#112 New Wave Group AB - A Stock Analysis

A Diversified Brand House for Long-Term Investors

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is not invested in the mentioned stock.

*Affiliate link – Get 15% off Fiscal.ai (formerly Finchat)

New Wave Group AB: A Diversified Brand House for Long-Term Investors

General Description

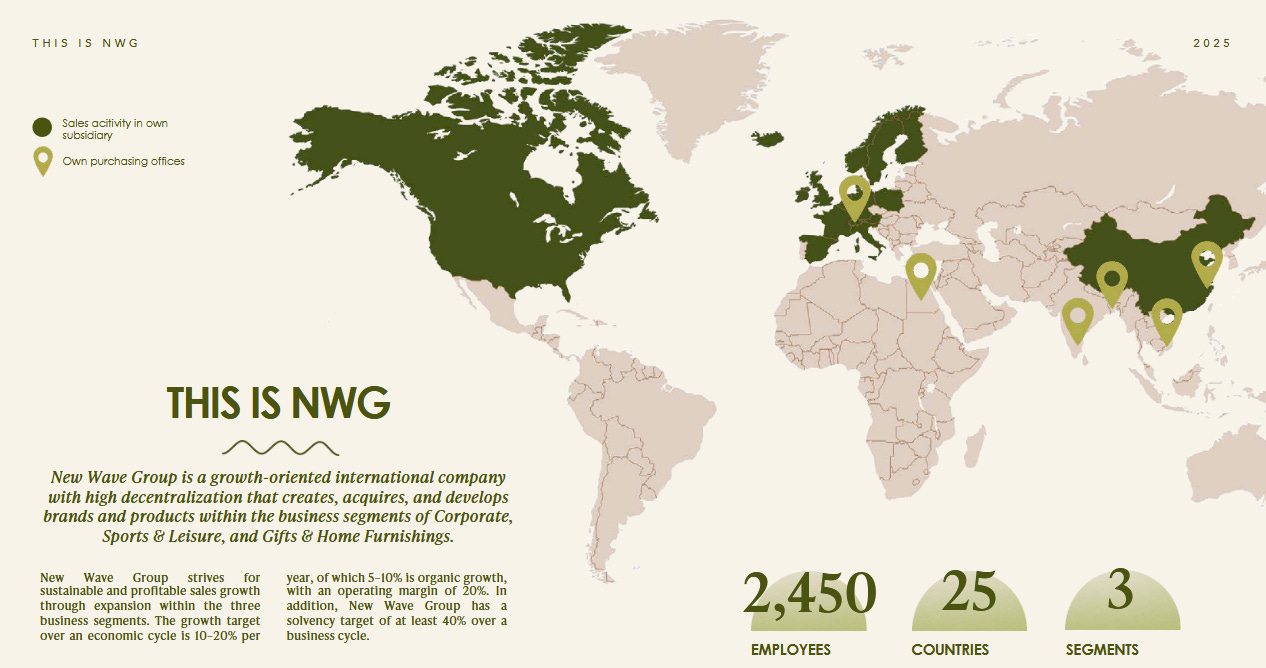

New Wave Group AB (NWG) is a Swedish consumer goods company with a diverse portfolio of brands spanning corporate promotional products, sports and leisure apparel, and gifts & home furnishings. Founded in 1990 by current CEO Torsten Jansson, NWG started by selling high-quality promowear at fair prices and has since grown into a “growth group” that designs, acquires, and develops about 40 brands across multiple niches. Well-known brands in its stable include Cutter & Buck (golf apparel), Craft (sportswear), Orrefors Kosta Boda (crystal glassware), ProJob (workwear), and Sagaform (home goods) among many others. The company also holds licensing rights for certain international names (for example, it distributes Speedo, Easton and Umbro products in some markets). This broad brand lineup allows NWG to serve both B2B customers (through corporate/promotional merchandise and workwear) and retail consumers (through sportswear, giftware and home décor lines).

