#111 Three under-the-radar US small-caps

From the Ranch to the Rack: Three Tiny Titans Hiding in Plain Sight

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is not invested in the mentioned stock.

*Affiliate link – Get 15% off Fiscal.ai (formerly Finchat)

Introduction

When you picture market-beating innovation, you probably think of AI chips, space tourism, or gene-editing—not cowboy boots, eggs, and protein powder. Yet that’s exactly where today’s hunt for quality led me. I ran my usual screen—clean balance sheets, double-digit returns on invested capital, durable mid-teens revenue growth, and insider ownership—across the entire U.S. small-cap universe. The output surfaced dozens of flashy tickers, but what grabbed my attention were three companies whose day-to-day operations feel almost old-fashioned: selling western wear, pasture-raised eggs, and niche sports-nutrition brands.

Why spotlight businesses that seem, at first glance, almost “boring”? Because dull often equals dependable. Companies with straightforward value propositions, sticky customers, and defensible supply chains can quietly compound capital while the market chases shinier objects. As macro volatility whipsaws sentiment, these steady growers keep stacking cash, opening new stores, and deepening retail and distribution relationships—with far less fanfare than their tech-heavy peers.

In this post I’ll break down Boot Barn Holdings (western apparel retailer riding a store-growth and private-label wave), Vital Farms (category-defining leader in ethically produced eggs and butter), and FitLife Brands (micro-cap roll-up carving out a profitable niche in gym supplements). We’ll look at how each scores on quality metrics, where their moats sit, and what catalysts could push them into the market’s spotlight. If you’ve ever wondered how “simple” business models can deliver anything but simple returns, read on.

Boot Barn Holdings (BOOT)

General overview

Boot Barn Holdings, Inc.* is the largest U.S. lifestyle retailer specializing in western- and work-related footwear, apparel and accessories. Founded as a single store in 1978, today Boot Barn operates over 400 stores across 45+ states. The company sells major brands like Ariat, Justin, Wrangler and Carhartt, along with its own private labels. Its omni-channel model includes brick-and-mortar stores (average ~10,900 sq. ft.) and an e-commerce platform (bootbarn.com plus sites like sheplers.com and countryoutfitter.com). Boot Barn targets a broad customer base – from country/rodeo enthusiasts to blue-collar workers – and emphasizes exclusive high-margin brands in its assortments.

Recent Financial Results

Boot Barn closed its fiscal year 2025 on a strong note, delivering impressive growth across key financial metrics. Net sales reached $1.91 billion, up 14.6% year-over-year, driven by a 5.5% increase in same-store sales. This included a 5.0% rise in retail store comps and a strong 9.7% growth in e-commerce. Gross profit came in at $717 million, with a margin improvement of 70 basis points to 37.5%. Net income rose by 23% to $180.9 million, and diluted earnings per share climbed to $5.88, up 22% from the prior year. Operating margin also improved by 60 basis points, reaching 12.5%.

The company opened 60 new stores during the year, bringing the total store count to 459. Inventory per store increased by 5.7%, reflecting broader product assortments. Notably, Boot Barn ended the year with $70 million in cash and no borrowings on its $250 million revolving credit facility, highlighting its strong financial position.

Performance was fueled by higher customer traffic and larger average transaction sizes. Merchandise margin gains—driven by better product mix, stronger exclusive brand performance, and improved inventory shrink—more than offset higher occupancy costs. At the same time, Boot Barn kept SG&A expenses steady at 25% of sales despite the rapid store expansion, helping convert more gross profit into bottom-line earnings.

CEO John Hazen summed it up by saying that 15% sales growth and 23% EPS growth reflect the strength of their business model and the loyalty of their core customers, even in a challenging macroeconomic environment.

Looking ahead, the company approved a $200 million share buyback program and plans to open 65–70 new stores in fiscal 2026. While same-store sales are expected to be flat to slightly positive, management still projects total revenue growth of around 10%, with earnings per share roughly in line with FY 2025. The clean balance sheet gives Boot Barn flexibility to continue investing in growth while returning capital to shareholders.

In short, FY 2025 was a highly successful year for Boot Barn. The company grew faster, operated more efficiently, and remained financially disciplined. With a robust store pipeline and a focus on long-term growth, it’s well-positioned heading into FY 2026—even if comparable sales cool off somewhat.

Business Model & Strategy

Boot Barn’s business model centers on a niche lifestyle retail concept. Its two segments – physical stores and online – carry a full array of western and work gear. Store merchandising is a core part of the model: boots are the signature category (displayed by size or function) and sales associates provide a hands-on shopping experience. Stores are typically free-standing or in prominent strip centers and average ~10,900 sq. ft..

To broaden its appeal, Boot Barn carries exclusive private brands (e.g. Shyanne, Cody James, Moonshine Spirit, Cleo + Wolf, etc.) alongside third-party labels. These house brands target under-served price segments and yield higher margins than national brands. The company has explicitly focused on growing exclusive-brand sales: FY2024 saw exclusive penetration jump ~370 basis points (helping margin).

Boot Barn’s growth strategy emphasizes store expansion and omni-channel synergy. Management believes the U.S. market can ultimately support ~900 stores (vs ~400 today). In FY2024 it opened 55 new stores; Q1’25 added 11 more; guidance calls for ~60 openings in FY2025. Geographic expansion is into both new states (45 states served to date) and denser coverage in existing markets. Supporting this, Boot Barn has invested in larger distribution centers and IT systems to enhance its omnichannel platform. The Sheplers and CountryOutfitter acquisitions (added as dedicated e-commerce channels) further extend the brand online and into related demographics.

