#121 Interparfums SA - A Stock Analysis

A Fragrant Long-Term Investment

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is not invested in the mentioned stock.

*Affiliate link – Get 15% off Fiscal.ai (formerly Finchat)

Interparfums SA (ITP): A Fragrant Long-Term Investment

Interparfums SA isn’t the kind of company that often grabs headlines. It doesn’t own splashy fashion houses or run billion-euro ad campaigns. But behind the scenes, this quiet French fragrance specialist has built a remarkable business – one that’s compounded shareholder value for decades by turning global fashion brands into best-selling perfumes.

With a portfolio that includes names like Montblanc, Jimmy Choo, Coach, and now Lacoste, Interparfums sits at the intersection of brand cachet and operational excellence. Its asset-light model, high margins, and disciplined management make it a standout in the mid-cap luxury space. Yet after years of strong growth, the stock has cooled off a bit in 2025, as the market digests a more tempered outlook and the fading of post-COVID tailwinds.

In this deep dive, I’ll break down what makes Interparfums tick – from its business model to recent financials – and take a close look at its current valuation. Is this a quality compounder trading at a fair price, or is the market signaling tougher times ahead? Let’s find out.

Company Overview

Interparfums SA* is a Paris-headquartered company operating in the global prestige fragrance industry since 1982. It produces and distributes a wide array of high-end perfumes and cosmetics, primarily under license agreements with well-known luxury, fashion, and lifestyle brands. In essence, Interparfums partners with brand owners to create and market perfumes that reflect each brand’s identity. The company has built an impressive portfolio of prestige fragrance licenses – including Montblanc, Jimmy Choo, Coach, Lacoste, Van Cleef & Arpels, Karl Lagerfeld, Kate Spade, Lanvin, Moncler, Boucheron, and others – distributing these products in over 120 countries. This model allows Interparfums to benefit from globally recognized brands without owning them outright.

From a corporate perspective, Interparfums SA is listed on Euronext Paris (ticker: ITP) and is a member of the SBF 120 and CAC Mid 60 indexes. It is majority-owned (about 72% of shares) by its U.S.-based parent company, Inter Parfums, Inc. (NASDAQ: IPAR), which reflects the company’s French-American heritage and aligns management’s interests with shareholders. The remaining float (~28%) is held by institutional and public investors. Since its IPO in 1995, Interparfums has rewarded long-term investors with substantial growth – the adjusted IPO price was just €0.68 per share, compared to around €32 in mid-2025. This tremendous appreciation underscores the company’s ability to grow its business and create shareholder value over the decades.

Overall, Interparfums’ identity is that of a “behind-the-scenes” fragrance specialist: it doesn’t market products under its own name, but rather leverages the brand equity of its license partners. The company’s lean structure, focus on marketing/brand management, and global distribution network have made it a notable mid-cap player in the beauty sector with approximately €3 billion in market capitalization.