Headquartered in Gothenburg, NWG has expanded its footprint beyond Sweden to become an international player – it operates across the Nordics, Central and Southern Europe, North America, and other regions. In fact, the United States is now NWG’s single largest market, accounting for about 23% of sales (26% including Canada). The company’s Class B shares are listed on the Nasdaq Stockholm (Large Cap list) and, as of 2024, NWG generated annual revenue of approximately SEK 9.5 billion (∼$870 million). Over three decades since its founding, New Wave Group has evolved into a globally diversified brand house – its strategy emphasizes continual growth through brand development and acquisitions, while maintaining a solid financial footing. The next sections will delve into NWG’s recent financial performance, business model, shareholder returns, valuation, and the investment thesis for long-term holders.

Summary of Latest Financials

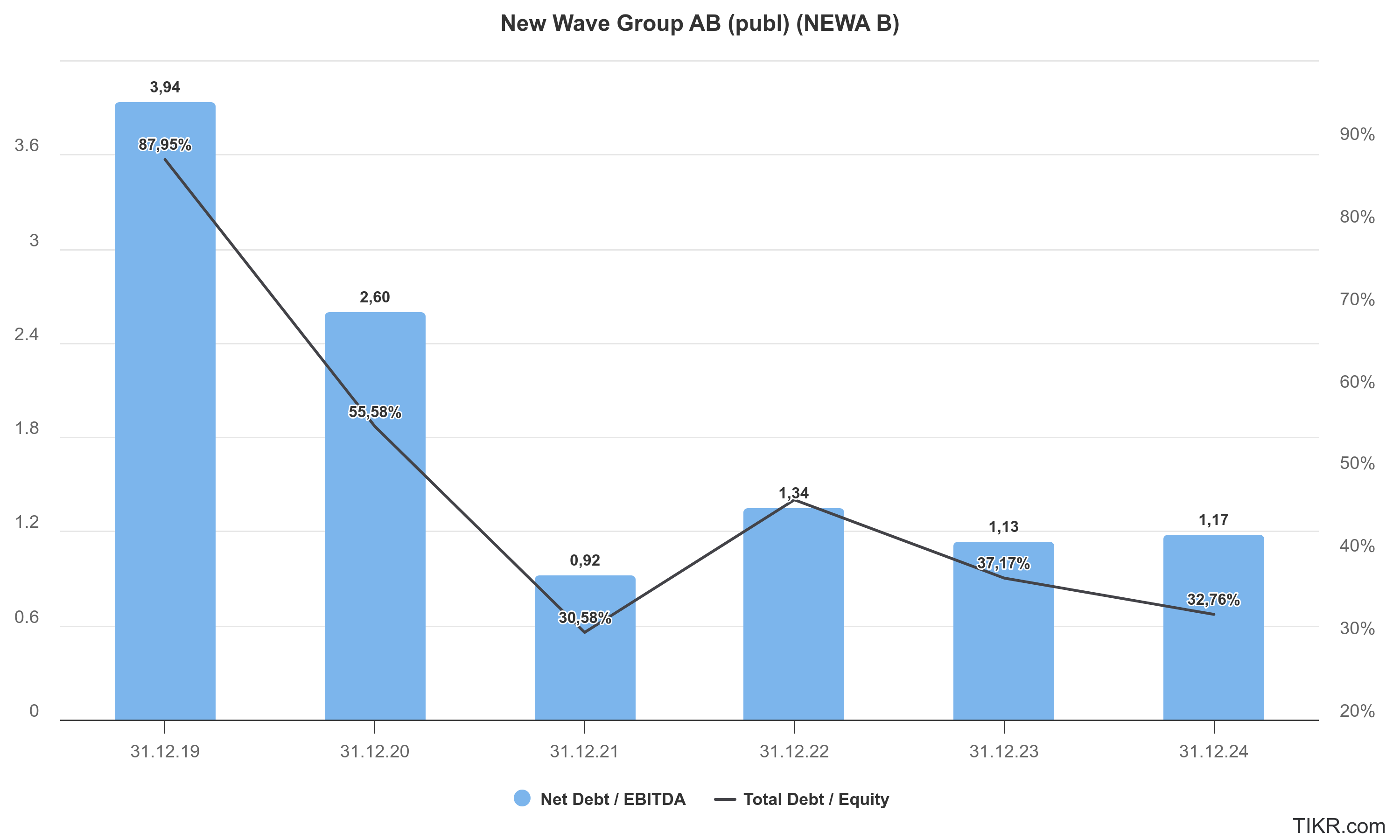

Annual 2024 Results: New Wave Group’s latest annual results (FY 2024) were mixed, reflecting a challenging economic backdrop. Net sales for 2024 were SEK 9,528.7 million, essentially flat (+0.2%) compared to 2023’s SEK 9,512.9 million. Sales held steady despite weaker demand in key markets like Sweden and Southern Europe, suggesting NWG managed to gain market share in a down market according to management. Operating profit (EBIT) came in at SEK 1,262 million for 2024, which is a 20% drop from the record SEK 1,577 million achieved in 2023. The decline in EBIT was driven by a slight reduction in gross margin (49.4% vs 50.3% prior) and higher costs as the company continued to invest in new markets and warehouse automation. Consequently, the operating margin fell to 13.2% in 2024, down from an exceptionally high 16.6% in 2023. Net income followed suit: profit after tax was SEK 880 million, down from SEK 1,119 million the year before. Earnings per share (EPS) for 2024 were SEK 6.63, compared to SEK 8.43 in 2023. On a positive note, operating cash flow hit SEK 1.28 billion, improving markedly from 2023 (SEK 964 million) despite lower earnings. This was partly due to working capital optimizations, which also strengthened the balance sheet – NWG’s equity ratio rose to 63.7% and net debt-to-equity declined to 25.2% by end of 2024, indicating a conservative capital structure.