Revenue is roughly 60–70% from in-store sales and 30–40% online (e-commerce sales have been a faster-growing component). Merchandise categories mix footwear (boots, work shoes), apparel (denim, outerwear, casual wear) and accessories (belts, hats, jewelry, work-gear). Average transaction size is higher in-store, but online sales have higher growth rates. The company emphasizes a “low promotional” pricing strategy and a curated product mix to protect margins. In summary, Boot Barn operates a lean, specialty-retail structure: specialty-buying of western/workwear, predominantly leased stores, centralized inventory and logistics, and aggressive expansion plans in a growing niche.

Strengths and Weaknesses

Strengths: Boot Barn’s key strengths include its market leadership and scale in its niche. It has far more western/work stores than any competitor, giving it buying power and broad brand visibility (465 stores as of mid-2025). Its exclusive brands and supply-chain efficiencies are boosting gross margins. A growing loyalty base and affinity for “cowboy lifestyle” fashion give it a somewhat insulated niche. The balance sheet is also a plus: total debt is minimal (~$14M in FY2025, down from $82M in FY2023), implying little financial leverage risk and capacity to invest or repurchase stock.

Weaknesses: On the flip side, Boot Barn faces some challenges. As a discretionary retailer, it is vulnerable to consumer spending cycles and weather-related foot traffic. Same-store sales have been uneven: for example, FY2024 saw comps fall –6.2%. (The weakness was notably higher in women’s apparel and e-commerce.) The company carries inventory risk – unsold seasonal merchandise can press margins – and depends on favorable weather and events (rodeo, fairs) to drive store traffic. Fashion trends (especially in women’s and casual wear) can be fickle, so product selection must keep pace. There is competitive pressure, too: other apparel retailers, farm-and-ranch stores, and online marketplaces may compete for similar customers. Finally, Boot Barn’s rapid expansion itself poses risk; opening ~15% more stores per year requires execution (real estate, staffing) and could ultimately saturate local markets if growth overshoots demand.

In summary, Boot Barn’s strengths are its focused niche strategy, broad store network, and improving margins. Its weaknesses include cyclical same-store sales and the inherent risks of fast retail expansion.

Dividends and Buybacks

Boot Barn does not pay a cash dividend; its reported dividend yield has been 0%. Management prefers share repurchases when returning cash to investors. In May 2025, the board authorized a $200 million stock buyback – roughly 40% of current market cap. This ongoing repurchase plan has no expiration date and can be executed via open-market purchases, accelerated programs, etc.. The size of this buyback (relative to cash flow) signals confidence by management in the firm’s future free cash generation. To date, Boot Barn has repurchased stock opportunistically (including under previous authorizations, although details are not fully public). Overall, shareholders should anticipate capital return in the form of buybacks rather than dividends.

Valuation

Boot Barn trades on the New York Stock Exchange under the ticker BOOT, and its International Securities Identification Number (ISIN) is US0994061002 . As of mid‑June 2025, there are approximately 30.59 million shares outstanding, of which around 30.47 million are free‑floating, with insiders holding less than 1 %. The company’s market capitalization hovers near US $5.0 billion, reflecting its stock price of about US $163 per share.

Boot Barn is commanding a premium valuation today. The stock trades at roughly 28 times trailing diluted earnings per share and about 23 times trailing EBIT on an enterprise-value basis. Both multiples sit well above their own three-year averages (around 18× for the P/E and 15× for EV/EBIT) and are closer to the upper end of the historical range than the lower. In absolute terms, that places Boot Barn among the most richly priced specialty apparel retailers and implies the market is willing to pay up for its expansion runway and durable margins.

What’s embedded in those numbers? First, investors clearly expect the double-digit top-line growth and margin gains of the past few years to continue—or at least not roll over. Second, the company’s net-cash balance sheet means there is no leverage masking weaker underlying returns; the valuation is being carried by the operating fundamentals alone. At these levels, the stock offers an earnings yield of a touch above 3½ % and an EBIT yield just north of 4 %, so the path to further upside likely hinges on sustained comparable-store growth, successful new-store rollouts, and continued merchandise mix improvement.

In short, Boot Barn is priced for ongoing outperformance. If management can keep expanding its store base while defending the industry-leading margins it has built, the premium makes sense. If growth or profitability stumbles, however, the multiple has room to compress back toward its mid-teens historical norms. For prospective investors, it’s a classic “prove-me-right” valuation: execution will have to stay as sharp as a pair of new cowboy boots.

Investment Case

Bullish case: An investor might buy and hold BOOT expecting continued execution of its long-term strategy. Key reasons include: robust growth potential – both from new store openings and expansion of online sales – as Boot Barn still has only about half of its 900-store potential. Management’s guidance (FY2025 sales +9–11%, EPS ~$5.20) implies mid-single-digit comp growth and healthy new-store lift. The company’s focus on exclusive brands and inventory management may further expand margins (we saw +370 bps in gross margin FY2024). The $200M share repurchase is a catalyst, as reducing share count boosts EPS. Finally, the niche “western lifestyle” market has favorable tailwinds (popularity of country culture, safety/regulations boosting workwear). If the U.S. consumer remains reasonably healthy, Boot Barn’s affinity brand and diversification of channels could drive solid earnings growth. Institutions like Baird and Citi even see $122–$167 share price targets (Nov 2024 analysts’ consensus) and upgrades on robust results.

