 7.4%, with the current figure at about 5.8%. Efforts to elevate the margin back to above 10% have so far been unsuccessful.

In response to these challenges, H&M's management has implemented a strategy of reducing store counts and enhancing their omnichannel approach. Despite the intense competition and the significant global challenges that emerged in 2020, placing the world in a state of crisis, H&M is striving to maintain and grow its market share and profitability. Acknowledging past missteps, the company is now focused on a turnaround strategy, learning from previous experiences to navigate the complex retail landscape.

Strong Brands

The H&M Group boasts a diverse portfolio of brands, each with a distinct identity and target market. Here's an overview of their main brands and their standing:

H&M: The flagship brand is known for its fast-fashion offerings, targeting a wide demographic with a range of trendy, budget-friendly clothing and accessories. H&M has a strong global presence with stores in numerous countries, and it's known for its collaborations with high-end designers and celebrities, which have bolstered its profile.

COS (Collection of Style): Positioned as a higher-end brand within the group, COS offers timeless, high-quality fashion items at a slightly higher price point. It appeals to a more fashion-conscious consumer who values minimalistic and modern design.

& Other Stories: Launched in 2013, & Other Stories provides women's apparel, shoes, bags, accessories, and beauty products. It caters to women looking for a more upscale and detailed fashion statement compared to the main H&M line, often drawing inspiration from high-fashion trends.

Weekday: This brand is known for its Scandinavian-inspired, fashion-forward clothing that resonates with young and conscious consumers. Weekday has a strong emphasis on sustainability and often features progressive designs.

Monki: A youth-oriented brand, Monki delivers a playful and vibrant fashion statement. It's characterized by its bold patterns and colors, targeting young women who want to express their individuality through their clothing.

ARKET: Launched in 2017, ARKET provides essentials for men, women, children, and the home. The brand focuses on sustainability, quality, and timeless design, aiming for a more premium segment of the market.

Afound: This brand operates as an off-price marketplace offering deals on fashion and lifestyle products from well-known and popular brands. It's part of H&M Group's strategy to enter the discount retail space and appeal to value-conscious consumers.

Singular Society: A newer addition to the H&M family, Singular Society offers a membership-based model where members can buy products at the price they cost to make. It's a unique approach in the retail space, emphasizing transparency and quality.

Sellpy: Although not a traditional retail brand, Sellpy, which H&M has invested in, is an online second-hand shop that aligns with the group's sustainability efforts. It allows consumers to buy and sell used H&M clothing, promoting a circular fashion industry.

Each brand under the H&M Group umbrella serves a specific market niche and contributes to the group's overall standing as a leader in the global fashion industry. The group's strategic positioning of its brands allows it to cater to a broad spectrum of consumers and adapt to shifting market trends. While H&M remains the powerhouse driving revenue, the other brands support the group's market diversification and help in targeting specific consumer segments more effectively. This multi-brand strategy has helped the H&M Group maintain a strong market position despite the highly competitive nature of the fashion retail industry.

Strategic approach

The H&M Group is strategically expanding through integrated channels to enhance omnichannel sales, recognizing customer preferences for shopping across various platforms, including in-store, online on brand websites, digital marketplaces, and social media. In 2024, the company plans to accelerate investment in its existing stores to offer a more inspiring shopping experience while ensuring its store portfolio remains profitable and growth-oriented.

Key expansions in 2023 included entering Albania as a new store market and launching online operations in Ecuador and Vietnam. Collaborations and launches on digital marketplaces like Superbalist.com in South Africa, JD.com, and Namshi.com were part of its strategy to increase its digital footprint.

Brand-specific expansions included Arket opening its first stores in Estonia, Switzerland, and Latvia; COS entering the Mexican market with a flagship store; and & Other Stories debuting in Switzerland. Both & Other Stories and COS expanded their online presence in Australia and New Zealand through Iconic.com. Monki extended its reach on Zalora.com to Hong Kong.

Looking ahead to 2024, Arket plans to open its first stores in Spain, Italy, and Poland. H&M Group is actively renegotiating a significant number of leases, which involves store rebuilds, adjustments in the number of stores and store space to optimize the store portfolio across markets. This strategy allows about a third of leases to be renegotiated or exited annually.

Development in 2023

The financial year showed a 6% increase in net sales to SEK 236,035 million, offset by a 1% local currency decrease. Without Russia and Belarus, the growth was 8% in SEK and 1% in local currencies, with online sales making up 30%.