Latest Financial Highlights

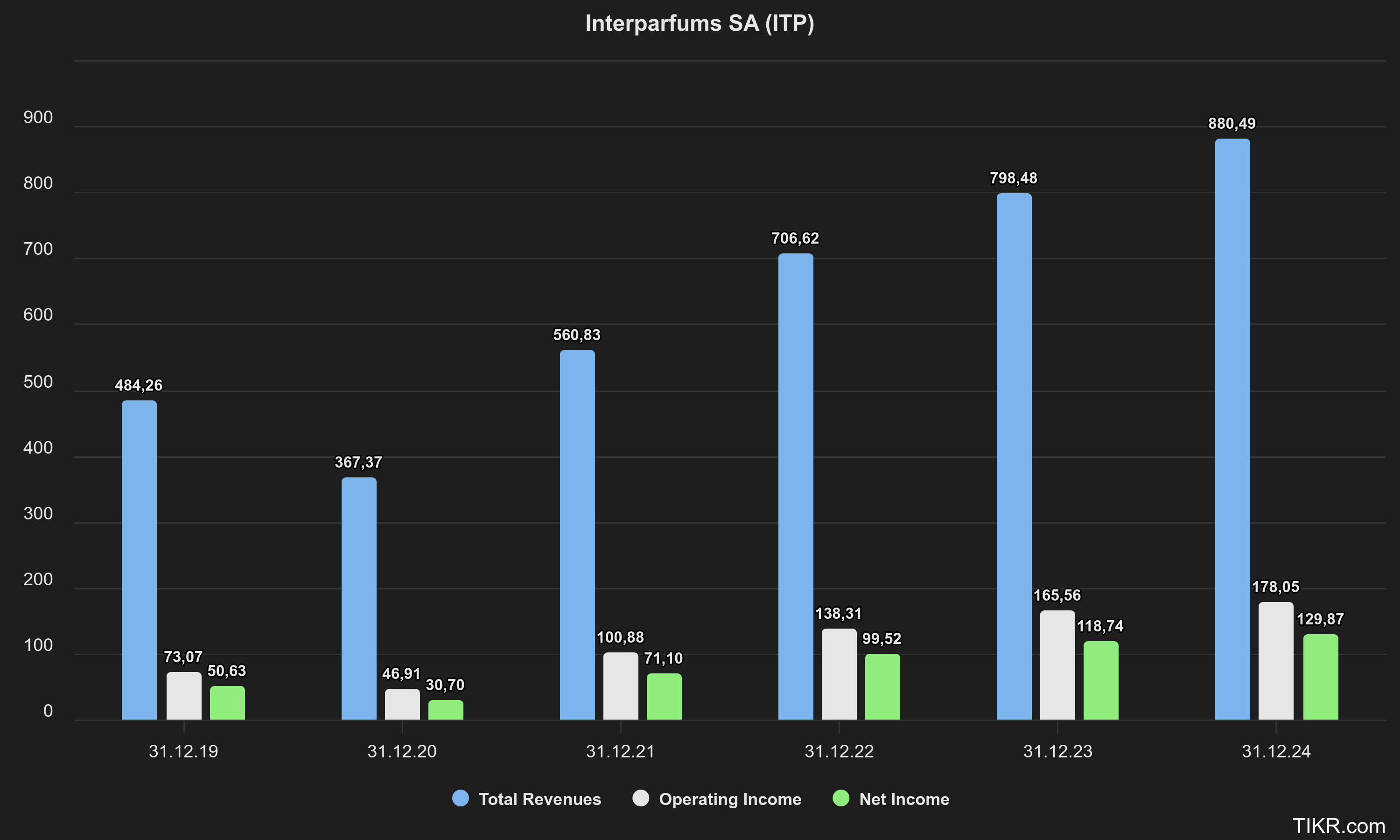

Interparfums has delivered steady growth and strong profitability, making it attractive to long-term investors. In the most recent full year results (2024), the company achieved record highs in sales and earnings. Revenue in 2024 was €880.5 million, up +10.3% from 2023, meeting management’s objectives for the year. Growth was fueled by robust demand across its top-selling brands and the successful integration of a major new license, Lacoste, which was in its first year under Interparfums’ management. Notably, each quarter of 2024 saw sales exceed €200 million – a testament to the sustained consumer appetite for the company’s fragrance portfolio.

