#14 The Cheesecake Factory - Tasty cakes and great returns?

#14 The Cheesecake Factory - Tasty cakes and great returns?

Assessing The Cheesecake Factory's Financial Flavor and Stock Valuation

Dear readers,

thank you for being here and for your interest in my work! If you like this article, if you find the stock watchlist and my deep dives valuable, and if you want to support my work, please feel free to subscribe!

Introduction

Discovering investment opportunities can be as simple as observing everyday life, rather than relying solely on conventional methods such as stock screeners or insightful articles. To illustrate this point, I would like to share a personal anecdote. During my first vacation to the U.S. in 2014, my girlfriend and I stumbled upon The Cheesecake Factory CAKE 0.00%↑ in Los Angeles, located in the vibrant Third Street Promenade. Initially, we assumed that their menu was limited to cheesecakes. However, we were pleasantly surprised to discover a full culinary array and indulged in two scrumptious slices.

This casual visit planted a seed in my investment journey. By 2017/2018, when I transitioned from passive investments in ETFs and mutual funds to active stock picking, I discovered that The Cheesecake Factory was, in fact, a publicly traded entity. With fond memories of their delightful cheesecakes and without conducting any rigorous valuation or due diligence – a stark contrast to my current approach – I made an investment in their stock. Reflecting on it now, with a wealth of experience and knowledge under my belt, I find it intriguing to consider the reasons behind that initial investment decision. It was a blend of personal experience and a rudimentary belief in the company's product, a far cry from the data-driven strategies I employ today. This story serves as a testament to how our investment choices can evolve over time, influenced by a mix of personal experiences and growing financial acumen.

About The Cheesecake Factory

The Cheesecake Factory Incorporated is a well-known company in the experiential dining industry, recognized for its culinary expertise and emphasis on hospitality. It operates 318 restaurants in the United States and Canada under different brands, such as The Cheesecake Factory (213 locations), North Italia (33 locations), Flower Child (31 locations), and other Fox Restaurant Concepts (FRC) brands (39 locations). In addition, The Cheesecake Factory operates 31 international restaurants under licensing agreements and runs two bakery production facilities.

The Cheesecake Factory Restaurants

The Cheesecake Factory operates 213 restaurants according to their latest 10-Q. They offer a high-quality dining experience at moderate prices with an extensive and innovative menu that caters to various dining preferences and occasions, including lunch, dinner, mid-afternoon, late-night, and special events. The restaurants feature an upscale casual ambiance with efficient and friendly service, and are open seven days a week. The establishment offers a comprehensive bar service, with alcoholic beverages comprising 12% of sales. In fiscal 2022, off-premise consumption options, such as delivery and online ordering for to-go sales, accounted for approximately 25% of their sales.

The menu features roughly 235 items, excluding beverages and desserts, and includes a diverse range of dishes, such as appetizers, pizzas, seafood, steaks, and vegan options. It is worth noting that their SkinnyLicious® menu offers dishes with fewer than 590 calories. Their dessert offerings, particularly their signature cheesecakes, contribute to 17% of their sales with around 45 varieties. This emphasis on unique, premium desserts significantly bolsters their brand identity and competitive edge in the restaurant industry.

The Cheesecake Factory's competitive positioning in the restaurant industry involves several key strategies:

Segment Positioning: It operates in the upscale casual dining segment, positioned above regular casual dining and closer to fine dining standards. This segment is characterized by freshly prepared, innovative food, unique layouts, and personalized service. The Cheesecake Factory is a leader in this segment, known for high average sales per square foot.

Competitive Landscape: The restaurant industry is fiercely competitive, with rivals ranging from national and regional casual dining chains to fast casual and quick-service restaurants, grocery stores, and meal kit services. The Cheesecake Factory competes based on menu quality, service, location, decor, and value.

Menu and Innovation: The restaurant provides a wide-ranging menu that emphasizes fresh, scratch-made dishes. Its strength lies in its ability to adjust to customer preferences and culinary trends. Regular menu updates and the addition of new items, such as the Classic Basque Cheesecake, ensure that the offerings remain relevant and diverse.

Pricing Strategy: Historically, menu prices increased by 2% to 3% annually. Due to inflationary pressures in fiscal 2022, they implemented higher price increases to support long-term margin objectives. Future pricing strategies will consider significant cost increases and consumer price sensitivity.