The portfolio brands enjoyed an 15% and 9% increase in SEK and local currencies, respectively, during the year. Eastern Europe, excluding Russia, Belarus, and Ukraine, noted a 15% and 5% uptick in SEK and local currencies, respectively. Notably, H&M resumed Russian operations temporarily and reopened seven Ukrainian stores in November 2023.

The annual gross profit improved by 7% to SEK 120,896 million, resulting in a 51.2% gross margin. These boosts stem from supply chain improvements, a cost and efficiency program, and normalized purchasing costs.

Selling and administrative expenses fell by 4% to to SEK 107,330 million. These reductions reflect operational cost control and the cost and efficiency program's impact, which anticipates SEK 2 billion in annual savings once fully implemented.

Operating profit increased to SEK 14,537 million, a 6.2% operating margin (H&M definition). This improvement is credited to robust gross margins, the efficiency program, and cost control, with past one-time costs impacting the previous year's comparison.

Associated company and joint venture investments yielded SEK 971 million, mainly from Sellpy's revaluation in Q1.

CEO Helena Helmersson underscored H&M's strategic advancements and commitment to long-term goals despite economic challenges. Improvements in the supply chain and gross margin, prudent cost control, and a focus on enhancing customer experience through tech investments were highlighted. The portfolio brands, especially COS, Arket, and Weekday, are increasingly contributing to profitability. New ventures like Sellpy are creating additional revenue streams, and the company is making strides towards its sustainability and climate goals, with a 20% reduction in greenhouse gas emissions since 2019. Looking to 2024, H&M Group anticipates continued profitable and sustainable growth, powered by strategic investments and a strong financial base.

Value and quality inside

While H&M may not possess a definitive moat, the company's significant brand recognition and favor among consumers, coupled with its operational efficiency and substantial scale, afford it certain competitive advantages. In spite of various challenges, H&M has consistently demonstrated revenue growth, with potential for further expansion into new markets.

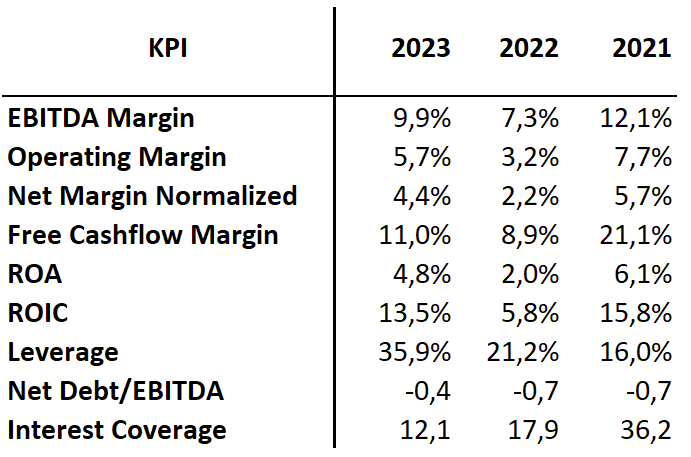

Currently, margins may not be particularly noteworthy, yet the company maintains profitability, exhibits a robust Return on Invested Capital (ROIC), and generates substantial free cash flow. Additionally, H&M's low levels of debt enhance its financial profile. These factors collectively indicate that H&M Group holds considerable value.