Bearish case: An investor cautious on BOOT would point to risks and valuation. First, the company’s recent same-store sales have been erratic – FY2024 comps fell – and depend on discretionary spend. If the economy weakens or inflation keeps consumers on budget, Boot Barn could see traffic and spending soften. Second, its valuation leaves less margin for error. A P/E ~27× means that any earnings shortfall (e.g. from weaker guidance or promotional price cuts) would disappoint investors. Third, the retail environment is competitive: from general apparel chains to online retailers. Tariff pressures (it sources merchandise globally) or supply-chain hiccups could raise costs. Finally, aggressive expansion could backfire: if new stores cannibalize older ones, or if leases turn unfavorable. In summary, bearish arguments focus on cyclical retail risk, high valuation, and execution uncertainties. (Industry analysts have flagged threats like macro consumer risk, market saturation potential, and the challenge of scaling up new stores.)

Outlook

Looking ahead, Boot Barn’s business is shaped by both industry and macro trends. The western and workwear market is generally expected to grow modestly. Factors like rodeo/country music popularity, a trend toward casual “cowboy chic” fashion, and strong construction/manufacturing employment all underpin demand. Additionally, workplace safety regulations drive continual sales of safety boots and gear (e.g. steel-toe boots, Hi-Vis clothing). On the flip side, general retail headwinds (e-commerce competition, rising costs, consumer budget pressures) are industry-wide trends to watch.

Boot Barn’s roadmap has shifted from “beat-and-raise” in FY 2025 to a more tempered—but still growth-oriented—outlook for FY 2026. Last year, management’s playbook called for roughly 60 new stores, high-single-digit revenue growth and a modest EPS lift. In the end they hit the store target and overshot the financials: net sales climbed 14.6 % to $1.91 billion, same-store sales rose 5.5 %, and diluted EPS reached $5.88—comfortably above the original $5.05–$5.35 range.

Looking ahead to FY 2026 (ending March 2026), guidance is built around steady expansion but assumes a cooler consumer backdrop:

New stores: 65–70 openings, roughly 15 % unit growth.

Total revenue: $2.07–$2.15 billion, implying 8–13 % topline growth.

Same-store sales: a corridor of –2 % to +2 %, reflecting caution after three strong years.

Diluted EPS: $5.50–$6.40, essentially flat to a modest up-year, with management flagging roughly $8 million in potential tariff headwinds for the back half.

The board has also re-loaded capital-return firepower with a $200 million share-repurchase authorization, signalling confidence even as macro uncertainty and higher input costs temper near-term expectations.

Boot Barn just proved it can out-execute its own forecasts; FY 2026 guidance resets the bar lower but keeps the growth engines—store openings, margin discipline, and buybacks—firmly in gear. Execution, as always, will determine whether the stock’s premium multiple stays snugly fitted or slips a notch.

Macro factors: Continued low unemployment and moderate inflation would help discretionary retailers like Boot Barn. Conversely, any sharp slowdown in consumer spending or spike in interest rates could tighten sales. Given its Texas headquarters and many rural stores, regional economic shifts (e.g. in the heartland states) may impact Boot Barn differently than coastal retailers. Overall, industry analysts view Boot Barn as well-positioned for moderate growth, assuming the U.S. economy avoids a severe downturn.

Conclusion

For long-term investors, Boot Barn presents a mix of strengths (niche leadership, growth runway, improving profitability) and cautions (cyclical sales, valuation premium). On the plus side, the company has demonstrated resilience and adaptability: it navigated the pandemic downturn, integrated acquisitions, and is executing a clear growth plan. Its focus on exclusive brands and digital channels bodes well for margin expansion. The substantial buyback authorization also indicates management is committed to shareholder value. However, investors should be mindful that much of the positive outlook is already in the stock price, and the business remains sensitive to consumer spending trends.

In sum, Boot Barn’s investment potential hinges on continued execution. At current valuation levels (mid-20s P/E), the stock offers upside if the growth story holds, but limited protection if there is a miss. Long-term holders who believe in the Western/workwear lifestyle theme and Boot Barn’s expansion strategy may see attractive returns – especially given the absence of dividend (returns come via buybacks and share gains). Bearish investors will focus on the high P/E and potential for a consumer slowdown. Ultimately, Boot Barn is a specialty retail play: best suited for investors comfortable with consumer cyclicality but attracted by high growth niche retail stories.

Vital Farms (VITL)

General overview

Vital Farms, Inc.* is a specialty food company known for its ethically produced pasture-raised eggs and butter, sold nationwide. Founded in 2007 in Austin, Texas, Vital Farms operates as a public benefit and Certified B Corporation, emphasizing animal welfare and sustainable farming. Its core products – shell eggs, butter, plus specialty items like hard-boiled and liquid eggs – come from a network of over 425 family farms. Each farm follows strict “pasture-raised” standards (hens have ~108 sq. ft. outdoors each). The company collects eggs from these farms, transports them to its large Springfield, Missouri packing facility (Egg Central Station, ~6 million eggs/day capacity), and sells finished products to retailers. Vital Farms has leveraged its mission-driven brand to expand from natural-food stores (Whole Foods, Sprouts) into mainstream supermarkets (Kroger, Target, Walmart, etc.). In 2024 its products were sold in roughly 24,000 stores nationwide.

Recent Financials

Vital Farms has delivered strong revenue growth and improving profits in recent years. For fiscal 2024 (year ended Dec 29, 2024), net sales were $606.3 million, up 28.5% from $471.9M in 2023. Gross margin expanded sharply (to ~37.9% from 34.4%), driving net income of $53.4M (versus $25.6M in 2023) and EPS of $1.18. Adjusted EBITDA roughly doubled to $86.7M. Notably, fourth-quarter 2024 revenue hit $166.0M (a like-for-like 30% increase), and Q4 net income was $10.6M (EPS $0.23).