Value Proposition: The Cheesecake Factory is recognized for its value and offers a range of freshly prepared dishes at moderate prices. In fiscal 2022, the average check was approximately $29.40.

Restaurant Locations and Design: The Cheesecake Factory targets high-profile locations and flexible site layouts, accommodating urban and suburban environments. The restaurants feature contemporary interior design and decor, which contribute to a distinctive dining experience.

Bakery Integration: The bakery operations are crucial in producing high-quality cheesecakes and desserts, which enhances the company's competitive edge. This integration allows for control over the quality and creativity of their desserts, proving to be more profitable than outsourcing.

Overall, The Cheesecake Factory's competitive positioning is bolstered by its innovative and extensive menu, upscale casual dining experience, strategic location selection, strong commitment to service, and integrated bakery operations. These factors contribute to its status as a leader in the upscale casual dining segment.

The Cheesecake Factory's approach to selecting and developing new restaurant sites is multifaceted and crucial to its growth and success.

Versatile Site Selection: The company has effectively operated in various layouts, including single or multi-level, and locations such as urban/suburban areas, shopping malls, and lifestyle centers. They maintain their focus on high-quality, high-profile locations that meet strict standards.

Expansion Plan: The company aims to expand to around 300 restaurants in the United States that it owns. The selection of sites will be based on criteria such as lease terms, permits, construction feasibility, and staffing.

Critical Site Analysis: Factors like demographics, visibility, accessibility, and proximity to activity centers are crucial in evaluating potential sites. The design of each restaurant is customized according to the specific location.

Lease Negotiations and Development Time Frames: Competitive lease terms are negotiated due to high sales productivity. The development and opening process, which can range from six to eighteen months, is influenced by various factors such as licensing, permits, and supply chain challenges.

Unit Economics: High average sales per restaurant and per square foot are indicators of success. The company leases all locations and invests in leasehold improvements, with construction costs averaging around $1,000 per interior square foot.

Initial Sales Surge: New restaurants often experience a "honeymoon" period of high initial sales, which then stabilize to normal levels over a few months.

Restaurant Operations: Effective management of their complex menu and high-volume operations is crucial. This includes detailed operating procedures, staff training, and efficient food line management.

Staffing and Management: Experienced managers, comprehensive training programs, and innovative compensation structures contribute to operational success and high-quality customer service.

Preopening Costs: The preopening process is extensive and costly, averaging $1.0 to $1.5 million per location. This includes costs for staff relocation, training, wages, and other support expenses.

Overall, The Cheesecake Factory’s approach to site selection and development is characterized by careful analysis, strategic planning, and an emphasis on operational excellence and staff training. This approach supports their goal of expanding their presence while maintaining high standards of quality and customer satisfaction.

The Cheesecake Factory has implemented an international expansion strategy by means of licensing agreements with three restaurant operators. These agreements permit the development and operation of The Cheesecake Factory® brand restaurants in selected international markets. Currently, as of the latest 10-Q, 31 licensed restaurants are operational in various countries, including Bahrain, Saudi Arabia, Kuwait, Qatar, UAE, Mexico, and China (including Hong Kong, Macau, Beijing, and Shanghai).

Key aspects of their licensing approach include:

Licensees' Investment: Licensees use their capital to build and operate the restaurants.

Revenue for The Cheesecake Factory: The company earns from initial development fees, site and design fees, and ongoing royalties based on the licensees' restaurant sales. Licensees also purchase bakery products branded under The Cheesecake Factory® mark.

Expansion Rights: Licensees in Kuwait have rights to expand in countries including Egypt, Turkey, Russia, and others. The licensee in Mexico can potentially expand into South American countries like Chile, Argentina, and Brazil. The licensee in Hong Kong has expansion rights in Asian countries including Thailand, Taiwan, Japan, and South Korea.

Corporate Support and Quality Control: A dedicated global development team from The Cheesecake Factory supports licensees with training, quality control, product specifications, and brand oversight. An internal audit department reviews compliance with licensing agreements.

Future Plans: The company is working to extend and expand agreements with existing licensees and exploring opportunities in Western Europe. There's also consideration for direct operation or joint ventures in new markets.

Selective Partnership Criteria: Potential partners are evaluated based on capitalization, business infrastructure, upscale casual dining experience, and governance practices. The focus is on maintaining high-quality, consistent brand representation.