Store Portfolio Optimization

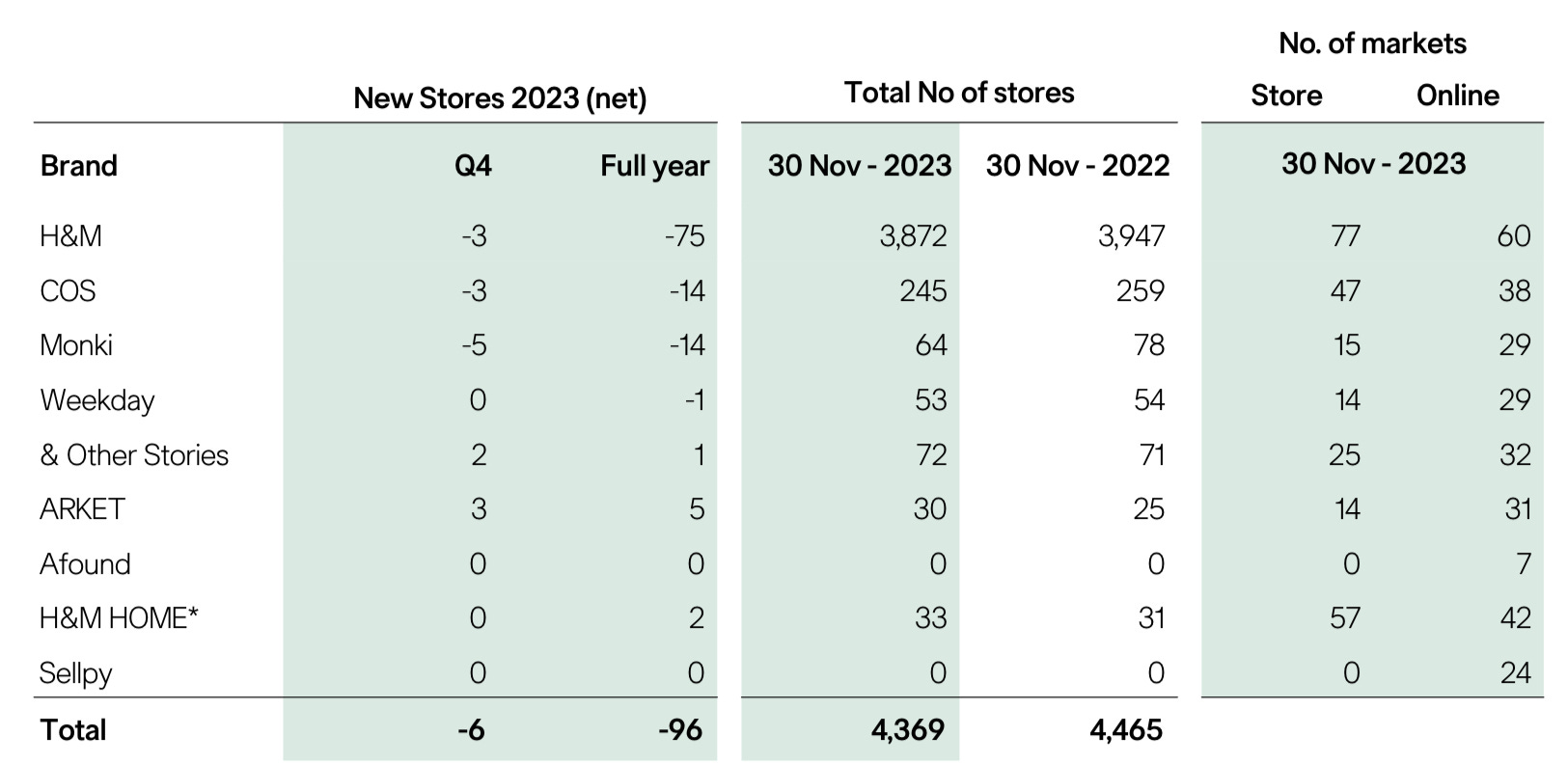

The H&M Group experienced a peak in its retail footprint in 2019 with 5,076 stores, more than doubling from 2,206 in 2010. However, the following years saw a strategic downsizing to 4,365 stores by 2023. The mainstay of these stores is the flagship H&M brand, which maintains the broadest market presence. The company's financial disclosures aggregate sales and operating income by region rather than by each brand, making it challenging to determine individual brand performance within the group.

Looking ahead to 2024, H&M plans to open around 100 new stores while simultaneously closing about 160, resulting in a net reduction of 60 stores. This shift in strategy emphasizes expansion in emerging markets while scaling back in more saturated, established markets, a move anticipated to have a favorable impact on sales.

Acknowledging the underperformance of certain locations, H&M's management is proactively optimizing the store portfolio in an effort to cut costs and bolster profitability. As part of its evolving distribution strategy, the Group is placing a heightened focus on online sales. Despite the shift towards digital, H&M faces ongoing challenges that call for enhancements in supply chain efficiency and logistics management.

Since the zenith of 2019, H&M has reduced its store count by 14%, a trend reflective of the broader retail industry's pivot towards streamlined operations and omnichannel sales approaches.

Share buybacks and Dividends

In September 2023, H&M Group initiated a SEK 3 billion share buyback program, authorized by the 2023 Annual General Meeting (AGM). As of 30 November 2023, the company repurchased 7,138,790 B shares for SEK 1,123 million, with the program expected to continue until 31 March 2024. The intention is for these repurchased shares to be cancelled, subject to approval at the 2024 AGM.

Regarding dividends, H&M Group aims to deliver a good return to shareholders while maintaining a strong financial position to support growth and investments. The dividend policy suggests that the ordinary dividend should exceed 50% of profit after tax over time. Additionally, surplus liquidity, considering the capital structure target and investment needs, may be distributed to shareholders via extra dividends or buyback programs.