Early 2025 results have stayed on this growth trajectory. In Q1 2025 (ended Mar 30), Vital Farms reported $162.2M revenue (up 9.6% year-over-year) with net income of $16.9M (EPS $0.37). Management reaffirmed full-year 2025 guidance of $740M in sales and $100M in Adjusted EBITDA, aiming for its goal of ~$1 billion in revenue by 2027. Highlights from these results include 20 consecutive quarters of year-over-year growth and rising brand awareness (butter sales jumped 41% in Q1 2025).

2024 vs 2023: 28.5% sales growth ($606.3M); net income +109% ($53.4M); Adj. EBITDA +80% ($86.7M).

Q4 2024 vs Q4 2023: Revenue $166.0M (≈+22% reported; +30% on equal weeks); Gross Margin ~36.1%; Net income $10.6M (up +47%).

Q1 2025 vs Q1 2024: Revenue $162.2M (up 9.6%); Gross Margin 38.5% (slightly down); Net income $16.9M (down from $19.0M prior year).

These results show robust top-line growth and improving operating leverage, though short-term profit margins can fluctuate as Vital Farms invests in growth (crew members, new farms, etc.).

Business Model and Operations

Vital Farms’ business model centers on a certified network of family farms and a direct-to-retail supply chain. Key points:

Product mix: Vital Farms’ flagship products are shell eggs (pasture-raised), which account for roughly 93–95% of net revenue. Secondary products include premium butter, ready-to-eat hard-boiled eggs, and liquid whole eggs (one of few pasture-raised offerings in that category). Butter and other non-egg products make up a smaller (~5–7%) but growing portion of sales.

Supply chain: The company contracts with family-run farms in the U.S. “Pasture Belt.” These farmers raise hens on pasture and manage daily operations (buying feed, birds, etc.), while Vital Farms provides logistical support and agrees to purchase all eggs produced under contract. This buy-sell model aligns incentives but commits Vital Farms to supply costs. As of end-2024, Vital Farms had ~425 farms (adding ~125 new farms in 2024). The company is expanding capacity: it already has the Egg Central Station in Missouri and is building a second egg-processing plant in Indiana (expected online ~2027) to handle more volume.

Distribution: After collection, eggs are transported to Vital Farms’ facilities for grading and packaging. The finished products are sold to grocery retailers and foodservice distributors. Vital Farms commands premium pricing and is present in both the natural/organic channel and mainstream supermarkets. The company offers ~23 SKUs across its lines and continues to explore new product innovations.

Differentiators: Vital Farms distinguishes itself through ethical branding and quality. It follows strict Certified Humane and B Corp standards, emphasizing animal welfare and clean ingredients. The transparent, mission-driven image has created loyal customers and strong shelf-velocity (shoppers prefer its taste and values). Its origin story (single farm startup) and public benefit status reinforce the narrative of “ethical food at scale.” These factors allow Vital Farms to maintain premium margins relative to commodity eggs.

Strengths and Weaknesses

Strengths:

Growing, Ethical Brand: Vital Farms is a recognized leader in pasture-raised eggs and one of the fastest-growing food brands, leveraging increasing consumer demand for “better” and traceable foods. It holds a low ~9% household penetration for its eggs (vs ~97% for eggs overall), indicating room to expand.

Strong Financial Growth: It has delivered ~30% annualized sales growth since 2020 and rapidly expanding profits. In 2024 net income more than doubled, showing operating leverage as volumes rise. The balance sheet is healthy (low debt: D/E ~0.07, strong current ratio ~3.3) with positive cash flows to fund expansion.

High Barriers via Supply Chain: Its vetted network of family farms and proprietary processing give it a reliable supply of high-quality eggs. New initiatives like “accelerator farms” (company-owned model farms) aim to further strengthen this moat.

Diversified Channels & Innovation: Presence in multiple retail and foodservice channels, plus product expansion into butter and prepared eggs, provides diversification. The company continues innovating (e.g. heirloom blue eggs, regenerative-restorative egg line) to attract more consumers.

Weaknesses/Risks:

Product Concentration: Vital Farms relies heavily on eggs: about 93–95% of revenue comes from shell eggs. Any disruption or demand swing in that one category could impact results. The company’s success hinges on continuing to expand other lines (butter, liquid eggs) to lower this concentration.

Premium Positioning: As a premium brand, Vital Farms is sensitive to commodity egg pricing and economic cycles. If conventional egg prices fall sharply, consumers might trade down, and retailers could pressure price points. Conversely, feed cost inflation or disease outbreaks (HPAI, EDS) can raise Vital Farms’ input costs or constrain supply. The 2024-25 surge in bird flu boosted overall egg prices and may benefit Vital Farms in the short term, but it also poses risks if outbreaks hit its farms.

Internal Controls: Management disclosed a material weakness in financial controls (revenue recognition processes) for 2024. Although no restatements were required and remediation is underway, such issues could distract management or undermine confidence if not fixed promptly.

Valuation Risk: The stock trades at high multiples, implying considerable execution is priced in (see below). If growth moderates, the shares could underperform.

Lack of Payouts: Vital Farms does not pay dividends (last and only dividend was a one-time 2013 payout of $0.3M) and has no announced buyback program. All cash is plowed into growth, which investors should note.

Dividends and Buybacks

Vital Farms has historically not returned cash to shareholders. Aside from a one-time small dividend in 2013, the company has paid no dividends and does not expect to in the foreseeable future. The board explicitly states it intends to reinvest all earnings to fund expansion. There is likewise no active share buyback program. Long-term investors should consider Vital Farms a growth stock with no current income distribution.