Complexities in International Expansion: Challenges include site selection, construction, staff training, supply source approval, and exportation of bakery products.

Consumer Packaged Goods: Beyond restaurant operations, The Cheesecake Factory leverages its brand in the consumer packaged goods channel. This includes partnerships with manufacturers for products like “Brown Bread,” puddings, and ice cream under The Cheesecake Factory At Home® mark, adding incremental revenue streams.

This licensing strategy enables The Cheesecake Factory to expand its global presence while upholding brand integrity and quality standards. However, it encounters the usual complexities associated with international expansion in the restaurant industry.

North Italia

North Italia is a modern take on upscale casual dining, blending contemporary style with traditional Italian cuisine. Currently, there are 33 North Italia locations, each with a modern design that includes open kitchens and spacious dining areas, creating a welcoming neighborhood atmosphere. North Italia's menu offers a diverse selection of handcrafted dishes, including appetizers, salads, pastas, pizzas, and main courses. The menu also features unique dishes that reflect local culinary preferences. In fiscal year 2022, the beverage segment, which includes wines, beers, and house-made cocktails, accounted for 25% of total sales. The brand's positioning in the market is indicated by the average expenditure per customer, which was approximately $32.00 for lunch and $41.50 for dinner.

Looking at North Italia’s growth strategy, there are several key components:

Expansion Potential: Given the popularity of Italian cuisine in the United States, there is considerable scope for expansion. North Italia aims to capitalize on this demand with plans for up to 200 domestic locations. This expansion aligns with the brand’s target of approximately 20% average annual unit growth, suggesting a robust and aggressive growth strategy.

Sales Performance: The financial metrics underscore the brand's success, with average sales per mature location reaching about $8.0 million in fiscal 2022. This translates to an impressive $1,300 per productive square foot, reflecting strong revenue generation capabilities.

Restaurant Size and Construction Costs: North Italia targets a specific range for its restaurant size, typically between 6,000 to 7,000 square feet. The investment in creating these spaces is substantial, with average construction costs amounting to approximately $650 per interior square foot. This investment reflects the brand’s commitment to maintaining a specific aesthetic and quality standard in its establishments.

Preopening Costs: The initial investment for opening a North Italia location in established markets ranges between $0.5 million to $0.7 million. These preopening costs are indicative of the comprehensive planning and resources allocated to ensure each new location is poised for success.

Fox Restaurant Concepts

Fox Restaurant Concepts (FRC) is an independent subsidiary within The Cheesecake Factory’s corporate structure. FRC is an innovator in the food, dining, and hospitality sectors, focusing on developing and nurturing new restaurant brands. This strategy has led to the launch of over a dozen diverse dining concepts.

Among these, Flower Child is a key player in the fast-casual dining segment. Flower Child prioritizes fresh, locally-sourced ingredients, aligning with growing consumer trends favoring health-conscious and environmentally sustainable dining options. FRC has identified other concepts like Culinary Dropout and Blanco as having significant potential for growth, indicating a strategic focus on diversifying its portfolio within different market segments.

FRC has set an ambitious target of achieving 15% to 20% average annual unit growth in terms of growth objectives. The expansion of Flower Child is expected to be the primary driver of this growth, indicating that this brand will be a central focus of FRC's expansion strategy in the coming years.

FRC's financial performance has been noteworthy, with FRC restaurants averaging approximately $5.8 million in sales per location in fiscal 2022. This figure provides insight into the revenue-generating capacity of FRC's restaurant portfolio. Furthermore, the construction costs for FRC locations average around $500 per interior square foot. This cost parameter is an essential factor in understanding the capital investment required for the development and expansion of new and existing restaurant concepts under the FRC umbrella.

Bakery Operations:

The Cheesecake Factory operates two key bakery production facilities located in California and North Carolina. These facilities are central to the company's operations, tasked with the production of a wide range of cheesecakes and other desserts. The integration of these bakeries into the company’s broader operational framework provides The Cheesecake Factory with direct control over the quality of their desserts. This control is not only crucial for maintaining product consistency but also presents a more cost-effective solution compared to the alternative of outsourcing. During the Q3 call the management revealed its plan to build a third bakery production in Charlestown, Indiana.