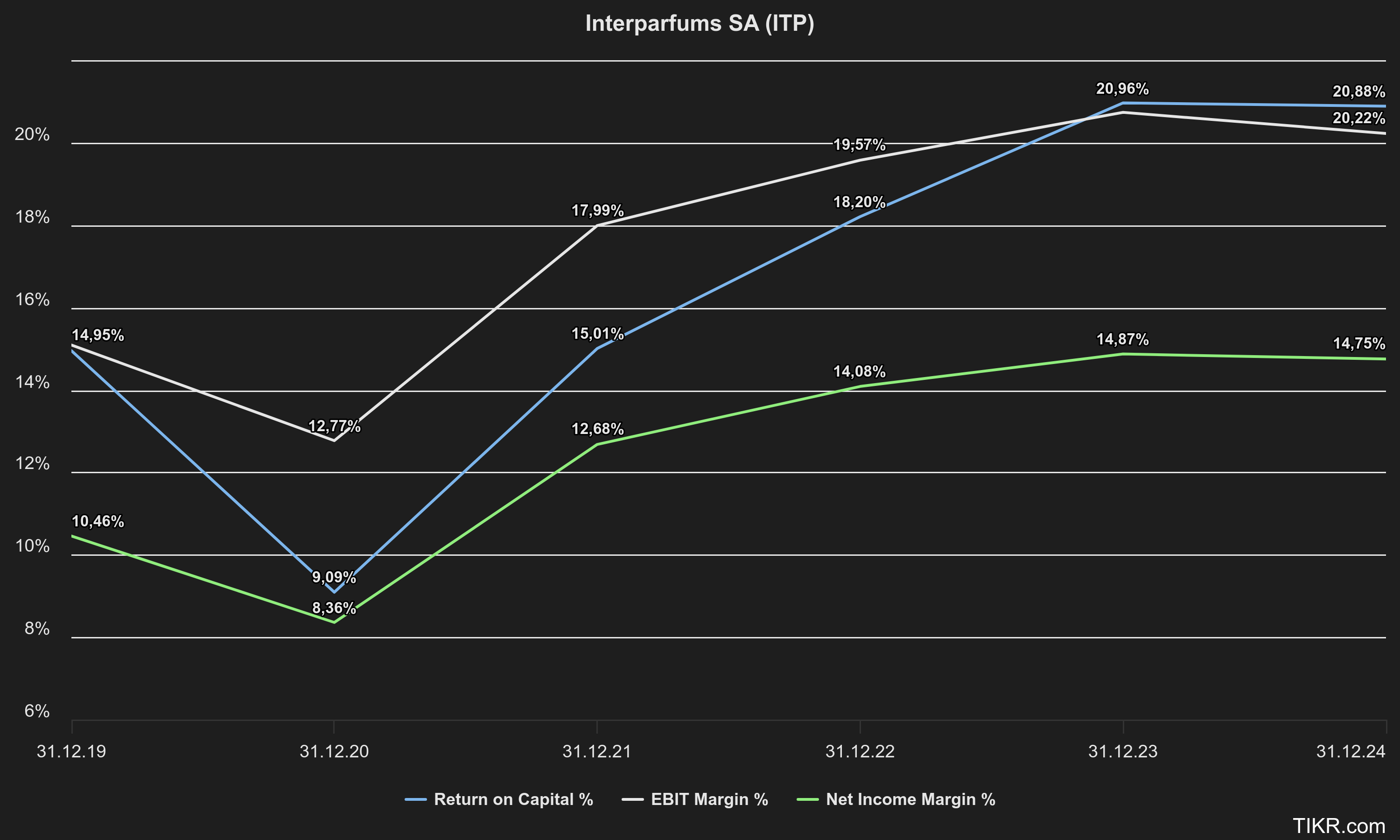

Profitability remained impressive despite inflationary pressures. Interparfums recorded an operating profit of €178.3 million in 2024, representing a current operating margin of 20.2%. This marks the second consecutive year of ~20% operating margins, indicating effective cost control and pricing power. Gross margins held steady around 65.6% of sales, as the company judiciously implemented moderate price increases in 2022–2023 to offset higher raw material and packaging costs. Net income reached €129.9 million (up +10% year-over-year), yielding a net profit margin of ~14.8% – essentially maintaining the prior year’s level. In short, 2024 saw double-digit growth in both top and bottom lines, with margins remaining solidly high.

Looking at the first half of 2025, growth has continued, albeit at a moderated pace. H1 2025 sales were €446.9 million, an increase of +5.8% year-on-year (+6.1% at constant exchange rates). The second quarter of 2025 was essentially flat (+0.7% reported, +3.3% constant currency) due to a strong prior-year comparison and some temporary headwinds. Management noted an “increasingly complex environment” in spring 2025 – including geopolitical turmoil that made consumers more cautious in certain markets. Despite that, key regions like the United States remained very strong (Q2 U.S. sales +9%), helping to offset softness elsewhere.

It’s worth noting that currency fluctuations have influenced the company’s outlook. With the euro strengthening against the U.S. dollar in 2025, the full-year 2025 revenue target was revised toward the lower end of initial estimates, ~€910 million. This is still about 3-4% growth over 2024, but slightly below earlier expectations (~€930–935m) due to the currency translation effect and a cautious view on the second half. The stock market reacted to this prudent outlook – in July 2025, Interparfums’ shares fell about 7% in one day when the company signaled it would likely hit only the low end of its sales guidance. Nonetheless, even this tempered target represents continued growth, and management’s commentary suggests confidence in ongoing expansion albeit at a more modest rate than the banner year of 2024.