Valuation

Vital Farms, Inc. trades on the NASDAQ under the ticker VITL, with ISIN US92847W1036. As of mid‑June 2025, the company has about 44.5 million shares outstanding, with roughly 33.8 million shares in public float. That puts its market capitalization around US $1.6 billion.

Vital Farms trades at a high growth multiple. As of mid-2025, its trailing P/E ratio is on the order of 30× earnings, and its EV/EBIT (enterprise value to operating profit) is roughly 22×. For context, this is expensive compared to large food companies (Pepsi ~20x PE, Nestlé ~20x, etc.), reflecting high growth expectations. In other words, the market is valuing Vital Farms as a fast-growing tech-style company rather than a mature grocer. Investors must believe in continued double-digit top-line growth and margin expansion to justify this valuation.

Investment Case

Bull Case: Supporters point to Vital Farms’ strong growth runway and brand momentum. The egg category is undergoing a shift toward cage-free and premium offerings; Vital Farms is positioned as a leader in this trend. It has an impressive growth track record (three-year CAGR ~28.5%) and guidance suggests ~20%+ revenue growth in 2025. Analysts note expanding distribution and narrowing price gaps with conventional eggs as near-term tailwinds. The company’s 2027 $1B revenue target (also echoed by management) implies continued acceleration. Vitl Farms also just raised supply capacity (adding farms, new lines), setting the stage for higher volume. Wall Street is mostly positive: Morgan Stanley initiated coverage with an “Overweight” rating (implying ~3.5:1 upside vs. downside), and multiple brokers (Stifel, DA Davidson, Jefferies, etc.) have Buy ratings with price targets in the low $40s, citing solid guidance and expanded capacity. In summary, the bull case rests on sustained premium growth in a large market, successful scale-up of operations, and continued margin improvement.

Bear Case: Skeptics worry Vital Farms’ valuation and execution risks. The stock is up and down with retail trends; for example, year-to-date it is down ~20% even after the rally, suggesting volatility. If Vital Farms fails to meet its aggressive growth assumptions, multiples could contract. Key risks include crop disruptions or animal diseases impacting egg supply (Vital Farms has noted this as an uncertainty), as well as commodity price swings that squeeze margins or consumer demand. The company remains mostly egg-focused, so any slowdown in the category (or if organic/premium growth stalls) would hurt. Additionally, the recently disclosed accounting weakness raises governance concerns, and the company has to prove it can implement more controls without derailing operations. Larger competitors could also intensify pressure: Cal-Maine Foods and conventional producers have far greater scale and could respond to Vital Farms’ success by expanding their own cage-free offerings or cutting prices. From an investor’s viewpoint, the bear case is that a disappointments in sales growth, rising costs, or missteps in scaling the business would lead to a sharp pullback, given the rich valuation.

Outlook

Looking ahead, Vital Farms’ prospects hinge on industry trends and its own expansion strategy. Consumer demand for ethical, clean-label foods appears robust: major retailers have announced cage-free egg commitments, and awareness of animal welfare is rising. This should favor Vital Farms’ offerings. The company’s guidance and commentary suggest that growth may accelerate in late 2025 once recent supply constraints ease. Management believes investments made in 2024–25 (new farms, processing lines, marketing) will “begin bearing fruit” in the back half of the year. If it hits its targets, Vital Farms could deliver mid-20% sales gains in 2025 and beyond.

However, several external factors warrant watching. Inflation and higher interest rates could curb consumer spending; input costs (feed, packaging) remain volatile. Also, maintaining its mission-driven image is crucial – any slip in animal welfare standards or sustainability claims (especially as a Certified B Corp) could harm the brand. On the positive side, Vital Farms has financial flexibility, and its debt is low (bank facility vs. cash), which should allow it to continue expanding. Overall, if demand for premium egg products stays strong and Vital Farms executes its capacity expansion smoothly, the company should sustain healthy growth.

Conclusion

Vital Farms is a unique food-growth story: it has a strong mission-driven brand, a compelling growth track record, and an experienced management team. Its financials show accelerating sales and profit gains, and the company is on track to achieve $1 billion in revenue within a few years. For long-term investors, the key attractions are the secular trends toward ethical and premium foods, and Vital Farms’ leading position in that niche.

However, investors must weigh these against the risks. The stock trades at lofty multiples (P/E ~30×, EV/EBIT ~23×), meaning expectations are very high. Vital Farms is still relatively small and closely tied to the volatile egg market. Any setback in growth, supply, or margins could materially impact returns. Additionally, with no dividend or buybacks, shareholders rely solely on appreciation.

Vital Farms is best-suited to investors who are optimistic about premium food trends and can tolerate some volatility. The company’s progress toward its growth targets (2025 guidance of $740M sales, 2027 $1B goal) and its ability to scale production while preserving brand trust are critical. Long-term, if Vital Farms continues to expand retail presence and innovate, it could reward patient investors with above-market returns. Conversely, those worried about valuation or commodity risks might be cautious. In either case, Vital Farms’ journey reflects a bet on conscious consumerism and the execution of a mission-driven strategy.

