#105 Inficon - A Stock Analysis

A Swiss High-Tech Sensor Specialist for the Long Run

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is not invested in the mentioned stock.

Inficon: A Swiss High-Tech Sensor Specialist for the Long Run

General Description of Inficon

Inficon Holding AG is a Swiss-based provider of advanced instruments and sensors for specialized industrial applications. The company’s products focus on gas analysis, measurement, and control in vacuum environments. These instruments are vital for detecting gas leaks in air conditioning, refrigeration, and automotive manufacturing, ensuring quality and safety in those industries. Inficon’s technologies are also critical in the complex fabrication of semiconductors and thin-film coatings (for products like microchips, flat-panel displays, solar cells, LEDs, and optical coatings) by monitoring and controlling conditions within high-vacuum production processes. Additionally, the company leverages its vacuum expertise to provide toxic chemical analysis devices used in emergency response, security, and environmental monitoring – for example, portable detectors for hazardous chemicals or pollutants.

Founded in 2000 via a consolidation of instrumentation businesses under OC Oerlikon, Inficon has grown into a global leader in niche sensing and process control. It has manufacturing facilities in Europe and the United States, with a worldwide sales and support network spanning North America, Asia, and Europe. Its customer base includes both equipment manufacturers (OEMs) and end-users – from major semiconductor chip makers and tool producers, to industrial OEMs and even governmental agencies. Inficon listed on the SIX Swiss Exchange in 2000 (and was briefly dual-listed on NASDAQ until 2005) and has a track record of steady growth through innovation and selective acquisitions. Today, it is recognized for its “world-class” sensor technologies and Industry 4.0 process control software, which help clients improve yield, productivity, and safety in high-tech manufacturing.

Latest Financials Snapshot (2024/Early 2025)