Beyond supplying desserts to their own restaurants, The Cheesecake Factory extends its market reach by selling to external foodservice operators, retail establishments, and through online distribution channels. This diversification of sales avenues is indicative of the company's adaptive business strategy and its focus on capturing a wider market segment.

On an international scale, The Cheesecake Factory's baked products are distributed under The Cheesecake Factory At Home® brand in about 20 countries. This international presence is not merely a channel for product distribution but also plays a role in enhancing the brand's global recognition. Additionally, it complements the company's efforts in expanding its restaurant footprint beyond domestic borders. Overall, the bakery operations of The Cheesecake Factory demonstrate a strategic blend of quality control, market expansion, and brand reinforcement, both domestically and internationally.

Companies Strategy

The strategic overview of The Cheesecake Factory Incorporated outlines a comprehensive plan that focuses on maximizing shareholder value through customer satisfaction, financial management, and targeted expansion. The company aims to enhance customer satisfaction by continuously innovating its menu, providing exceptional service, and executing operations impeccably.

Meticulous financial management is a pivotal aspect of this strategy. The company maintains strict control over expenses in all areas of the business, including restaurants, bakeries, and the corporate support center. Effective use of purchasing power is crucial in achieving this goal.

The company's strategy places significant emphasis on expansion, particularly through the development of new company-owned restaurants. These establishments are strategically located in prime areas with a focus on expanding The Cheesecake Factory and North Italia brands, while also developing new concepts under the Fox Restaurant Concepts (FRC) umbrella. The grammar, spelling, and punctuation are correct. No changes in content were made.

The company aims for investment returns of 20-25% cash-on-cash for The Cheesecake Factory, 35% for North Italia, and 25-30% for FRC concepts. The language used is clear, objective, and value-neutral, with a formal register and precise word choice. The text adheres to conventional structure and format, with consistent citation and footnote style. Revenue growth is driven by the opening of new restaurants and increases in comparable restaurant sales.

The Cheesecake Factory employs a multifaceted strategy to increase comparable sales, including initiatives to increase the average check and maintain customer traffic. This approach includes menu innovations, service enhancements, expanded off-premise dining options, and targeted marketing efforts.

The company carefully balances pricing and menu management to align with its margin objectives and customer traffic expectations. Regular menu updates and price adjustments are implemented, particularly in light of recent inflationary pressures.

The margin objectives are clearly defined, with the goal of not only recapturing pre-COVID-19 pandemic margins but also driving long-term margin expansion. The Cheesecake Factory Incorporated aims to optimize its restaurant portfolio for maximum efficiency by leveraging various revenue streams.

Its capital allocation strategy balances investments in new restaurants, debt management, and returning capital to shareholders through dividends and share repurchases.

The company's long-term financial objective is to achieve a 13-14% total return to shareholders. The Cheesecake Factory Incorporated's strategy combines the growth in earnings per share with the dividend yield.

The company achieves this through a blend of culinary innovation, financial rigor, and strategic growth initiatives. The diverse brand portfolio, which includes international licensing and bakery operations, is integral to the company's overarching goal of comprehensive growth and sustained shareholder value.