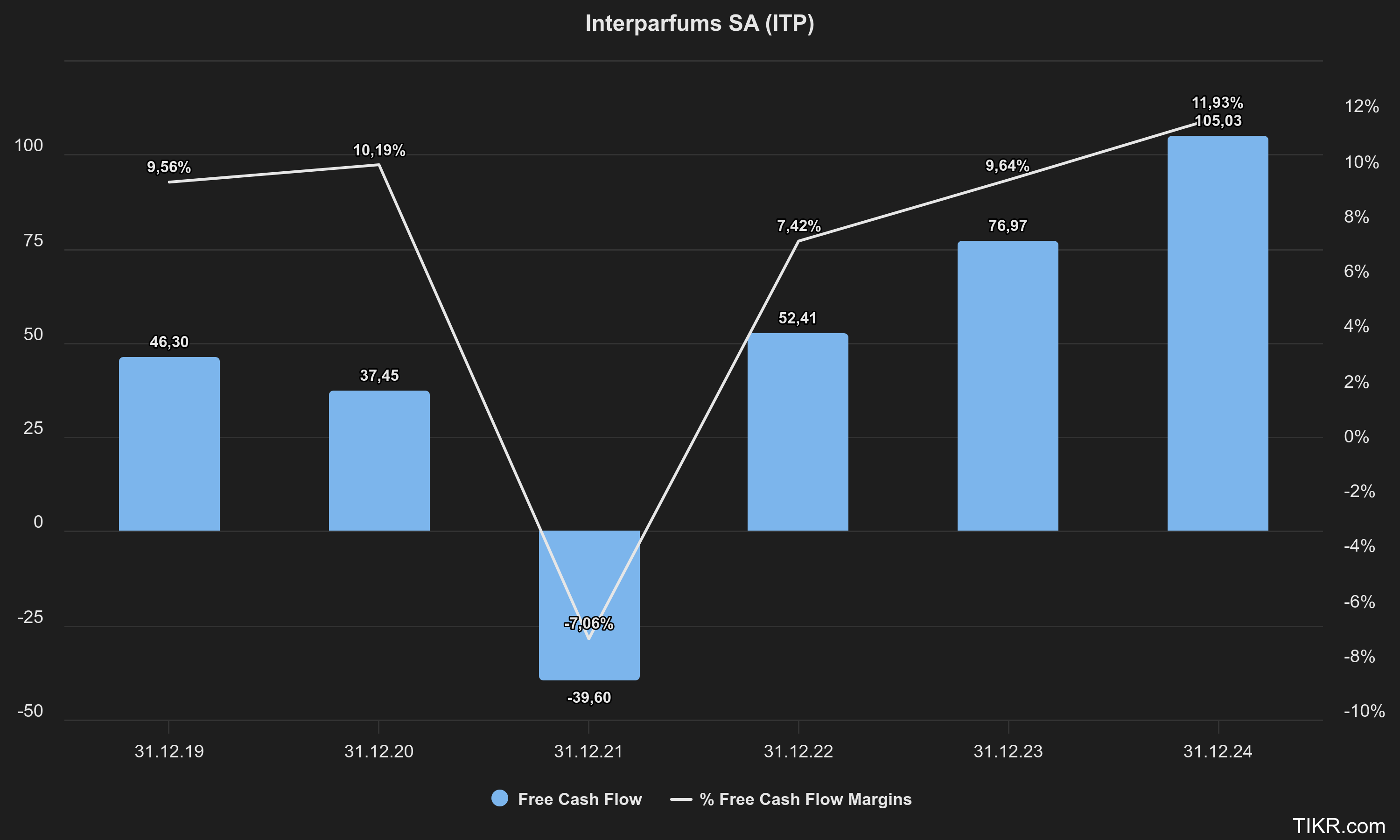

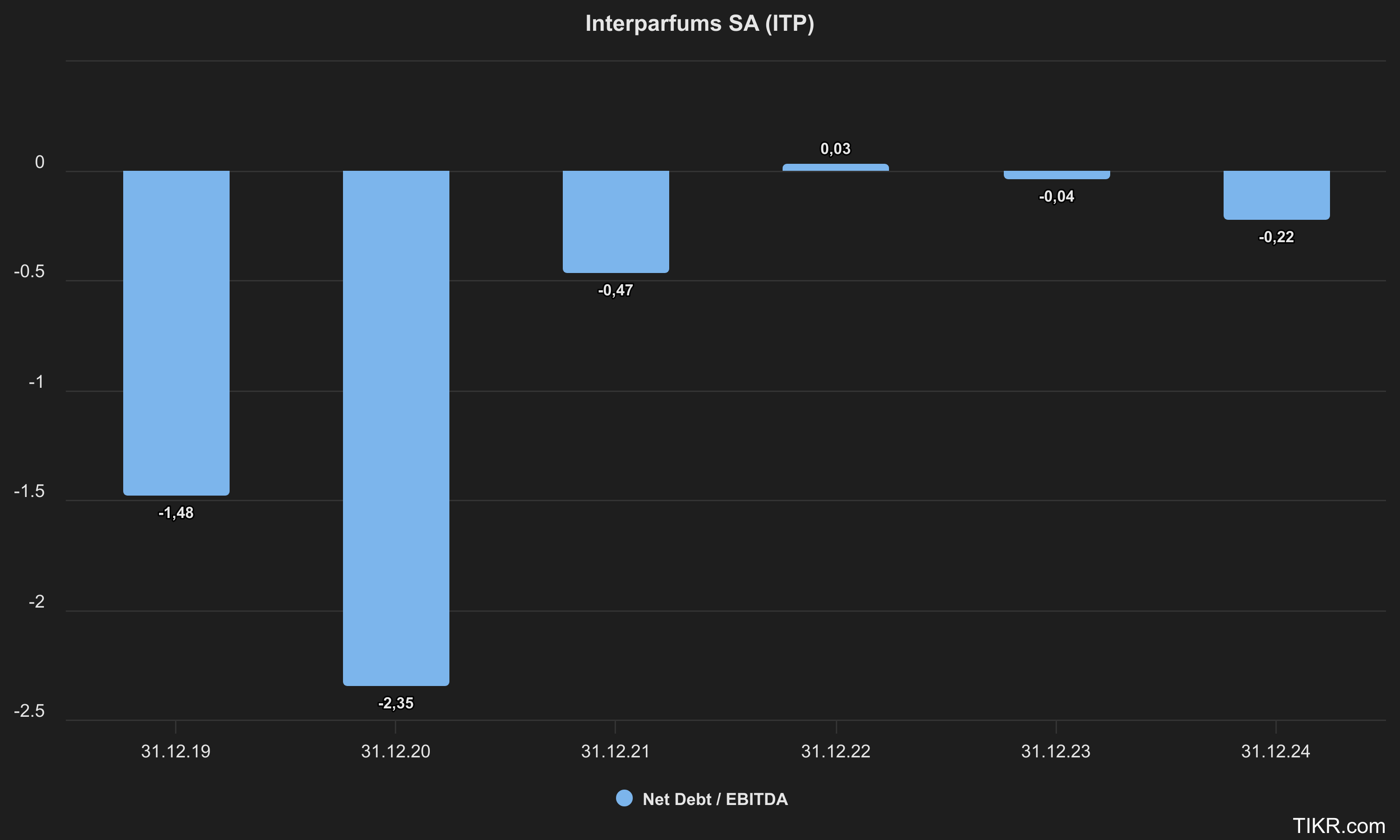

Financially, Interparfums maintains a strong balance sheet. As of December 31, 2024, the company had €190.6 million in cash and modest debt, resulting in net cash of around €57 million after deducting borrowings. Shareholders’ equity stood at nearly €700 million (roughly 66% of total assets), indicating a solid capital base with low leverage. This conservative financial posture gives Interparfums flexibility to weather economic swings and invest in growth opportunities (such as new licenses or brand acquisitions) without overstraining its resources.

In summary, recent financial performance shows healthy growth and profitability: double-digit revenue and earnings increases in 2024, followed by mid-single-digit growth in early 2025. High margins and a debt-light balance sheet highlight the quality of the business. Next, let’s examine how Interparfums generates these results – by exploring its business model and the strengths and weaknesses inherent in it.