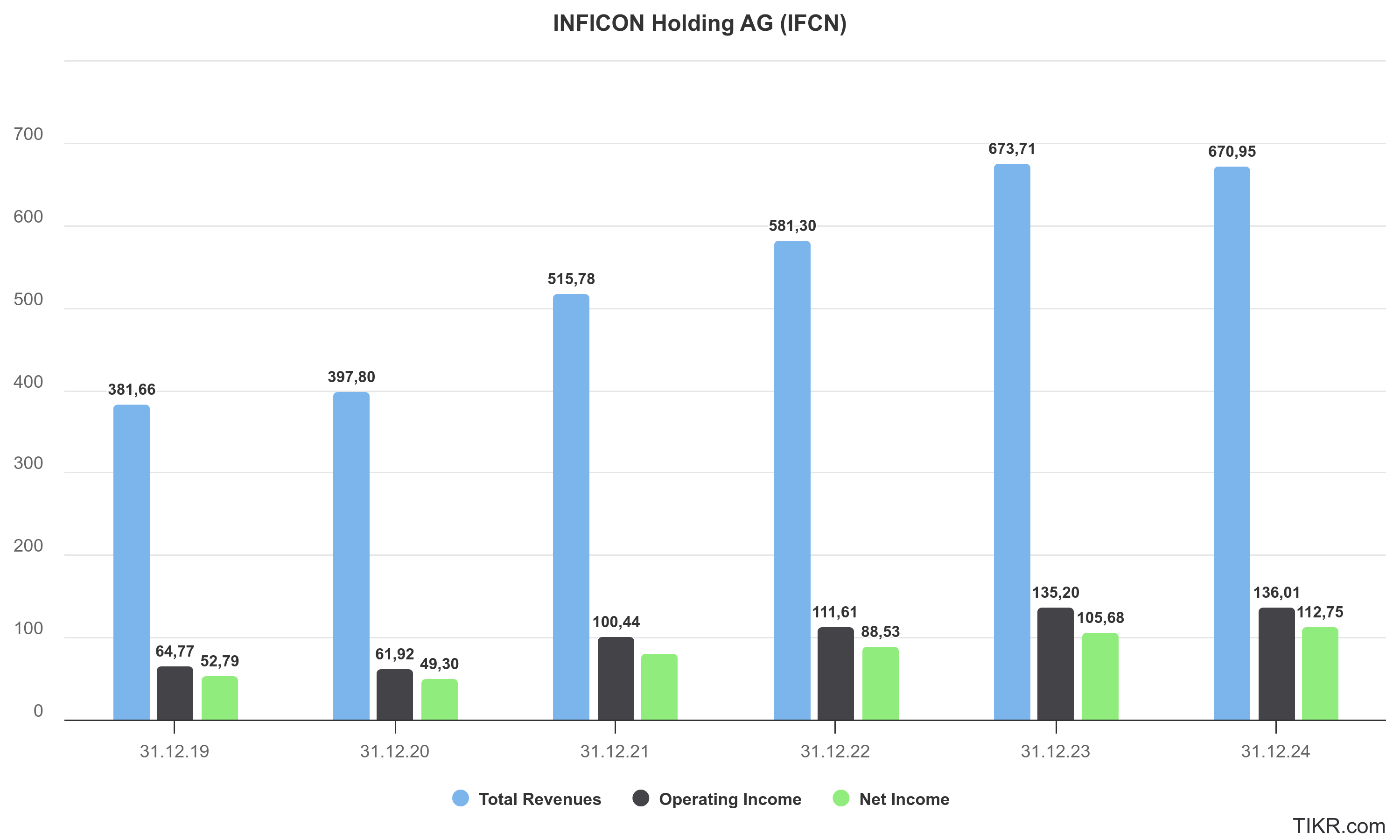

Inficon’s recent financial performance has been robust, even amid industry headwinds. In full-year 2024, the company achieved net sales of USD 671.0 million, essentially matching its 2023 record revenue (USD 673.7 million) despite a challenging macro environment. Operating profit in 2024 ticked up to USD 136.0 million, representing an operating margin of ~20.3% of sales. Net income for 2024 reached USD 112.8 million, about 6.7% higher than the prior year, as profit margins improved to a healthy 16.8% of sales. This net margin expansion reflects Inficon’s tight cost control and favorable product mix – gross profit margin rose to 47.1% in 2024 (up from 46.0% in 2023). Earnings per share accordingly climbed to $46.13 (on a pre-split basis) from $43.24 the year before.