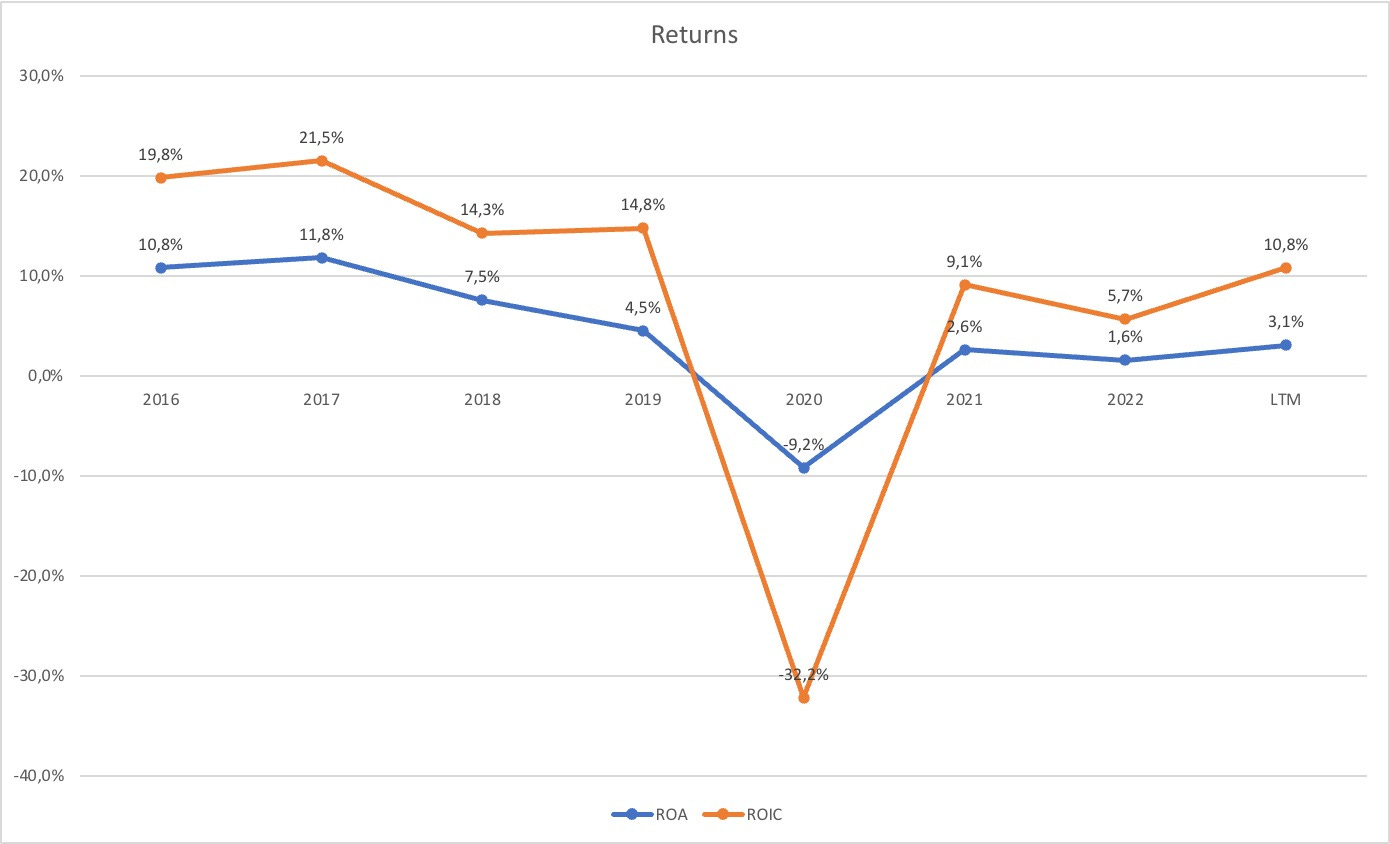

Key financial figures

The graphs and tables provided offer a clear visual representation of the key trends, allowing for a more concise analysis.

In the upcoming graphs, a notable observation is the consistent growth in revenues over time. However, this growth is not mirrored in the company's income. This discrepancy indicates that while the company has been successful in increasing its sales, it has not been equally effective in translating these sales into profits. A closer examination reveals a concerning trend of deteriorating margins and returns over recent years. This trend is a crucial point of discussion in the investment thesis section, where I argue the absence of a significant competitive advantage, or 'moat', for the company. The data visualizations serve to underscore this argument, highlighting the challenges faced by the company in maintaining profitability amidst revenue growth.Mostly the graphs and tables speak for themselves, so I will save words here.

Recent developments

The Cheesecake Factory experienced significant developments in the first nine months of 2023. Here are the key highlights:

Revenue Growth: The company's revenues increased by 6.3% to $2.5625 billion compared to $2.4104 billion in the prior year. This growth was primarily driven by an increase in comparable restaurant sales and additional revenue from new restaurant openings.

Sales Performance: The average sales per restaurant operating week for The Cheesecake Factory increased by 3.0% to $235,398. The total operating weeks at The Cheesecake Factory restaurants increased by 1.4% to 8,227.

Comparable Sales Increase: There was a 3.2% increase in comparable sales, amounting to $58.4 million, from the first nine months of fiscal 2022. This increase was mainly due to a rise in the average check of 4.5%, driven by a 10.2% increase in menu pricing, partially offset by a 5.7% negative impact from menu mix. Customer traffic decreased by 1.3%.

Off-Premise Sales: Sales through the off-premise channel comprised approximately 22% of the restaurant sales during the first nine months of 2023, compared to 25% in the same period in 2022. However, these figures remain elevated compared to the pre-pandemic level of 16%.

