#10 Walgreens - Value Trap or Opportunity?

#10 Walgreens - Value Trap or Opportunity?

A look at Walgreens' future prospects and challenges

No Investing advice! Please see disclaimer at the end of the post, thanks!

Introduction

This analysis of Walgreens Boots Alliance WBA 0.00%↑ approaches the subject objectively, without personal evaluations. The stock's performance over the past half-decade has been disappointing, with a significant decline of approximately 62% in its value, leading to substantial erosion of shareholder value.

This analysis aims to examine the future prospects of the company. To achieve a comprehensive understanding, the evaluation will go beyond traditional key performance indicators such as operating and net margins, free cash flow margins, Return on Invested Capital (ROIC), and debt levels.

The focus will be on several critical areas that are key to assessing whether Walgreens remains a compelling investment proposition. We will look into the company's transformation initiatives, the strategic direction under the new CEO, the potential impact of a Boots UK IPO, the ramifications of ongoing opioid litigations, and the fiscal outlook for 2024. Furthermore, an examination of the stock valuation and dividend policy will offer additional insights into the company's attractiveness to long-term investors.

The purpose of this analysis is to ascertain whether Walgreens is a viable investment option to retain in a portfolio or if it is an advantageous time for new investments. The objective is to provide an impartial perspective that encompasses the difficulties and possibilities that Walgreens faces in the changing healthcare and retail pharmacy industries.

Key figures

Ticker: WBA

Market Cap: $22.5 bn

Employees: 331,000

Focus Areas

This analysis delves into crucial topics for long-term investors considering Walgreens Boots Alliance. The topics highlight the company's current status and provide insights into its future trajectory. The key topics include:

Transformation Initiatives

U.S. Healthcare Segment

New CEO Leadership

Boots IPO Prospects

Opioid Litigations

2024 Financial Outlook

Stock Valuation

Dividend Analysis

By exploring these areas, this deep dive aims to provide a holistic view of Walgreens Boots Alliance, offering long-term investors a comprehensive understanding of the company's strengths, challenges, and potential for future growth.

Transformation

Launched in December 2018, Walgreens' Transformational Cost Management Program is a strategic initiative aimed at improving cost efficiency and streamlining operational processes. The program aimed to realize over $2 billion in annual savings by fiscal 2022, a goal that was impressively achieved by the end of fiscal 2021. Since then, Walgreens has continued to raise its cost-saving ambitions.

Program Expansion and Extension: In October 2021, the initiative was expanded and extended through fiscal year 2024, with an annual savings target of $3.3 billion. The target was later revised upward to $3.5 billion for fiscal year 2022 and further to $4.5 billion by the end of fiscal year 2024.

Progress Update: Currently, Walgreens appears to be on a solid trajectory to meet these enhanced savings goals.

Program Scope: The program includes divisional optimization, global smart spending, a streamlined organizational approach, and IT modernization. These initiatives target the U.S. Retail Pharmacy and International segments, alongside global corporate functions.

Store Rationalization: An important aspect of this strategy is optimizing the store network. The plan includes reducing up to 300 Boots stores in the UK and 200 in the US by fiscal year 2024, in addition to the previously planned closures of approximately 350 Boots stores in the UK and 450-500 in the US. As of August 31, 2023, Walgreens has successfully closed 291 stores in the UK and 466 in the U.S.

Financial Repercussions: For fiscal year 2023, the estimated cumulative pre-tax charges to GAAP financial results related to this program have increased from $3.6 billion to between $4.1 and $4.4 billion. These increased charges are due to heightened charges associated with exit and disposal activities.

Accumulated Charges: From its inception until August 31, 2023, Walgreens has recognized $3.1 billion in cumulative pre-tax charges, mainly within Selling, General, and Administrative expenses. These costs cover a range of financial obligations, including lease commitments, real estate expenses, asset impairments, employee severance, business transition costs, IT transformation, and other associated exit expenditures.

The program highlights Walgreens' proactive stance towards enhancing efficiency and cost control. However, it also emphasizes the significant financial and operational implications of such a comprehensive transformation. The ambitious targets and broad scope of the program reflect the company's assertive strategy to adapt to evolving market dynamics and business demands. However, the financial charges and store closures associated with this extensive restructuring operation present significant immediate challenges.

Despite achieving substantial cost savings through this program, there has not been a commensurate improvement in operating margins over the years. This observation points to a complex interplay between cost management and overall financial performance, emphasizing the need for a balanced approach that aligns cost reduction with sustainable profitability and growth.

