#34 NVIDIA Valuation

#34 NVIDIA Valuation

What is the fair value of the AI champ?

Dear readers,

thank you for being here and for your interest in my work! If you like this article and if you want to support my work, please feel free to subscribe! Please read the disclaimer at the end of this article. This is not an investment advice!

Introduction

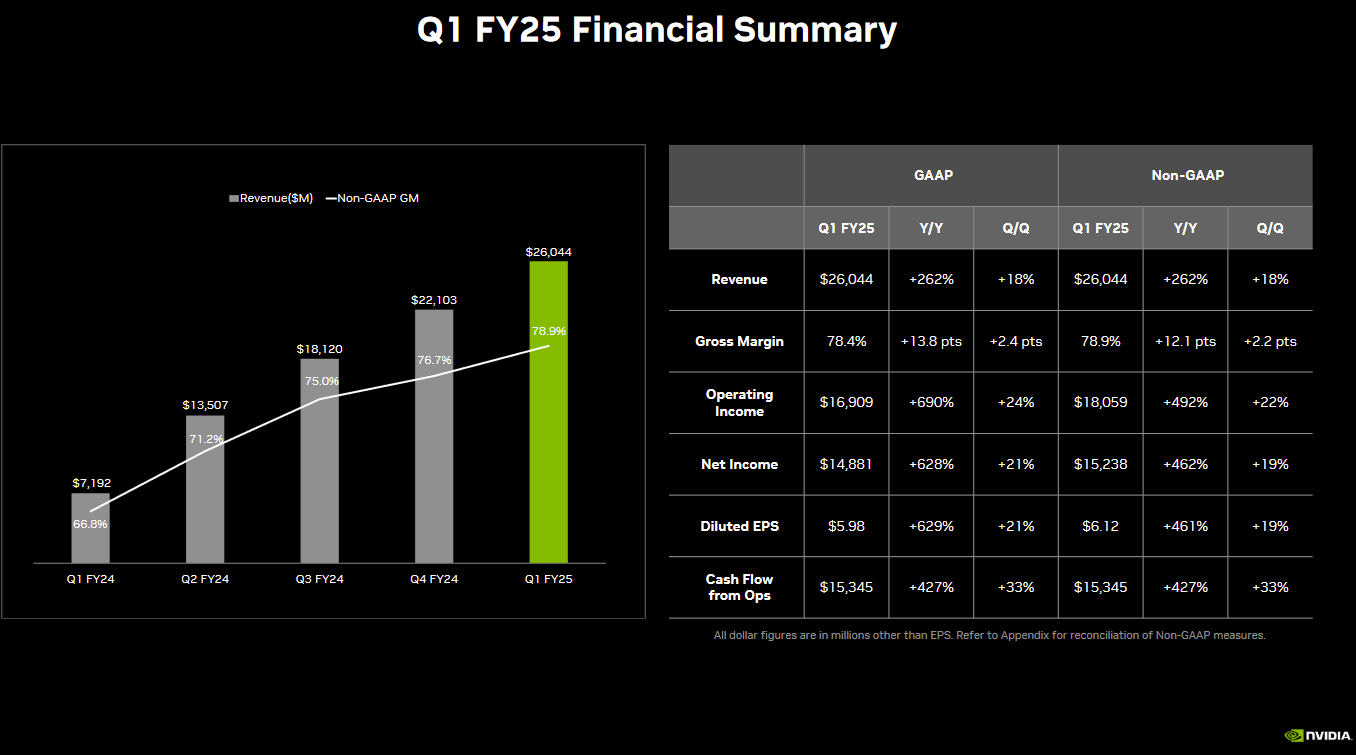

Nvidia NVDA 0.00%↑ has reached new heights, boasting a market cap of $2.8 trillion, now towering over giants like Amazon and Tesla, and edging closer to Apple and Microsoft. The company’s recent financial performance is nothing short of spectacular, with a 262% increase in revenue and a staggering 690% rise in earnings year-over-year. Under the leadership of visionary CEO Jensen Huang, Nvidia has consistently seized emerging tech trends over the past decades. From revolutionizing gaming and media to pioneering cloud computing and cryptocurrency, Nvidia is now set to spearhead the next industrial revolution powered by artificial intelligence.