Latest Quarter (Q1 2025): The first quarter of 2025 showed a return to growth. Q1 2025 net sales were SEK 2,184 million, up +9.5% year-on-year (with ~9% organic growth). All three business segments contributed to this top-line expansion: Corporate segment sales grew ~9%, Sports & Leisure grew ~11%, and Gifts & Home Furnishings grew ~3%. Moreover, both of NWG’s sales channels saw gains – the promotional (B2B “Promo”) channel was up 12%, while the retail channel (sales to consumers via stores/E-commerce) grew 6%. Operating profit in Q1 2025 reached SEK 212 million, a 14% increase from SEK 186 million in Q1 2024. The quarterly operating margin improved to 9.7% (from 9.3%) as NWG held gross margins steady at ~49.8% and benefited from higher volume. Net profit for Q1 2025 was SEK 144 million, up from SEK 121 million in the prior year quarter, and EPS came in at SEK 1.09 (versus SEK 0.91). Management described this as a “strong and stable start” to 2025, highlighting the broad-based growth despite a continued challenging market. The company noted that even excluding a positive calendar effect, organic growth was robust. NWG’s cash flow from operations in Q1 was SEK 219 million, slightly above last year’s level. One item to watch was foreign exchange – the strengthening of the Swedish krona late in Q1 led to a sizable negative translation adjustment in equity (–SEK 440 million) as overseas assets were marked down. Nonetheless, the balance sheet remained very strong with an equity ratio of ~63.8% after Q1.

In summary, NWG’s latest financials depict a company that weathered a soft 2024 with flat sales and compressed margins, but entered 2025 with renewed growth. The full-year 2024 results underscore NWG’s resilience (holding sales steady in a downturn) and its continued cash generation, while the Q1 2025 uptick suggests a potential inflection if economic conditions improve. Key figures from the recent reports are tabulated below for reference:

Despite the dip in 2024 profits, NWG’s management struck an optimistic tone for the future. They note that the company continued to invest in new warehouses, IT systems, and market expansion throughout the downturn, which should bolster long-term competitiveness. The CEO expressed confidence that NWG’s market share gains and high service levels will pay off when the economy turns, and indeed Q1’s rebound is an early positive indicator.