U.S. Healthcare Segment

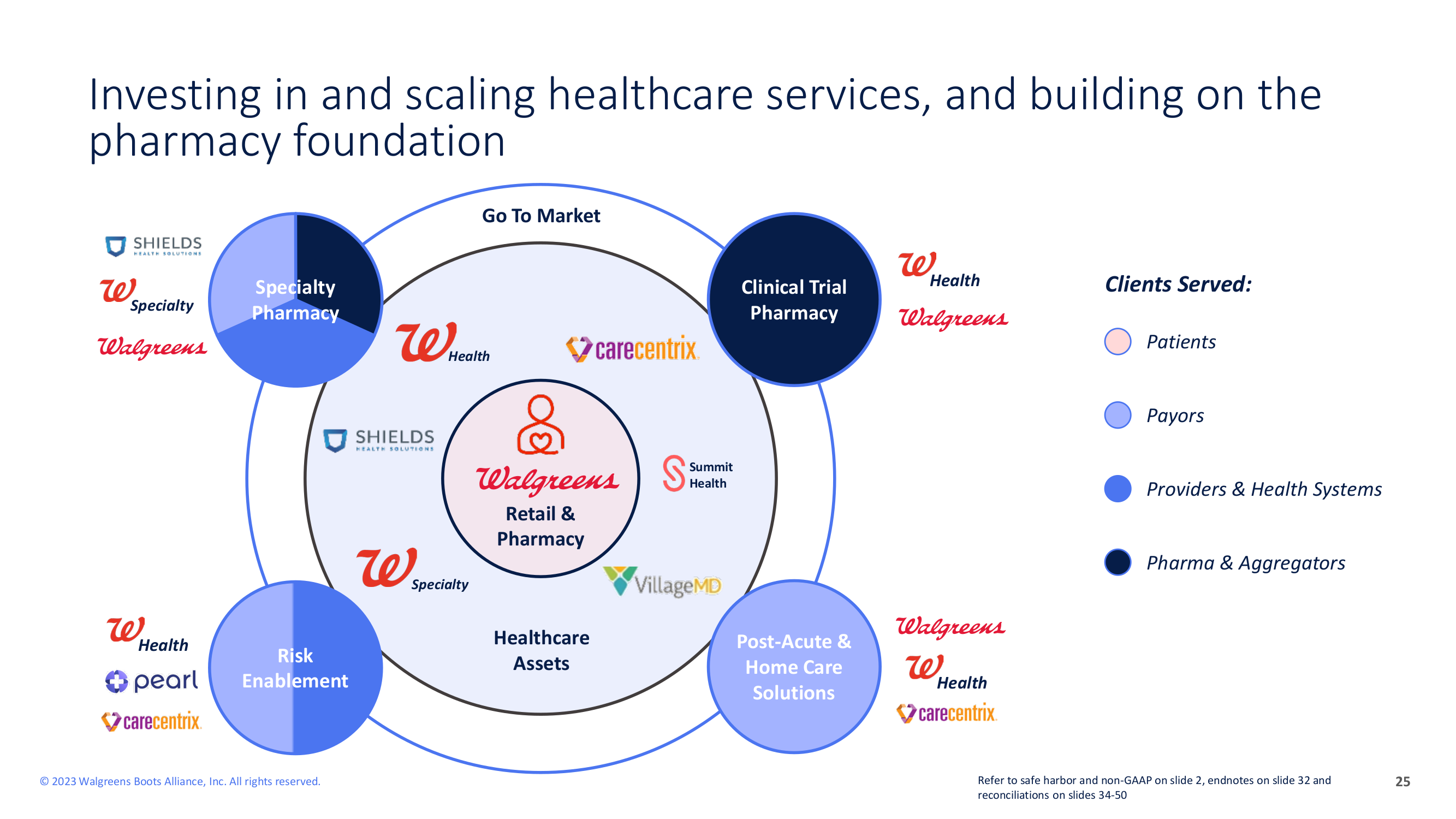

The U.S. Healthcare segment of the Company, established at the outset of fiscal 2022, represents a forward-thinking, technology-driven healthcare enterprise focused on delivering a consumer-centric experience. This segment is structured to provide a holistic, omni-channel journey for consumers, encompassing every stage of their healthcare needs. Its primary objective is to enhance health outcomes while simultaneously reducing costs for both payors and providers. This is achieved through a blend of direct care provision and strategic partnerships.