Key financials

Business Model and Strategy

Interparfums operates a unique asset-light, license-driven business model in the fragrance sector. The company does not own manufacturing plants or large in-house production assets; instead, it outsources production to third-party manufacturers and suppliers. Interparfums acts as a creative and strategic hub – essentially a general contractor orchestrating the development, marketing, and distribution of fragrances for the brands in its portfolio. Key elements of the business model include:

License Agreements with Brand Owners: Interparfums secures long-term exclusive licenses from brand owners (fashion houses, luxury goods companies, designers, etc.) to create and sell perfumes under those brands’ names. These agreements typically last for many years (often 10+ years, with options to renew) and may involve royalty payments to the brand owner based on sales, as well as upfront fees or minimum guarantees. For example, in 2024 the company signed a new 9-year license extension with Van Cleef & Arpels (through 2033), and in 2025 it added a license for Longchamp through 2036. By partnering with established brands, Interparfums leverages their heritage and marketing cachet to sell fragrances – a symbiotic relationship: the brand owner expands into perfumes without building in-house expertise, and Interparfums gains a revenue stream tied to a desirable name.

Portfolio of Prestige Brands: Over time, Interparfums has built a diversified portfolio of brands across various styles and customer segments. This includes luxury fashion houses (e.g. Montblanc, Jimmy Choo, Coach, Van Cleef & Arpels, Boucheron), trendy designers (Karl Lagerfeld, Anna Sui), lifestyle brands (Kate Spade, Hollister under its U.S. division), and even its own owned brands (Interparfums owns the Rochas fashion and fragrance brand, acquired in 2015). Each brand license contributes to the overall sales mix – reducing reliance on any single name, although the top licenses do account for a large share of revenue. In 2024, for instance, Jimmy Choo fragrances generated €224.3m, Montblanc €203.4m, and Coach €182.0m, meaning these three brands alone made up roughly 68% of annual sales. The newer Lacoste fragrance line contributed €78.7m in its first year (about 9% of sales), and is expected to exceed €100m annually going forward. This portfolio approach allows growth to come from multiple engines – as some brands mature or slow down, others (new launches or recently added licenses) can ramp up.

Product Development & Launch Cycle: A critical competency of Interparfums is managing a pipeline of new fragrance launches for each brand. Perfumes are highly subject to fashion and trends; to sustain consumer interest, Interparfums typically launches new fragrance “families” or major product lines for each brand every few years, supplemented by more frequent flanker launches, limited editions, and seasonal offerings. The company works closely with perfumers, bottle designers, and the brand’s creative teams to ensure each new product aligns with the brand’s image and appeals to its target clientele. An average of 12–18 months of market research and development precedes any major launch, covering everything from scent composition to packaging and marketing concept. This methodical approach has yielded many hits – e.g., Montblanc’s “Legend” and “Explorer” lines, Jimmy Choo’s “I Want Choo” series, Coach’s men’s and women’s lines – which become recurring revenue generators. However, it also means the business must continually innovate and invest in marketing to refresh brand sales. In 2024, Interparfums spent €187m (over 21% of sales) on marketing and advertising to support its brands – a sizable but necessary expenditure to drive growth.

Outsourced Manufacturing and Distribution: Interparfums keeps capital expenditures low by not owning factories. Instead, components like bottles, caps, and packaging are sourced from specialized suppliers and then filled and assembled by third-party contract manufacturers. Finished products are stored and shipped from distribution centers to subsidiaries and local distributors worldwide. This flexible supply chain allows Interparfums to scale production up or down with demand and avoid the fixed costs of running production plants. It also means lower depreciation and capital risk on the balance sheet. The downside is reliance on key suppliers and potential exposure to cost inflation or supply disruptions – which the company mitigates by maintaining multiple sourcing partners and adequate inventory. In fact, in late 2024 the company deliberately held high inventory levels to ensure it could “respond quickly to customer demand” after taking over Lacoste distribution.