Key financials

Business Model Analysis

How NWG Makes Money: New Wave Group generates revenue by selling a wide range of branded consumer and corporate products through two main channels – Promotional (Promo) sales and Retail sales. In the Promo channel, NWG supplies products that companies use for marketing, uniforms, or gifts. This includes promotional apparel (like logo-ready shirts, jackets, caps), workwear and safety gear (through brands like Jobman and ProJob), and promotional items/giveaways (pens, drinkware, bags, etc., via brands like Toppoint and Sagaform’s corporate line). The Retail channel targets end-consumers, offering sportswear, leisurewear, footwear, and home decor items through retail stores, e-commerce, and distributors. For example, NWG’s Craft Sportswear sells performance clothing to athletes and teams; its Orrefors and Kosta Boda brands sell glassware and art glass through home décor retailers; and Cutter & Buck apparel is sold in golf shops and department stores. Some NWG brands straddle both channels – for instance, Clique provides basic apparel that is sold as promo merch and also as casual retail wear.

NWG operates with three reporting segments based on product category: Corporate, Sports & Leisure, and Gifts & Home Furnishings. The Corporate segment (largest by revenue) covers promo wear, workwear, and promotional gifts – essentially catering to corporate clients’ needs for branded merchandise and uniforms. Sports & Leisure includes sports apparel, equipment, and footwear (Craft, Cutter & Buck, Seger socks, etc.), often catering to both amateur and professional sports markets. Gifts & Home Furnishings includes home decor, glassware, awards/trophies, and gifts (Orrefors, Kosta Boda, Sagaform, etc.). Each segment has dedicated management to coordinate product development and strategy, but importantly they share certain group resources and infrastructure to realize synergies.

Diversification as a Strength: A hallmark of NWG’s business model is its diversification – by product category, brand, geography, and channel. This reduces reliance on any single market. Geographically, NWG’s sales are well spread across Europe and North America, with ongoing expansion into new countries. While Sweden is the home base, its contribution to sales has been declining (Sweden was only ~16% of group sales in Q4 2024, and saw a 6% drop that quarter). Meanwhile, other Nordic countries, Central Europe, and the U.S. have grown. As noted, North America now accounts for over a quarter of revenues, following successful expansion in the United States (now NWG’s #1 market) and Canada. This broad reach helped NWG offset weaknesses in specific regions – for example, when Sweden and Southern Europe lagged in 2024, growth in the U.S., Nordics (ex-Sweden), and Central Europe kept overall sales flat.

Another strength is NWG’s multi-brand portfolio strategy. Having dozens of brands enables the group to target various customer segments and price points. Some brands focus on value and volume (e.g. Printer Active Wear offers basic promo clothing in large volumes), while others are premium (e.g. Orrefors art glass, Auclair high-end gloves). NWG often acquires established brands and then invests to grow them further. For instance, NWG acquired U.S.-based Ahead (golf headwear and apparel) and Paris Glove (gloves) in 2011, broadening the Sports & Leisure lineup. More recently in 2023–2025, NWG has pursued strategic acquisitions to boost its distribution might. In 2020, it bought B.T.C. Activewear in the UK, and in mid-2025 NWG announced the acquisition of Austria-based Cotton Classics, a major multi-brand apparel wholesaler in Central/Eastern Europe. These moves strengthen NWG’s presence in key markets and add new B2B e-commerce capabilities (Cotton Classics, for example, brings an advanced B2B webshop platform through which ~90% of orders are placed). Such acquisitions not only contribute additional revenue (Cotton Classics had €97 million in sales 2024) but also allow NWG to plug its own brands into new distribution networks. This is a powerful model: NWG can acquire distributors in new regions and then introduce its proprietary brands alongside the existing portfolio, driving growth synergies over time.