Key components of the U.S. Healthcare segment include:

VillageMD: Holding a majority stake, VillageMD stands as a prominent provider of value-based care. It offers a wide range of services, including primary care, multi-specialty, and urgent care, available in traditional clinics, through at-home visits, and via online appointments.

Shields: Functioning as a specialty pharmacy integrator, Shields collaborates with hospitals to enhance and accelerate pharmacy services, emphasizing a patient-focused approach.

CareCentrix: As a key player in the post-acute and home care management sectors, CareCentrix focuses on providing essential support and care in the crucial period following acute medical treatment.

Walgreens Health Organic Business: This division contracts with payors and providers to deliver a comprehensive range of clinical healthcare services and care management programs. These services are accessible to members and their caregivers through both digital platforms and physical channels, ensuring a versatile and responsive healthcare experience.

The U.S. Healthcare segment demonstrates the Company's dedication to advancing the healthcare industry by utilizing technology and personalized care to meet the diverse needs of today's healthcare consumers.

The strategy for the U.S. Healthcare Segment is designed to maximize profitability and operational efficiency. The approach focuses on targeted growth within key areas of the healthcare sector.

Emphasizing Profitable Healthcare Growth: The main goal is to achieve profitable growth, especially in the U.S. healthcare sector. This involves utilizing the capabilities of VillageMD, Summit Health, and CityMD. By concentrating on these entities, the company intends to improve its services, broaden its patient base, and optimize revenue streams in the healthcare industry.

Strategic Market Focus and Clinic Optimization: The company is conducting a strategic reassessment of its market presence and clinic operations in order to achieve growth. As part of this process, the company plans to exit approximately five markets and close around 60 clinics that do not align with its strategic goals or are underperforming. The goal is not only to scale back, but also to refocus efforts and resources on markets that offer the greatest potential for profitable growth. The reason for this decision is to allocate resources more efficiently, focusing on regions and clinics that align with the company's strategic vision and have demonstrated or have the potential for high-performance metrics.

Enhancing Operational Efficiency: The company aims to enhance operational efficiency by withdrawing from these markets and optimizing its clinic portfolio. This involves reducing overhead costs, streamlining operations, and reallocating resources to more profitable areas. The objective is to establish a healthcare segment that is more agile and responsive, capable of adapting to changing market dynamics and patient needs.

Investing in High-Potential Areas: The funds and efforts saved from these market exits and clinic closures will be reinvested into areas with higher growth prospects. This could involve expanding services in existing profitable markets, investing in new technologies to enhance patient care, or exploring new healthcare models that align with emerging trends in the industry.

Focus on Quality and Patient Outcomes: Central to this strategy is the commitment to maintaining high standards of patient care and outcomes. Despite the focus on profitability, the company is dedicated to ensuring that the quality of care remains a top priority, understanding that patient satisfaction and health outcomes are key drivers of long-term success in the healthcare sector.

In summary, the U.S. Healthcare Segment Strategy is a balanced approach that combines prudent market and clinic optimization with a focus on profitable growth areas. This strategy is expected to not only streamline operations and reduce unnecessary expenditures but also to bolster the segment's ability to provide high-quality healthcare services in a more focused and effective manner.

Possible Boots U.K. IPO

Walgreens Boots Alliance (WBA) is reportedly considering an Initial Public Offering (IPO) on the London Stock Exchange for its UK-based Boots pharmacy chain. This strategic move follows unsuccessful attempts to sell the business last year.

IPO Consideration: The potential IPO, which could value Boots at around £7 billion (approximately $8.8 billion), is part of early discussions about the future of the chain. This move would not only mark a major shift in WBA's strategy but also potentially provide a significant boost to the London stock market.

Previous Sales Efforts: The consideration for an IPO follows unsuccessful attempts to sell Boots. The failure to secure a buyer last year has led WBA to explore other options to offload the UK pharmacy chain, with an IPO being a prominent alternative under discussion.

Boots' Performance: Notably, Boots reported a 12% rise in like-for-like sales in the fourth quarter, demonstrating its solid financial performance and potential attractiveness to investors. This uptick in sales might enhance its appeal in the public market, making an IPO a viable option for WBA.

In summary, Walgreens Boots Alliance is considering the future of its UK subsidiary, Boots, with a London IPO being a significant possibility. This move is driven partly by previous unsuccessful sale attempts and the chain's robust financial performance. A successful IPO could lead to a major realignment in WBA's business strategy and potentially have a notable impact on the London Stock Exchange.