For 2024, the Board proposes a dividend of SEK 6.50 per share, unchanged from the previous year, to be paid in two installments in May and November. Furthermore, the Board will seek authorization at the 2024 AGM for a general authorization to buy back B shares up to the 2025 AGM, providing flexibility in managing the group's capital structure.

Growth Ambitions by 2030

After several challenging years, the company aims to refocus on growth, setting the ambitious goal of doubling its revenue by 2030 (base year is 2021) and achieving an EBIT margin of over 10%.

The plan set forth is notably ambitious, and it's reasonable to approach its feasibility with a degree of skepticism. With FY 2023 revenue reported at 236 billion SEK, H&M aims to achieve a revenue target of approximately 400 billion SEK by 2030. To meet this objective, the company would need to maintain a Compound Annual Growth Rate (CAGR) of 7.83%. While this growth rate may appear manageable at first glance, given H&M's recent performance and market challenges, a cautious outlook is warranted.

I also question whether this is the right approach for H&M. As highlighted, over the past 15 years, H&M has expanded significantly at the expense of profitability and return on investment. Many stores that were opened with substantial investments are now being closed, but it's crucial for management to learn that growth at any cost may not be sustainable. While it's positive that the company is now also focusing on improving its EBIT margin, a target of 10% seems too modest.

CEO Change

The sudden leadership change at H&M, with Daniel Ervér replacing Helena Helmersson as CEO, marks a significant moment for the Swedish fashion conglomerate. Helmersson's departure after four years at the helm and 26 years with the company—during which she led H&M through a pandemic and various geopolitical and macroeconomic challenges—was unexpected. Her tenure, characterized by navigating through exceptionally turbulent times, was acknowledged as both a period of notable achievements and personal challenges.

Daniel Ervér, a long-standing H&M insider with 18 years of service, steps into the CEO role with a background that includes key responsibilities in merchandising for H&M in Germany and, more recently, overseeing the core H&M brand. His appointment signifies a continuation of leadership from within the company's ranks, suggesting a potentially smooth transition given his extensive experience and understanding of the company's operations across its various brands, including COS, Weekday, and & Other Stories.

The transition occurs against the backdrop of a disappointing quarterly report that saw the company's stock decline. This change at the top, coupled with financial performance concerns, introduces a period of uncertainty and scrutiny for H&M. Stakeholders will be closely watching Ervér's approach to steering the company through its current challenges, his strategy for maintaining H&M's competitive edge in the fast-paced fashion industry, and how he plans to address the ongoing pressures of retail in a post-pandemic market environment. The internal promotion of Ervér, while ensuring leadership continuity, raises questions about the strategic shifts he might implement to rejuvenate the brand and improve financial performance.

Attractive valuation

A conservative Discounted Cash Flow (DCF) analysis suggests that the stock is significantly undervalued. In this model, even if the company falls short of its projected growth (CAGR of 2.0% to 3.0%) and profitability targets (normalized EBIT Margin of approximately 6.5% to 7.0%), there remains a substantial margin of safety.

The estimated fair value range for the stock is between 255 SEK to 270 SEK per share. Given the current share price of approximately 140 SEK, this implies a margin of safety ranging from 182% to 193%, highlighting a potentially undervalued investment opportunity.

Supporting this valuation, several multiplier metrics corroborate the undervaluation estimate. The Next Twelve Months (NTM) Enterprise Value to EBIT (EV/EBIT) ratio stands at 13.97x, which is below its 3-year average of 18.55x. Additionally, the NTM Market Cap to Free Cash Flow ratio is trading at 10.69x, compared to its 3-year average of 12.43x. These comparisons further highlight the stock's potential undervaluation relative to historical performance.

Insider buys

In early February, board member Christina Synnergren made a substantial investment in H&M stocks, acquiring 34,475 shares at an average price of 145.01 SEK per share, totaling an expenditure of 5 million SEK (approximately 475 thousand USD).

Conclusion

The large Swedish fashion conglomerate, known for its leading brands, has historically prioritized expansion at the expense of profitability. Currently, it is striving to achieve a double-digit operating margin through initiatives such as store closures, enhancing operational efficiencies, and implementing an omnichannel strategy. Despite setting potentially overambitious growth targets for 2030, the company demonstrates resilience and quality by continuing to grow amidst the challenges posed since 2020.

The new CEO faces the substantial challenge of possibly reevaluating these goals. A shift towards prioritizing margin improvement and Return on Invested Capital (ROIC) would be beneficial, aligning with the hopes that the new leadership will focus more on these areas. Despite the conservative assumption that the company may fall short of its objectives, the stock appears undervalued, underscoring the inherent strength and potential of the company.

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is invested in H&M Group.