Distribution and Integration: NWG’s distribution strategy combines direct sales, distributor partnerships, and its own retail outlets. In the promo channel, the group often sells business-to-business, meaning its customers are typically promotional product agencies or corporate clients ordering in bulk. NWG has an extensive network of resellers for its promo products (e.g. small promo product firms across Europe source blank apparel from NWG’s Clique or New Wave catalogs). For retail, NWG sells via third-party retailers (sporting goods stores, gift shops, online marketplaces) and also operates some flagship stores/outlets, especially for its giftware segment (the “Kosta” area in Sweden even features a destination retail village and hotel centered around Kosta Boda). Additionally, e-commerce is an increasingly important channel: NWG’s own brand sites (like CraftSportswear.com), online retailers, and the B2B portals all facilitate sales in the digital age. The company has been investing in warehouse automation and IT systems to support both promo and retail fulfillment, aiming for efficient handling of many SKUs and order sizes.

Strenghs and Weaknesses

Strengths: New Wave Group’s business model shows several strengths. First, its brand portfolio and product breadth position it to capture a wide range of customer spending – from corporate marketing budgets to individual consumer purchases. During economic expansions, the promo business typically benefits as companies ramp up advertising and uniforms, while the retail side captures consumer discretionary spending on sports and gifts. During slowdowns, having a strong value-oriented offering (e.g. basic apparel) and B2B revenue can provide some cushion. NWG’s economies of scale in sourcing and distribution also give it an edge: the group can leverage its centralized procurement (for textiles, for example) across brands to negotiate favorable manufacturing costs. The synergy of shared services (warehousing, logistics, finance) across dozens of brands allows smaller brands under NWG’s wing to be more profitable than they might be independently. NWG is also known for its entrepreneurial culture and long-term management – Torsten Jansson as founder-CEO (and major owner) provides continuity and deep industry knowledge, and the group tends to reinvest for growth with a long horizon. The balance sheet strength (over 60% equity ratio) is a strategic asset, enabling NWG to seize acquisition opportunities and endure economic cycles without jeopardizing stability.

Weaknesses and Risks: Despite its resilience, NWG’s model has some weaknesses. The promotional products industry is cyclical – when economic uncertainty or recessions hit, companies often cut back on marketing, branded swag, and uniform upgrades, which can hurt NWG’s Corporate segment. Indeed, NWG’s sales stalled in 2024 partly due to macro softness, and management openly acknowledges that a significant risk would be a broader economic downturn reducing demand. Similarly, consumer-facing segments (sports apparel, home décor) are discretionary and face competition from larger global brands. Another challenge is managing a large portfolio of brands across many regions – execution needs to be strong to ensure each brand stays relevant and distribution channels are optimized. NWG has to balance investments across established cash-cow brands and newer growth brands. Additionally, while acquisitions offer growth, they also pose integration risks. For instance, the Cotton Classics deal will add volume but comes with lower initial margins, expected to dilute NWG’s overall operating margin by ~1 percentage point in the short term. If NWG cannot successfully introduce its higher-margin products into these acquired channels or if integration is slower than planned, profitability could lag. There’s also currency risk: NWG reports in SEK but earns a big chunk abroad, so fluctuations in SEK (like the Q1 2025 krona spike) can impact reported equity and require hedging strategies. Lastly, NWG’s promotional product business could face competitive pressure from both local players and online platforms, so continual innovation and service are needed to maintain its market share.

Overall, NWG’s business model is characterized by diverse revenue streams and prudent expansion. Its strengths in brand management and distribution have enabled steady long-term growth, but investors should remain aware of the cyclical and execution-related challenges inherent in this model.

Keep reading with a 7-day free trial

Subscribe to Kroker Equity Research to keep reading this post and get 7 days of free access to the full post archives.