Global Distribution Network: Sales are made through a combination of the company’s own distribution subsidiaries in certain markets and third-party distributors in others. Interparfums has a strong presence in North America, Europe, and Asia. For the full year 2024, its sales were well diversified geographically: ~38% in North America, 18% in Western Europe, 14% in Asia, 9% in Eastern Europe, with the remainder in Latin America, Middle East, Africa, and France. This global reach helps smooth out regional volatility. For example, in the first half of 2025, North America delivered nearly +20% growth, buoyed by U.S. demand, even as Asia saw an -11% drop (due to distribution consolidation in some countries). The company adjusts its strategy by region – focusing on markets where each brand is best known. It’s also adapting to external factors like tariffs; when the U.S. imposed import tariffs on European cosmetics (10%, with threat of 30%), Interparfums took measures (like pricing and cost adjustments) to limit the impact on profitability.

In summary, Interparfums’ business model is characterized by partnering with top brands, excelling at product development and marketing, and maintaining an agile, capital-light operation. This model has proven scalable and resilient, but it is not without challenges. Let’s break down the key strengths and weaknesses for a clearer picture.

Strengths

Diversified Prestige Brand Portfolio: Interparfums manages a broad lineup of brands covering different styles and customer bases, which reduces dependence on any single brand’s fortunes. Its top brands are leaders in their segments (e.g. Montblanc in men’s luxury, Jimmy Choo in designer feminine fragrances, Coach in accessible luxury, etc.), and new additions like Lacoste broaden the portfolio further. Strong performance of multiple brands in parallel has driven consistent growth – for example, in 2024 several brands achieved record sales simultaneously. This diversity provides some cushion: if one brand faces a slow patch, others can compensate. It also gives Interparfums a pipeline of launch opportunities each year across the portfolio.

Asset-Light, High-Margin Operations: The company’s outsourcing strategy keeps fixed costs low and margins high. With no factories to maintain, Interparfums can achieve operating margins around 20%, which is high for a consumer products business. Return on sales is boosted by the focus on brand value and marketing rather than heavy manufacturing assets. The company’s gross margin of ~65%reflects its pricing power and premium positioning – consumers are willing to pay for prestige perfume brands, which supports healthy markups. Moreover, Interparfums requires relatively low capital expenditure, so it generates strong free cash flow from its earnings. This has enabled robust dividend payouts and a net cash position on the balance sheet.

Proven Marketing and Product Development Expertise: Interparfums has a 40+ year track record of creating successful fragrances that resonate with consumers. Many of its lines enjoy longevity and loyalty (e.g., the Montblanc Legend line, first launched in 2011, or Jimmy Choo’s various editions). The company’s ability to capture the essence of each brand in a scent and bottle design – and refresh it with new editions – is a core competitive advantage. For instance, in early 2025 the launch of Coach for Men Eau de Parfum and Coach Women Sunset Gold helped Coach fragrances sales surge +24% in H1. Likewise, Interparfums deftly kept Jimmy Choo’s momentum with flankers like I Want Choo Forever and a new Jimmy Choo Man line, yielding growth even for that already-mature brand. This consistent innovation engine strengthens relationships with its license partners (who see their brand’s fragrance business thriving) and with retailers who count on new releases to drive sales.

Global Distribution and Market Presence: Interparfums has a well-established worldwide distribution network and knowledge of local markets. It focuses its efforts where each brand has the strongest following – for example, Montblanc and Jimmy Choo are especially popular in Europe and North America, while some brands like Anna Sui or Hollister (from its U.S. division) have dedicated followings in Asia. This targeted approach optimizes marketing spend. The company is also quick to capitalize on new growth markets; it has seen very rapid growth in areas like South America (+13% in 2024) and a rebound in Western Europe (+25% in 2024). Its expansion into China has been positive as well (China sales +18% in 2024). In essence, Interparfums can ride the wave of global consumer trends, wherever they arise, thanks to its geographic reach.

Experienced and Aligned Management: The company is led by its co-founder Philippe Benacin (CEO of Interparfums SA) and a long-tenured executive team with deep industry experience. The U.S. parent’s CEO/Chairman, Jean Madar, co-founded the firm as well. Insiders (through Interparfums, Inc.) control the majority of shares, aligning their interests with long-term shareholder value. This stable ownership and governance structure has allowed Interparfums to execute consistent strategies without the pressure of short-term activists. Management has shown prudence (e.g., maintaining a strong financial position) and opportunism (adding promising licenses like Montblanc in 2000, Jimmy Choo in 2009, Coach in 2015, and most recently Ferragamo, Moncler, Lacoste in the 2020s) to drive growth.