FitLife Brands, Inc. (FTLF)

General Overview

FitLife Brands, Inc.* is a small-cap nutritional supplements company based in Omaha, Nebraska. It markets a portfolio of over 100 proprietary supplement and wellness products under multiple brand families. Its flagship lines include sports and weight-loss products sold as NDS Nutrition, PMD Sports, SirenLabs, Core Active and Metis Nutrition, plus the iSatori brands (including BioGenetic Laboratories and Energize). In 2023–24 FitLife expanded via acquisition: it purchased Mimi’s Rock Corp. (MRC) in early 2023 – adding the Dr. Tobias, All Natural Advice and Maritime Naturals brands – and in late 2023 it acquired the MusclePharm sports-nutrition brand. These moves broadened FitLife’s product mix and added well-known branded portfolios. FitLife’s products are sold through a mix of channels: largely direct-to-consumer e-commerce (including its website and Amazon) and select wholesale/retail partners. For example, FitLife has long distributed NDS products via GNC (General Nutrition Centers) franchises and corporate stores, while iSatori products go through specialty/mass retail and online, MRC products are sold primarily on Amazon, and MusclePharm is sold both to wholesalers and online.

Recent Financials

FitLife’s growth accelerated in 2024. In FY2024 (year ended Dec 31, 2024) total revenue was $64.5 million, up about 22% from ~$52.7 M in 2023. Online sales dominated (67% of revenue, ~$43.0 M), helping drive a strong gross margin of 43.6% (versus 40.7% in 2023). Operating leverage kicked in: FitLife reported about $28.08 M gross profit on $64.47 M revenue, and after SG&A and other expenses earned roughly $9.0 M net income in 2024. This was a 70% jump from $5.3 M in 2023, translating to $0.98 basic EPS ($0.91 diluted) versus $0.59/$0.54 prior-year. Adjusted EBITDA also grew robustly – about $14.1 M in 2024, up ~39% YoY – thanks to margin expansion and cost control. The balance sheet is modestly leveraged: term loans stood at ~$13.1 M (all long-term after Dec 2024) with ~$4.5 M cash, for net debt around $8.6 M (about 0.6× trailing EBITDA).

Q1 2025: In the first quarter of 2025, revenue was $15.9 M, about 4% lower than Q1 2024. Online sales remained 67% of that, and gross margin dipped slightly to ~43.1%. FitLife earned ~$2.0 M net income in Q1’25 vs $2.2 M in Q1’24. (Adjusted EBITDA Q1’25 was ~$3.4 M.) Management noted that some one-time M&A-related costs weighed on Q1 results, but underlying contribution (gross profit minus marketing) was solid. In sum, FY2024 finished on a strong note with improving profitability and cash flow; Q1 2025 was roughly flat YoY in sales and profits.

Business Model & Strategy

FitLife’s business hinges on supplement innovation and brand marketing in a growing health & wellness market. It sells performance, weight-loss, general health supplements developed in-house and through acquisitions. The company generally outsources production to FDA-regulated contract manufacturers, then markets its branded products across channels. Major segments include:

NDS Nutrition Brands: Core weight-loss and sports-nutrition products (e.g. protein powders, meal replacements, pre-workouts) sold mainly through GNC franchise stores and GNC’s corporate stores. FitLife supplies ~700 GNC franchisees plus >1,400 GNC-owned stores. GNC remains a key wholesale partner.

iSatori Portfolio: Includes energy and weight-management supplements (Energize, iSatori, BioGenetic Labs), sold through fitness specialty stores, big-box retailers, and online.

Mimi’s Rock (MRC) Brands: Acquired Feb 2023, these are general wellness supplements (Dr. Tobias multivitamins, etc.) and natural beauty products (All Natural Advice, Maritime Naturals). These are sold mainly via e-commerce platforms like Amazon, as well as FitLife’s own DTC webstores.

MusclePharm: Acquired in Oct 2023, this is a well-known sports-nutrition brand selling protein and performance products. It sells to gyms and nutrition stores (wholesale) and online direct.

Distribution: In practice, direct-to-consumer sales dominate FitLife’s revenue. In 2024 roughly 67% of sales were online (own websites and Amazon). The rest comes via retail/wholesale: GNC is the largest single partner (23% of 2024 sales), plus smaller retailers (specialty chains, some grocery/club channels), and international distributors. The online focus is a strength given consumer e-commerce trends, while the GNC channel provides scale in brick-and-mortar stores.

Key revenue drivers include: new product launches and brand cross-selling (FitLife often bundles or cross-promotes its brands on Amazon), expanding its e-commerce marketing, and acquisitions that add new customer bases. The company continually develops new formulas (e.g. expanding its Metis Nutrition line in 2024) and leverages Amazon’s platform (FitLife says ~66% of sales flowed through Amazon in 2024). In essence, FitLife monetizes health trends (aging population, preventive health) by selling targeted nutrition products, primarily to health-conscious consumers shopping online and at supplement stores.

Strengths and Weaknesses

Strengths:

Robust Growth and Profitability: FitLife has delivered double-digit revenue growth (22% in 2024) and improving profit margins. It turned consistently profitable in recent years, reaching about 14% net margin in 2024. High gross margins (mid-40s) and disciplined SG&A keep operating margins strong.

Large Online Presence: Two-thirds of sales come via online channels. This allows higher margins and broad reach. FitLife ranks among the larger supplement sellers on Amazon and owns its customer data from direct web sales.

Diverse Brand Portfolio: Through organic development and acquisitions, the company covers multiple segments (sports, wellness, beauty). The addition of MusclePharm and Dr. Tobias/All Natural Advice has meaningfully expanded market footprint. Brand recognition in niche categories helps drive repeat sales.

Financial Strength: Low leverage (net debt ~0.6× EBITDA) and healthy cash flows give flexibility. No substantial near-term debt maturities – most term loans are 2028-2030. Strong 2024 cash generation should fund reinvestment or M&A.