Nvidia's strategic alliances with advanced chip foundries, particularly TSMC, have been a cornerstone of its rapid innovation and sustained high margins. This savvy collaboration has allowed Nvidia to leapfrog competitors like Intel, maintaining its position at the forefront of the tech industry. Nvidia is at the helm of building "AI factories," with its cutting-edge H200 chips driving pivotal AI applications, such as OpenAI's GPT-4. The demand for these chips far exceeds supply, painting a bright future for Nvidia’s growth, especially in the realms of autonomous driving and consumer internet.

Nvidia’s GPUs were game-changers in the 2000s, meeting the burgeoning demands for multimedia and gaming. The company adeptly adapted to the shifts toward mobile computing, cloud computing, and cryptocurrency, consistently staying ahead of the curve. Nvidia’s early recognition of GPUs' potential in AI, championed by researchers like Andrew Ng, established it as a leader in AI hardware. Strategic realignment around data centers and AI applications in the 2010s solidified its dominance in this critical sector.

Nvidia’s partnership with TSMC leverages cutting-edge manufacturing capabilities without owning fabrication plants, unlike Intel. This fabless model has enabled Nvidia to scale rapidly and introduce powerful chips efficiently, maintaining its competitive edge. Competitors like AMD and Intel are launching AI chips, aiming to capture a slice of Nvidia's market share. Nevertheless, Nvidia’s focus on model inference and innovative AI applications keeps it ahead, continually pushing the boundaries of technology. Ongoing investments from tech giants like Tesla and Meta in AI infrastructure signal sustained demand for Nvidia’s products. This continuous support from industry leaders underscores Nvidia’s pivotal role in the tech ecosystem.

Nvidia is impeccably positioned for future growth in AI and accelerated computing markets. Despite potential market share challenges, its relentless innovation and strategic foresight ensure continued relevance and profitability. Nvidia's remarkable ability to adapt and lead in evolving tech landscapes highlights its strategic brilliance, cementing its status as a key player in the next wave of technological innovation.

NVIDIA Valuation

Valuing Nvidia stock at the moment is challenging due to several key factors. First, the rapid and unprecedented growth in the AI and data center markets, where Nvidia is a dominant player, makes future revenue projections highly uncertain. The demand for Nvidia’s advanced GPUs and AI technologies can fluctuate significantly based on technological advancements, competitive actions, and shifting customer needs.

Second, the geopolitical landscape introduces additional volatility. Export controls, particularly affecting sales to China, can abruptly alter Nvidia's market opportunities and revenue streams. These regulatory uncertainties add layers of complexity to any valuation effort.

Third, the company's financial performance is heavily influenced by supply chain dynamics. Nvidia relies on third-party manufacturers, and any disruptions or mismatches in supply and demand can lead to substantial financial variability. This dependence complicates the prediction of future earnings and profit margins.

Lastly, Nvidia's high market valuation, reflecting optimistic growth expectations, incorporates significant speculative elements. Investors' high expectations for future growth in AI and other emerging technologies can lead to overvaluation if the company does not meet these lofty projections.

Together, these factors create a volatile and unpredictable environment, making it difficult to establish a stable and accurate valuation for Nvidia stock.

Base Case Assumptions

The foundation of this growth projection is NVIDIA's continued technological leadership, a soaring demand for AI solutions, and an absence of significant economic or geopolitical disruptions.

Revenue Growth

In the DCF Model, a five-year detailed planning period is used, projecting a 22% Compound Annual Growth Rate (CAGR) until 2028. This trajectory anticipates NVIDIA's revenue to reach a staggering $217 billion by 2028.