Weaknesses and Risks

Dependence on License Agreements: The flip side of Interparfums’ model is that it does not own most of the brands it sells. License agreements are by nature finite – typically lasting 7 to 15 years with possible extensions. There is a risk that a major brand partner could choose not to renew a license or to take it in-house or elsewhere when the term ends. A historical example is Burberry, which was Interparfums’ largest license from the 1990s until 2012; Burberry decided to bring its fragrance business in-house, and that license termination caused a significant drop in Interparfums’ sales at the time. Today’s portfolio is more diversified, but the top three brands still form a large chunk of revenue. If, say, Montblanc or Jimmy Choo were lost, it would create a big hole. That said, Interparfums has worked to secure long-term extensions (as noted, Coach was just extended to 2031, Van Cleef to 2033, etc.) and often has excellent relationships that make non-renewal less likely. Nonetheless, this dependency is a structural risk.

Product Concentration and Launch Risk: Within each brand, success hinges on the performance of key product lines and new launches. Fragrance is a hits-driven business – a strong new perfume can boost sales dramatically, but a flop can hurt results (and waste investment). As seen in H1 2025, Montblanc’s sales fell -10% because some recent flankers underperformed and older lines started to fade. Without a major new blockbuster until late 2025, that brand’s momentum stalled. This shows that Interparfums must continually create appealing products to maintain growth. There is execution risk around each launch (from getting the scent right to marketing messaging). Consumer tastes can be fickle or shift with cultural trends, so not every new fragrance will resonate. A string of underwhelming launches could dampen the company’s growth and lead to excess inventory or markdowns. Mitigating this, Interparfums’ long experience and market studies tend to produce more hits than misses, but it’s an inherent risk in the creative consumer goods space.

Macroeconomic Sensitivity: Although perfumes are an affordable luxury, the business can be impacted by broader economic conditions and consumer confidence. During periods of economic stress or geopolitical instability, consumers may pull back on discretionary purchases like designer fragrances. For instance, in spring 2025, management observed a “wait-and-see attitude” among consumers in some markets amid geopolitical turmoil, contributing to only slight Q2 growth. Moreover, currency fluctuations can have a notable effect because Interparfums reports in euros but sells globally. A stronger euro can reduce the translated value of U.S. and international sales (as happened in 2025, prompting the company to lower its euro sales guidance to ~€910m). Conversely, a weak euro boosts results (which helped 2024’s growth somewhat). These factors – FX swings, recession risks, global crises – are outside the company’s control and can introduce volatility in results or stock performance.

Competitive Industry: The beauty and fragrance market is highly competitive, especially in the prestige segment. Interparfums competes against much larger cosmetics conglomerates like L’Oréal, Estée Lauder, LVMH, Coty, and also against niche boutique fragrance houses. Big players have greater financial clout and often own key brands or their own fragrance labels. Interparfums must continually prove itself as the best license partner for brands, delivering growth for them, so that it can win renewals and new deals. If a brand owner thinks another company could better scale their perfume business, Interparfums could lose out on new licenses. Competition is also intense at the consumer level – shelf space in perfumeries is limited, so each Interparfums product needs to justify its place with strong sales. The company’s mid-size scale means it doesn’t enjoy the same economies of scale in advertising or distribution as some giants, though it has found a profitable niche focusing purely on fragrances. Still, maintaining market share and securing new deals requires continuous effort.

Limited Upstream Control: Because manufacturing is outsourced, Interparfums can be exposed to supply chain disruptions or cost inflation. For example, sudden shortages or price spikes in alcohol (a key perfume ingredient), glass bottles, or spray pumps could impact production and margins. The company partly hedges this by having multiple suppliers and some pricing power to pass costs on, but there can be lags. Also, quality control is paramount – any issues at a third-party factory could reflect poorly on the brand. Interparfums’ lean staffing (it has relatively few employees given its sales volume) could be stretched if it had to quickly find alternatives in a disrupted supply scenario. Thus far, the company has managed these risks well (even through events like COVID-19 logistics challenges), but they remain considerations.

In weighing strengths vs weaknesses, it’s clear that Interparfums has a well-honed model that has delivered growth and profitability consistently. However, investors should keep an eye on the concentration of revenue in key licenses and the need for continued product success, as well as macro factors like currency and competition.