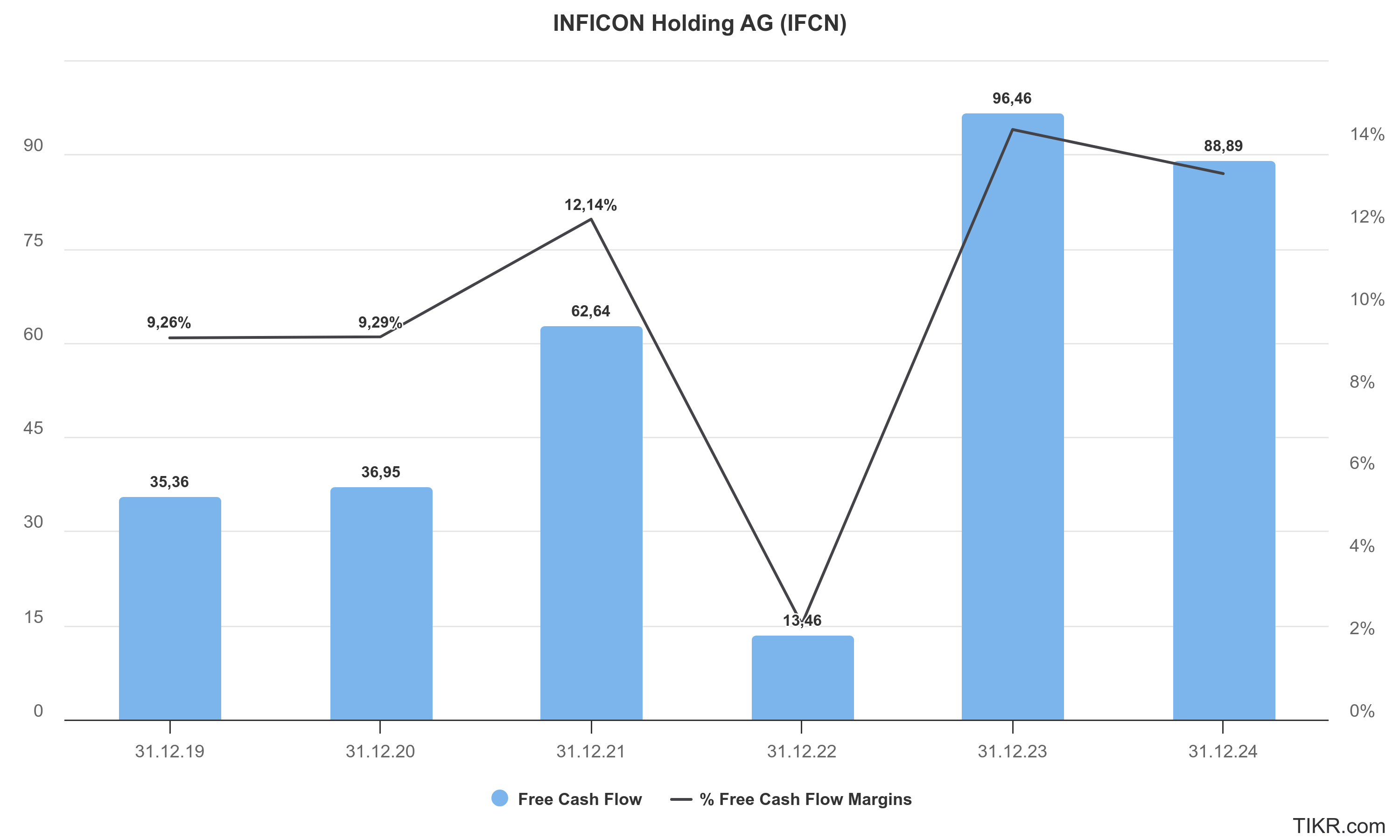

Importantly, cash flow and balance sheet metrics remain strong. Inficon generated USD 116.5 million in operating cash flow during 2024, and ended the year with a net cash position of USD 74.9 million on its balance sheet (up from $44.4 million a year earlier). The equity ratio improved to a solid 72.4% of total assets, indicating a conservative capital structure with minimal debt. This financial strength gives Inficon flexibility to invest in R&D, fund dividends, and weather industry cycles.

Early 2025 results show a continuation of these trends. In the first quarter of 2025, sales grew about 2.7% year-on-year, with particularly strong demand in the semiconductor-related business. The Q1 gross margin improved further (nearly 49.4%), and operating margin held around 20%. Net profit for Q1 came in roughly flat year-on-year (just under USD 25 million for the quarter) as Inficon maintained its profitability despite some segments facing softer orders. The company confirmed its full-year guidance for 2025, anticipating USD 660–710 million in sales at around a 20% operating margin. In short, Inficon is entering 2025 on stable footing – revenue is holding near record levels, margins are strong, and the balance sheet is debt-light – positioning the firm to capitalize when its markets rebound.

Key financials

Business Model and Operations

Inficon’s business model centers on designing and selling highly specialized instruments that ensure quality and efficiency in manufacturing processes across several high-tech markets. The company’s product portfolio includes:

Gas leak detectors – e.g. helium and hydrogen leak detection equipment – used in manufacturing and servicing of refrigeration and air-conditioning systems, automotive components (fuel systems, airbag inflators, EV battery cooling systems, etc.), and even food & pharma packaging. Inficon has a long heritage here and is a market leader in refrigerant leak detection (with an estimated 70–80% market share in that segment). These products help customers meet safety and environmental regulations by quickly finding and fixing leaks of refrigerants or other gases.

Vacuum instrumentation and sensors – a broad category that includes vacuum gauges, residual gas analyzers, quartz crystal microbalance sensors, thin-film deposition controllers, and related process control software. These are mission-critical for semiconductor fabrication and other vacuum-based manufacturing. For instance, in a chip fabrication plant (fab), Inficon’s sensors monitor the vacuum chamber conditions and gas composition in real time, enabling precise deposition of materials and early detection of any contamination. Inficon supplies both the semiconductor end-users (chip manufacturers) and the equipment OEMs that build fabrication tools. In fact, Inficon is regarded as a top provider of process monitoring subsystems in the semiconductor industry, alongside only a few competitors like U.S.-based MKS Instruments. The company holds roughly 50% global market share in certain vacuum instrumentation niches (particularly for end-user semiconductor applications), underscoring its strong reputation in this field.

Environmental analysis and security devices – for example, Inficon produces portable mass spectrometers and gas chromatographs that can detect toxic chemicals or trace compounds on-site. These are used by emergency response teams, military organizations, and industrial safety departments for applications ranging from chemical warfare agent detection to monitoring of petrochemical facilities and environmental air quality. Inficon’s Security & Energy division, while the smallest of its segments, has developed a strong niche (reportedly ~90% market share in portable toxic gas detectors) by serving defense and government customers with specialized solutions. Although sales in this segment can be uneven (often driven by the timing of large government orders), it represents an important long-term opportunity given rising global focus on environmental safety and security.