New CEO Tim Wentworth

In October 2023, Walgreens Boots Alliance, Inc. announced the appointment of Tim Wentworth as its new Chief Executive Officer, effective from October 23, 2023. This decision marks a significant transition in the company's leadership. Wentworth, a seasoned professional in the healthcare industry, previously served as the CEO of pharmacy-benefits manager Express Scripts. His appointment followed Rosalind Brewer's departure as CEO at the end of August 2023.

Tim Wentworth's experience in pharmacy services will be invaluable as Walgreens navigates the complex and evolving healthcare and retail pharmacy sectors. His leadership will be pivotal in steering Walgreens through its current challenges and opportunities, focusing on growth, efficiency, and innovation within the company's diverse operations.

Opioid crisis

As a major pharmacy retailer in the United States, Walgreens has played a significant role in the distribution and sale of prescription opioids. This has placed the company at the center of the nation's opioid crisis and led to legal scrutiny and challenges. The focus of these legal challenges has primarily been on Walgreens' management of opioid distribution and dispensing.

Legal Challenges and Settlements: Walgreens was accused of inadequate oversight in dispensing opioids, which allegedly contributed to their misuse and diversion. As a result, the company became involved in numerous lawsuits and major settlements, resulting in significant financial penalties and requiring changes in its practices to implement more stringent monitoring and reporting of opioid dispensing.

Efforts in Addressing the Crisis: In response to these challenges, Walgreens has implemented more stringent controls on opioid dispensing. This includes enhanced tracking systems and stricter adherence to prescribing guidelines. Additionally, the company has supported treatment and prevention efforts by participating in drug take-back programs and providing access to naloxone, an overdose-reversing medication.

Impact on Business and Reputation: The opioid crisis involvement had a notable impact on Walgreens' reputation, prompting a review of its business practices related to prescription medications, particularly opioids.

Ongoing Developments: Walgreens continues to face legal proceedings related to the opioid crisis, influencing policy changes and affecting the company's operations regarding controlled substances.

Key Milestones in Opioid Litigation:

1. Settlement with Florida (May 5, 2022): Walgreens announced a $683 million settlement with the State of Florida, including $620 million in remediation payments over 18 years and $63 million for attorneys' fees, to resolve claims related to opioid distribution and dispensing.

2. National Settlement Frameworks (November 2, 2022): The company agreed to terms to potentially resolve a majority of opioid-related lawsuits for up to approximately $4.8 billion and $155 million in remediation payments to states, political subdivisions, and tribes over 15 years, along with $754 million in attorneys' fees.

3. Financial Accruals (November 30, 2022): Walgreens recorded a $6.5 billion liability for the settlement frameworks and other opioid-related claims.

4. Multistate Settlement Agreement (August 7, 2023): This became effective after sufficient participation from states and subdivisions, resolving litigation with all states, territories, tribes, and most subdivisions. The company accrued a total liability of $7.0 billion for these settlements.

5. Continued Defense in Litigation: Walgreens continues to defend against litigation not covered by the Multistate Settlement Agreement and believes in its strong legal defenses in these cases.

Consolidated Multidistrict Litigation: Walgreens remains a defendant in federal court actions concerning the impacts of widespread opioid abuse. Many of these cases are part of the In re National Prescription Opiate Litigation, consolidated in the U.S. District Court for the Northern District of Ohio.

In summary, Walgreens' response to the opioid crisis reflects the complex challenges faced by pharmacies in balancing the provision of necessary medications with the prevention of their misuse and abuse. The company's substantial legal settlements, implementation of stricter controls, and ongoing legal defenses demonstrate its extensive involvement in addressing this significant public health issue.

Walgreens faces a significant financial commitment, estimated at around $7 billion in penalties over the next 15 years, averaging approximately $460 million annually. This poses a considerable financial challenge for the company, affecting both its reputation and financial stability. Such a substantial outlay could potentially limit Walgreens' ability to allocate funds for transformation and investment initiatives. The allocation of these resources towards penalty payments indicates a crucial moment for the company as it balances addressing past issues with investing in future growth and innovation.

Management Outlook for 2024

Walgreens Boots Alliance has outlined its financial outlook for fiscal year 2024, highlighting several key factors and strategic initiatives:

Sales and Profit Forecasts: The company projects total sales in fiscal '24 to increase by 1% to 4% on a constant currency basis. However, adjusted operating income (AOI) is expected to decline by 18% to 21% in constant currency terms, primarily due to property transactions from fiscal '23 and the pending sale of the business in Chile. Excluding these impacts, AOI growth is forecasted to be flat to up 2%, with continued growth in the Boots U.K. retail business being somewhat offset by inflationary pressures.