Weaknesses and Risks:

Customer Concentration: FitLife is heavily dependent on a few sales channels. About 66% of revenue runs through Amazon and ~23% through GNC’s distribution. Any adverse change on Amazon’s platform (policy shifts, competition, account issues) could sharply affect sales. Similarly, if GNC were to delist FitLife products, it would remove a large chunk of wholesale revenue.

Competitive Market: The supplement industry is crowded. FitLife’s competitors include both large national brands and private-label retailers. Competitors often have greater marketing budgets or broader product lines, which can pressure prices and market share. FitLife must continuously innovate products and marketing to stay ahead.

Integration Risk: Recent acquisitions (MRC, MusclePharm) pose execution risk. FitLife must integrate supply chains, branding, and IT systems. Early costs or missteps could temporarily drag margins (reflected in elevated M&A expenses in Q1’25).

Regulatory and Supply Risks: Although not a major FDA issue, the supplement industry faces ongoing regulatory scrutiny (ingredient standards, labeling). FitLife relies on third-party manufacturers; any supply disruptions or quality issues could hurt production.

No Dividend/Repurchases: FitLife currently returns no cash to shareholders (see next section). Investors seeking income may be disappointed.

Dividends and Share Buybacks

FitLife does not pay any cash dividend and has never done so. The company’s policy is to reinvest earnings in growth (product development, marketing, acquisitions) rather than distributions. For example, the 2024 10-K explicitly notes: “We have never paid cash dividends on our Common Stock and do not anticipate paying any… in the foreseeable future.”.

FitLife has authorized a modest share repurchase program (up to $5.0 M of stock) for a 24-month period (extended in 2023). However, no repurchases were made in 2023 or 2024 under this authorization. The repurchase authorization remains unused (as of Dec 31, 2024 there is up to $5M still available). In practice, FitLife management appears to prefer using cash for operations and acquisitions over buybacks.

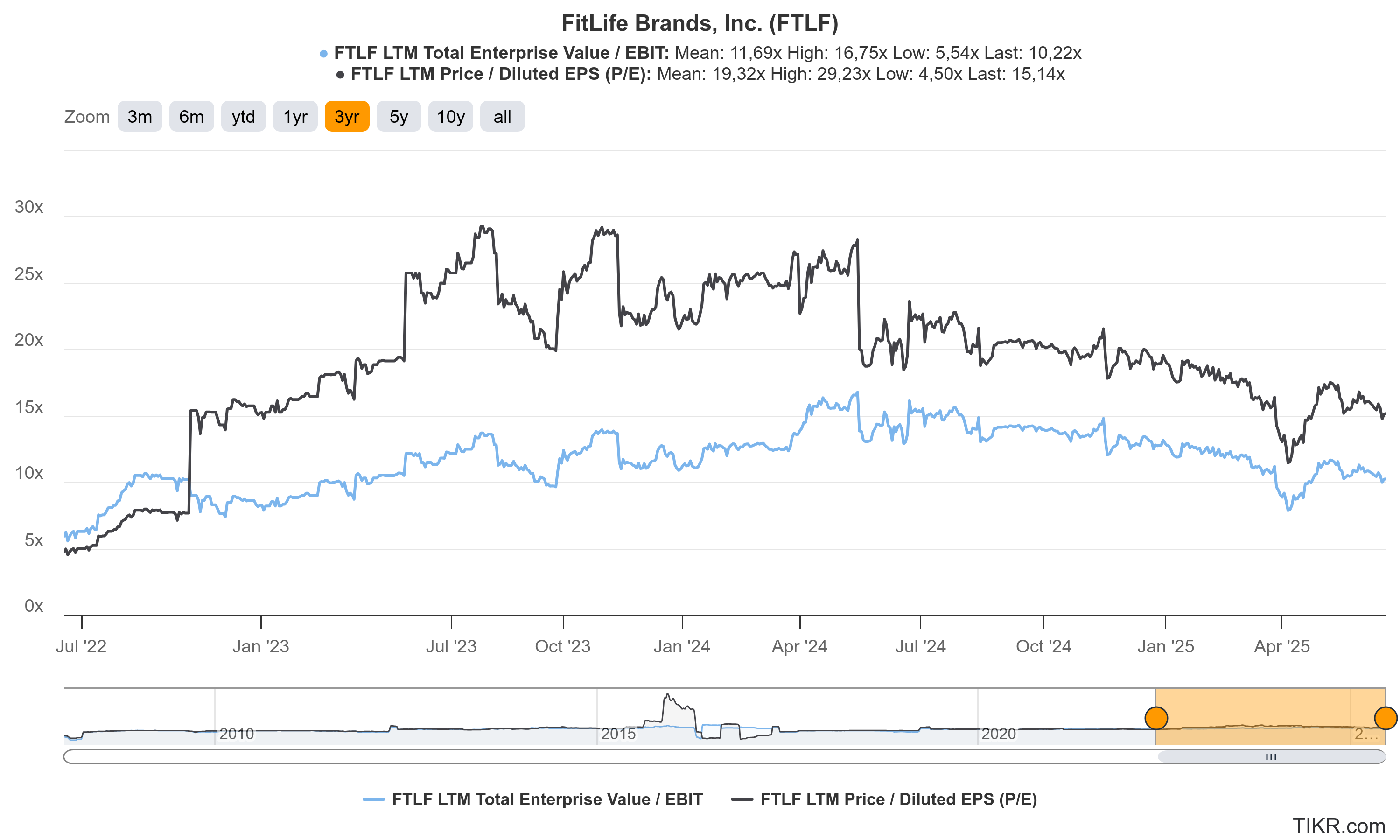

Valuation

FitLife Brands, Inc. trades on the NASDAQ under the ticker FTLF and carries the ISIN US33817P4054. As of mid‑June 2025, the company has approximately 9.39 million shares outstanding, with a public float of about 7.94 million shares and insiders holding roughly 14–15 %. With its share price hovering around $13.50–14.60, FitLife Brands is valued at a market capitalization of roughly US $130–133 million.