Geographically, Inficon’s business is well diversified across major regions. In 2024, about 49% of sales came from Asia-Pacific (with China and other East Asian semiconductor hubs being key markets), 26% from North America, and 24% from Europe. This distribution reflects the global nature of the semiconductor and refrigeration industries. Inficon supports these markets via a global footprint: it operates manufacturing plants in Switzerland, Liechtenstein, the United States, and other locations, and maintains sales/service offices in countries like China, Japan, Korea, Taiwan, Germany, the UK, and more. This local presence and support network helps Inficon stay close to its customers – often embedding its engineers at customer sites – and respond quickly to their needs.

A core aspect of Inficon’s model is continuous innovation. The company invests heavily in research and development – roughly 7–8% of its annual revenue in recent years (USD 51.5 million in 2024 on R&D) – to keep its product offerings technologically ahead. Over its 25+ year history, Inficon has introduced over 100 new products, frequently upgrading its instruments to improve sensitivity, speed, and integration with modern manufacturing (such as compatibility with data analytics and “smart factory” systems). For example, Inficon’s latest helium leak detector models or fab monitoring software often incorporate advanced automation and user-friendly interfaces to help customers identify issues faster and reduce downtime. This emphasis on innovation builds customer loyalty – many top semiconductor manufacturers and OEMs (Samsung, TSMC, Intel, Applied Materials, etc.) rely on Inficon’s solutions as standard tools in their production and R&D processes. In essence, Inficon’s business model is to be the go-to “sensor and control specialist” for any company that runs high-precision vacuum processes or needs reliable gas detection. By excelling in these niches and providing excellent support, Inficon embeds itself deeply in customers’ operations, which can lead to recurring sales (replacement sensors, calibration services, software upgrades) and a defensible market position.

Strengths and Weaknesses

Like any company, Inficon has distinct strengths underpinning its success, as well as some weaknesses and risks to consider. Below is an analysis of the key positives and negatives:

Key Strengths

Leading Niche Market Positions: Inficon enjoys market leadership in its core niches, supported by proprietary technology and decades of know-how. It commands approximately half of the global market share in certain vacuum instrumentation segments for semiconductors, and an even higher share (estimated 70%+) in HVAC/refrigeration leak detection equipment. This dominance suggests a competitive moat in these specialized fields, where Inficon’s products are often considered the industry standard.

Diversified End-Market Exposure: The company serves a range of end markets – notably semiconductor manufacturing (~50% of 2024 sales), general industrial vacuum processes (~23%), refrigeration/air conditioning & automotive (~20%), and security & energy (~6%). This spread means Inficon isn’t solely reliant on one industry’s fortunes. For instance, even when general industrial demand softened in 2024, the semiconductor and security segments grew and helped offset that decline. Over a full cycle, strength in one area can counterbalance weakness in another, giving a measure of resilience.

Strong Profitability and Financial Health: Inficon consistently delivers high margins and returns. Its EBITDA margin has been above 20% in recent years, and 2024’s net profit margin reached nearly 17% – excellent for a manufacturing-focused business. Return on equity is also impressive (around 31% in the latest year). Furthermore, the company has very low debt (debt-to-equity only ~0.12) and has built a net cash position on its balance sheet. This conservative financial structure reduces risk and enables strategic flexibility (for example, Inficon can fund R&D, acquisitions, or dividends without heavy borrowing). Reliable cash flows (operating cash conversion has been strong, with free cash flow of $88 million in 2024) provide the fuel for continued investment and shareholder returns.

Continuous Innovation and R&D Excellence: A key strength of Inficon is its commitment to innovation. The company’s specialized focus has allowed it to become a technology leader in vacuum sensor and gas analysis. Customers value the performance and precision of Inficon’s products – e.g. its newest leak detectors or process monitors often outperform competitors in speed or sensitivity. Management highlights a strong pipeline of new products and “benchmark” solutions in development. This constant innovation (supported by ~8% of sales in R&D spending) helps maintain Inficon’s competitive edge and pricing power, as clients are willing to pay a premium for tools that improve their yield or safety.

Global Reach and Customer Proximity: Inficon’s worldwide presence is another strength. It can service multinational customers locally, whether a semiconductor fab in Taiwan or an automotive HVAC plant in Detroit. The company’s global network of technical support and applications engineers ensures it can respond quickly to customer issues or new requests. In an era of supply chain uncertainties and trade restrictions, Inficon’s manufacturing footprint on multiple continents also helps mitigate risk (the company notes it can adjust production between its U.S., European, and Asian facilities to navigate tariffs or export controls). This operational agility and customer-centric approach strengthen Inficon’s relationships and reputation in its markets.