U.S. Healthcare and Retail Pharmacy: In the U.S. Healthcare segment, sales are expected to range from $8.3 billion to $8.8 billion, reflecting the first full year of Summit Health and ongoing growth in all businesses. Adjusted EBITDA for this segment is anticipated to be breakeven. The U.S. Retail Pharmacy segment is projected to see flat to 2% sales growth, with underlying business driving 5% to 10% AOI growth despite headwinds from lower COVID-19 contributions and reduced sale and leaseback gains.

COVID-19 Vaccinations and Retail Margins: Walgreens has already administered over 3 million COVID vaccinations quarter-to-date and expects to deliver approximately 5 million COVID vaccinations in 2024. In retail, margins are expected to benefit from the category performance improvement program and increased penetration of own brand products.

Cost Savings Initiatives: The company aims to achieve over $1 billion in cost savings during fiscal 2024. These savings are part of a broader strategy to improve the cost base across the company and drive underlying growth.

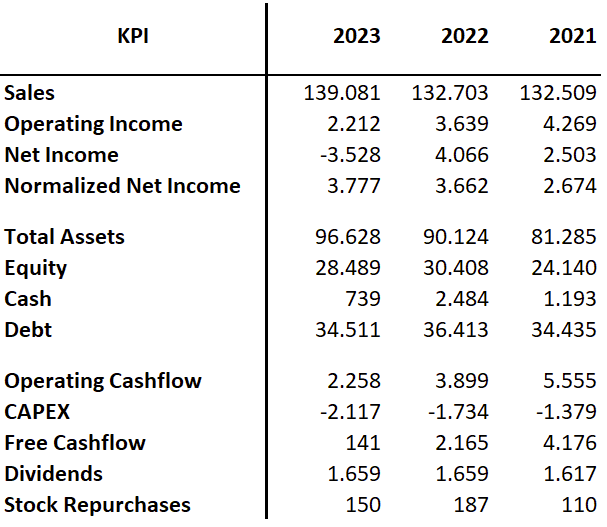

Capital Expenditures and Cash Flow: Fiscal '24 guidance includes reduced capital expenditures by approximately $600 million and a $500 million benefit from working capital optimization initiatives. This is in line with the efforts to improve free cash flow, following a fiscal '23 free cash flow of $665 million and a reduction in debt by $2.6 billion.

Adjusted Earnings Per Share (EPS): For fiscal '24, Walgreens is guiding adjusted EPS to be between $3.20 and $3.50, down from $3.98 in fiscal '23.

In summary, Walgreens' outlook for FY 2024 is a combination of strategic cost-cutting measures, anticipated growth in key business segments, and ongoing challenges from macroeconomic pressures and the evolving healthcare industry landscape. The company aims to balance growth with efficiency improvements to overcome these challenges.

Walgreens Stock Valuation

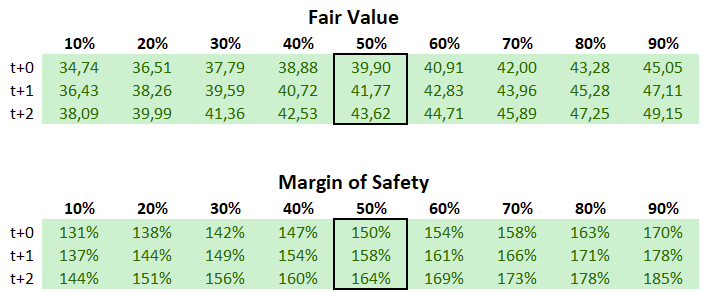

Walgreens stock is currently trading at historically low levels, which presents an interesting scenario for investors. Based on an analysis that assumes modest single-digit sales growth and a gradual improvement in margins over the coming years, the stock appears to be undervalued. This assessment considers a relatively high Weighted Average Cost of Capital (WACC), which reflects the various risks inherent in Walgreens' business environment, including market competition, operational challenges, and legal issues.

Furthermore, the TEV/EBIT multiplier suggests that Walgreens may be undervalued. This financial metric is commonly used to assess a company's valuation relative to its earnings power. It indicates that the market may not be fully recognizing Walgreens' earnings potential or its capacity for future growth and profitability improvements.