EBIT Margin

In the last twelve months, NVIDIA's EBIT margin was an impressive 60%. For the DCF Model, I have normalized this margin to a more conservative 56%.

Normalized Net Income Margin

From the EBIT margin, the Last Twelve Months (LTM) Normalized Net Income margin stands at 53.4%. Moving forward, it is estimated to stabilize around 49%.

Free Cash Flow

My Free Cash Flow assumptions include a Net Capex ratio as a percentage of sales (Net Capex = Capex - Depreciation) of 0.9%, reflecting the average of recent years. Working Capital, expressed as a percentage of sales, is determined by the average Working Capital over the past years, calculated at 12.3% of net sales. The Free Cash Flow estimation does not adjust for stock-based compensation.

WACC

The Weighted Average Cost of Capital (WACC) is set at 8.5%.

Results

Based on these assumptions, NVIDIA's equity value is estimated at $1.863 trillion. Dividing this by the current number of shares, we derive a fair value per share of $757. In comparison to its latest stock price of $1,096, the stock appears significantly overvalued.

Adjusting the WACC to 9% would lower the fair value per share to $664, while a decrease in WACC to 8% would increase it to $852 per share.

Scenarios

Bull Case Scenario:

In an optimistic scenario, assuming a CAGR for revenue of 24.6%, an EBIT Margin of 59%, and a normalized net income margin of 51%, the fair value per share would be $828.

Bear Case Scenario:

Conversely, in a pessimistic scenario with a CAGR for revenue of 19.7%, an EBIT Margin of 40%, and a normalized net income margin of 47%, the fair value per share would be $686.

In both extreme scenarios, the stock remains overvalued.

Conclusion

NVIDIA’s rise to prominence and its current status as a technological leader in AI is nothing short of extraordinary, largely due to the visionary leadership of CEO Jensen Huang. NVIDIA's journey is a unique success story, capitalizing on AI developments and thriving like no other company at present. However, this success is not without its risks, which must be carefully considered.

Risks

One significant risk is the concentration of sales to a limited number of partners and distributors. NVIDIA generates a substantial portion of its revenue from a small group of direct customers. For example, in the first quarter of fiscal year 2025, two major customers, referred to as Customer A and Customer B, accounted for 13% and 11% of NVIDIA's total revenue, respectively. These customers are primarily associated with the Compute & Networking segment. If any of these partners were to reduce their purchases, develop competing solutions, or if NVIDIA were unable to sell to them due to trade restrictions, the company’s financial health could be severely impacted. Additionally, ongoing geopolitical tensions, particularly between Taiwan and China, pose a significant threat to NVIDIA's supply chain and overall business operations.

Valuation Concerns

NVIDIA's stock price and equity value have skyrocketed in recent years. While the overvaluation itself is not the primary concern—since stocks can continue to rise—the real issue lies in the enormous expectations now placed on NVIDIA by the market. According to my DCF Model assumptions, NVIDIA must sustain exceptionally high revenue growth rates and maintain extraordinarily high margins over an extended period to justify its current valuation. This feat will be achievable only if there are no major disruptions and if NVIDIA can maintain its technological leadership as the number one in the industry.

Finally, my questions for all readers. What do you think about NVIDIA's valuation?

Thank you for your interest in this article! If you are interested in more, please subscribe!

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is not invested in NVIDIA.

Great read. I was there to read the comments since they always add a lot of color. All valid points! Honestly you all should do a collaboration post on Nvidia just to takle different perspectives. @thecapitalist @krokerequityresearch @olgausvyatsky

Great post!

In a bit more optimistic scenario, my fair value was $1,147. However given that we may be at beginning of something that is really big, all these traditional valuation methods may be rendered meaningless.

Jensen Huang says data centers deployed will double in the next 10 years and GPUs in those data centers will have to be replaced in every 4 years. If that scenario materializes, $NVDA can also easily double even from here.

But all these are speculations and investors will be better off sticking with conservative assumptions!