Key Weaknesses (and Risks)

Cyclical End Markets (Semiconductor Exposure): A significant portion of Inficon’s business is tied to cyclical industries, especially semiconductors. Chip manufacturing equipment demand is famously volatile – it soars during industry upswings and contracts sharply in downturns. Inficon’s largest segment, Semi & Vacuum Coating, is roughly half of revenues. While this segment grew in 2024 despite a broader semiconductor slowdown, a prolonged downturn or delayed recovery in the chip cycle could hurt Inficon’s top line. The company itself acknowledges it is waiting for the next upswing in the semiconductor industry (expected in H2 2025) to drive growth. If that rebound is weaker or later than anticipated, Inficon’s growth may stall in the short term. Similarly, other end markets like automotive and general industrial vacuum tend to follow economic cycles – for example, Inficon’s sales to “General Vacuum” customers dropped over 20% in 2024 amid a global industrial slowdown. Investors must be prepared for this revenue volatility over the cycle.

Lumpy Orders in Smaller Segments: Inficon’s smaller divisions, particularly Security & Energy (~6% of sales), can see irregular demand because they depend on large project orders (often government or military related). A big government contract can boost this segment one quarter, then the next quarter might drop off. Indeed, Inficon noted a 27% year-on-year decline in Security & Energy sales in Q1 2025, attributing it to the timing of public sector orders. This lumpiness can add noise to overall results and make short-term forecasting difficult. While not a huge portion of total sales, it’s a factor that can create quarterly volatility.

Competition and Technological Disruption: While Inficon is a leader in its niches, it does face competition from several capable firms, including some larger players. In semiconductor process control, MKS Instruments (USA) is a direct competitor with a broad product lineup and greater scale in some areas. Other competitors across Inficon’s divisions include Agilent (which took over Varian’s vacuum tools), Japan’s ULVAC, as well as smaller specialized sensor makers. A risk is that a competitor could develop a new technology that leapfrogs Inficon’s solution or aggressively undercuts pricing to gain share. Inficon’s strategy of high-performance, high-quality products means it doesn’t usually compete on the lowest price, so it must ensure its technology remains sufficiently superior to justify the premium. There’s also the risk that customers (especially large OEM clients) might try in-house development of sensors or source from multiple suppliers to reduce dependency on Inficon. So far, Inficon has managed to stay ahead, but continual innovation is required in these fast-evolving tech markets.

Moderate Size and Talent Retention: Inficon is relatively small (around 1,700 employees and $670 million revenue) compared to some multi-billion-dollar industrial conglomerates. This moderate size can be a weakness in that resources are more limited – for instance, R&D budget, salesforce reach, and ability to weather multiple large projects at once. The company needs to carefully prioritize where it focuses its innovation efforts. Additionally, in cutting-edge fields like sensors and software, attracting and retaining top engineering talent is critical. Inficon’s size and niche focus mean it must compete with bigger tech firms for skilled personnel. Any loss of key talent or know-how could impact its innovation pipeline. The company does appear to have a stable team and has been successful in its recruiting (leveraging its high-tech appeal and global presence), but it’s an area to watch as a potential vulnerability.

In summary, Inficon’s strengths – such as its leading technology, diverse applications, and financial solidity – make it a high-quality business, but investors should be mindful of the cyclical and competitive forces that could pose challenges.

The valuation stock list has been available online since tonight. You can find it here:

Get an information edge with our ever-evolving dashboard of proprietary intrinsic-value estimates and Quality Scores across a broad universe of equities.

Why it matters

Actionable numbers, not hype. Every fair-value range is built from my in-house DCF and comparable-multiple models, so you can see at a glance where price diverges from worth.

Breadth and depth. You’ll find every company featured in my deep-dive Substack articles — plus a growing roster of great names I’m tracking privately.

Always up to date. Valuations are reviewed at least once a year (often sooner when fundamentals shift), new tickers are added as ideas surface, and low-conviction names are removed.

Plus, you will have full access to all the deep dives and additional valuable content!

Keep reading with a 7-day free trial

Subscribe to Kroker Equity Research to keep reading this post and get 7 days of free access to the full post archives.