FitLife Brands is currently trading at valuation levels that suggest the market has reset its expectations after a period of strong optimism. Its latest price-to-earnings (P/E) ratio stands at around 15, which is meaningfully below its three-year average of over 19. That puts the stock at roughly a 6–7% earnings yield—a level that implies investors see the business as steady, but not in high-growth mode.

On an enterprise value to EBIT (EV/EBIT) basis, the company trades at just over 10×, again below its recent average of nearly 12×. That valuation reflects a more cautious stance from investors, despite FitLife’s solid profitability and capital-light model. The spread between the P/E and EV/EBIT ratios also suggests the balance sheet is clean, with little to no debt distorting the multiples.

Overall, this positions FitLife as a fairly valued small-cap with room to re-rate higher—if it can reaccelerate growth or further improve margins. Current valuation levels don’t assume aggressive expansion, which could work in investors’ favor if the company outperforms. On the other hand, if earnings momentum slows, the stock could continue to drift in line with its now more tempered multiples. For investors, it’s a wait-and-see setup: execution will matter more than hype.

Investment Case

Bullish Thesis: FitLife has demonstrated that it can grow rapidly while maintaining profitability. Revenue rose 22% in 2024, driven by both organic gains and accretive acquisitions (MRC, MusclePharm). Gross and operating margins have expanded with scale, indicating a profitable growth model. The company is essentially leveraging internet retail – two-thirds of sales are online – which should benefit from ongoing e-commerce trends. Management appears savvy in product development and cross-selling; its varied brand lineup lets it capture multiple supplement niches. Cash flow is strong and debt is low, enabling future investments. If FitLife can continue adding brands or expanding channels (e.g. international, more retailers) while keeping costs in check, earnings could accelerate and justify a higher valuation.

Bearish Thesis: On the flip side, FitLife faces concentration risks and tough competition. A large portion of its sales comes via Amazon (∼66%) and one retailer (GNC). If Amazon changes fees/policy or GNC reduces orders, revenue could plunge. The supplement market is very crowded, so price and advertising wars could erode margins. The recent acquisitions – while promising – may also overstate future growth if integration proves difficult (the elevated M&A expenses in early 2025 hint at that challenge). The company is still relatively small; it could get squeezed by larger players on marketing spend or shelf space. Finally, as a micro-cap stock, FTLF can be volatile and thinly traded, meaning good news can already be priced in, while bad news could cause big swings.

Outlook

Looking ahead, FitLife’s prospects depend on execution and market trends. The company expects to leverage its acquired brands in 2025 now that MusclePharm and MRC are fully integrated. Management has expressed optimism about growing the “legacy” business (the original brands) and bringing new products through the marketing pipeline. Key catalysts include:

New product launches: Fresh supplements or improved formulas can spur repeat purchases. Each quarter FitLife tends to roll out new variants (e.g. new protein flavors, wellness vitamins) that keep its online customers engaged.

M&A or partnerships: FitLife has explicitly pursued acquisitions to fuel growth. The ability to find, finance, and integrate further deals (in nutritional supplements or related health products) could add revenue. Conversely, failure to find attractive targets might slow growth.

Retail expansion: On the wholesale side, recovery or expansion of GNC (post-bankruptcy stabilization) would boost volumes. GNC stores are slowly reopening, so FitLife may benefit. Also, getting shelf space at additional retailers (e.g. sports chains, international outlets) would diversify channels.

Marketing and brand building: Management has been increasingly active on social media and direct marketing. Success in driving traffic to their websites or Amazon pages (through influencer campaigns, SEO, etc.) could amplify e-commerce growth.

Operating leverage: As revenue grows, fixed costs (warehouse, admin) can spread, improving margins. Investors will watch whether SG&A grows slower than sales, lifting free cash flow.

On the macro side, tailwinds like rising health awareness, aging populations, and preventative-health trends support supplement demand. However, no formal analyst consensus or official guidance is available publicly beyond these expectations. The market will likely reward FitLife if it continues beating growth targets and expanding profits.

Conclusion

FitLife Brands is a profitable, high-growth supplement company that aims to capture health-conscious consumers primarily through online channels. Its diversified brand portfolio (sports nutrition, weight-loss, general wellness) and recent acquisitions have pushed growth into the mid-20% range, with solid bottom-line improvement. The company shows strengths in marketing, a lean cost structure, and modest leverage. For long-term investors, FitLife offers a growth-at-a-reasonable-price story: it trades at a mid-teens P/E with favorable margins and significant online sales exposure.

However, investors must weigh the risks: heavy reliance on Amazon and GNC for sales, intense competition, and the challenge of scaling a small consumer company. FitLife’s suitability as a long-term investment depends on believing in its execution. If management can maintain double-digit growth, integrate acquisitions smoothly, and navigate platform risks, the stock could re-rate higher. But if industry headwinds or concentration issues materialize, returns could be volatile. In summary, FitLife Brands presents a balanced investment thesis: a company with proven growth and profitability in a large market, but with clear risks that merit caution.

Another great piece, thank you very much. For me the one that goes on my watchlist is Fitlife Brands. It has high margins whilst Boot Barn Holdings and Vital Farms are lower.