And what about the Dividend?

Walgreens Boots Alliance has a strong history of paying dividends, demonstrating its dedication to providing returns to shareholders. The company has paid dividends for an impressive 91 years and has consistently increased them for the past 47 years. This commitment to dividend growth showcases the company's financial discipline and long-term focus.

Walgreens currently offers a dividend yield of 7.37% based on the Last Twelve Months (LTM) dividend payments. This yield is particularly notable in the current market environment, making it an appealing aspect for income-focused investors.

During the Q4 earnings call, Ginger Graham, the Board's Lead Independent Director, confirmed that the Board has not altered its commitment to maintaining the current dividend policy, which includes annual increases in dividend payments. This statement reflects the leadership's confidence in the company's financial strategy and its dedication to preserving shareholder value.

However, it is important to acknowledge the financial challenges associated with sustaining such a dividend policy. Balancing dividend commitments with other financial obligations, including investments in growth initiatives, debt management, and navigating legal and operational challenges such as the opioid litigation, is a challenging task in the face of fluctuating market conditions and evolving healthcare landscapes.

Despite the challenges, the management's position suggests that maintaining and potentially increasing the dividend is a feasible goal, albeit not without difficulties. Achieving this will require strict financial management, operational efficiency, and successful execution of strategic initiatives. For investors, this aspect of Walgreens' financial policy should be considered alongside broader analysis of the company's performance, future outlook, and overall investment strategy.

Conclusion on Walgreens

The outlook for Walgreens' stock is complex, with both challenges and opportunities under the leadership of new CEO Tim Wentworth. Investors and stakeholders should take into account various key factors.

Leadership Challenges: The new CEO faces considerable hurdles, including navigating the complex healthcare landscape, addressing ongoing legal issues, and steering the company through a period of transformation. Effective management and strategic decision-making will be crucial for overcoming these challenges.

Attractive Valuation: Despite these challenges, Walgreens' stock may be appealing to investors due to its attractive valuation. The company's efforts in cost management and operational efficiencies could enhance its long-term value proposition.

Revenue Growth Prospects: Investors should temper expectations for massive revenue growth. The company's current focus appears to be more on improving operational efficiency and profitability rather than rapidly expanding revenues.

Potential for Improved Margins and Income: The strategic emphasis on cost savings and margin improvements could lead to increased profitability. The company's initiatives, such as the Transformational Cost Management Program, are aimed at enhancing margins and operational income.

Boots IPO Impact: The potential IPO of Boots UK could inject significant cash into Walgreens, offering resources for investment and the ability to address litigation claims. This move could provide the financial flexibility needed for strategic growth initiatives and debt management.

Importance of Risk Management: Post the opioid crisis, it's imperative for the management to ensure robust compliance and risk mitigation strategies to prevent similar incidents. Effective governance and oversight will be critical to maintain corporate reputation and investor confidence.

Opportunities in U.S. Healthcare: The U.S. healthcare sector, while complex and challenging, presents significant growth opportunities for Walgreens. The company's focus on expanding its healthcare services, including the development of the U.S. Healthcare segment, positions it to capitalize on this potential. Success in this area could be a major growth driver.

In conclusion, Walgreens' stock presents both challenges and opportunities. The company is positioned to enhance its profitability and market presence by focusing on operational efficiencies, cost management, and strategic expansion in the U.S. healthcare sector. However, successfully navigating legal, operational, and market challenges will be crucial to realizing this potential. Investors evaluating Walgreens should take into account the company's strategic initiatives and the inherent complexities of the healthcare industry.

And is Walgreens a Value Trap?

Determining whether Walgreens is a value trap is a complex challenge. On one hand, the company's deteriorating margins might suggest it could be a value trap. However, it's important to recognize the efforts of the management team, which is actively working to counteract these challenges. Additionally, the business is experiencing growth in sales and remains overall profitable, indicating underlying strengths despite the room for improvement.

In light of my current position, I've decided to maintain my investment in Walgreens. My analysis suggests that the company is undervalued, which mitigates some of the risks associated with the investment. However, I do not plan to increase my stake at this time. Instead, I intend to benefit from the dividends that the investment yields and monitor the company's progress with keen interest.

The evolution of Walgreens in the coming periods will be crucial. I am interested in observing how the management's strategies will unfold and affect the company's financial health and market position. This careful yet hopeful approach enables me to balance potential risks with the opportunities that Walgreens may present as a long-term investment.

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is invested in WBA.