Cost Management: As a percentage of revenues, food and beverage costs were 23.5%, down from 24.5% in 2022, mainly due to menu price increases slightly exceeding inflation. Labor expenses decreased as a percentage of revenues from 37.1% to 35.9%, attributed to menu price increases outpacing wage rate inflation.

New Restaurant Openings: The company opened seven new restaurants, including three The Cheesecake Factory locations, one Flower Child location, and three other FRC locations.

Preopening Costs: Preopening costs increased to $15.8 million from $9.0 million, partially due to the mix of new restaurant openings and delays in the timing of new restaurant openings, resulting in additional costs.

Interest and Other Expenses: Interest and other expenses increased to $6.1 million from $3.9 million, primarily due to higher interest on the Revolver Facility.

Income Tax Rate: The effective income tax rate decreased to 6.0% from 7.4% in the first three quarters of fiscal 2023 and 2022 respectively.

These points reflect a period of growth and expansion for The Cheesecake Factory, with a focus on increasing sales and managing costs effectively. The expansion of new restaurants and the increase in average sales per operating week demonstrate the company's strategic efforts to enhance its market presence and operational efficiency.

Stock Valuation

The Cheesecake Factory is expected to experience strong growth in the coming years. Revenues are projected to increase annually at a rate of 6.4% until 2025, indicating a steady upward trend. Additionally, EBIT (Earnings Before Interest and Taxes) is expected to grow at an annual rate of 12.2%, indicating a strong recovery from recent economic challenges.

These projections serve as the foundation for my analysis of the company's financial health and future prospects. By incorporating these growth rates into my calculations of Free Cash Flow, I have estimated an intrinsic value of approximately $39 per share for The Cheesecake Factory's shares. This provides insight into the company's potential market value in the near future.

Capital Allocation

The Cheesecake Factory allocates a significant portion of its sales revenue towards the development of new restaurants, reflecting its status as a business with substantial investment in physical assets. In the past year, the company allocated approximately 3.9% of its sales revenue to capital expenditure. This investment rate is expected to increase marginally in the near future.

The Cheesecake Factory distributes its Free Cash Flow through both stock repurchases and dividend payments, actively returning value to its shareholders. At present, the company has an ongoing authorization to repurchase up to 61 million shares. The primary objectives of these repurchases are to offset the dilution of shares resulting from equity compensation grants and to augment the growth of earnings per share. The share repurchase program is open-ended, meaning it does not have a set expiration date and the company is not obligated to acquire a predetermined number of shares. The program's terms allow for modifications, suspensions, or terminations at any time.

The Cheesecake Factory currently distributes $0.27 per share each quarter as dividends, providing a yield of 3.3% to its shareholders. This reflects the company's commitment to consistent and reliable financial returns, making it an attractive investment option for those seeking a steady stream of income.

Investment Case

Formulating an investment case for The Cheesecake Factory presents challenges, particularly when considering the company's competitive positioning. It is perceived that the company lacks a distinctive competitive advantage that sets it apart from competitors. However, the stock appears to be slightly undervalued, which could present an opportunity for investors.

When analyzing The Cheesecake Factory's potential, it is noteworthy to consider the company's recent emphasis on its rewards program, as highlighted in the Q3 2023 earnings call. The program is still in its early stages of success but is poised for further development with a focus on member engagement and growth. This initiative proposes a strategic effort to increase membership enrollment and enhance engagement with current members, which could lead to more frequent visits and increased spending through personalized promotions and targeted offers.

The company's plan to expand and refine the rewards program, possibly incorporating new features and leveraging data analytics to better serve members' preferences, is in line with industry trends. Rewards programs in the restaurant sector typically aim to enhance customer loyalty, improve guest experiences, and collect valuable customer data. These programs often offer perks such as special discounts and redeemable points. The Cheesecake Factory's program likely includes similar features designed to foster repeat business and build a loyal customer base.

Beyond the rewards program, The Cheesecake Factory's investment case includes several elements:

Brand Recognition and Offerings: The company is known for its extensive menu and signature desserts, appealing to a diverse customer base.

Growth Potential: There's substantial growth potential domestically and internationally, particularly with plans to expand brands like North Italia and FRC.

Stable Financial Performance: Historical data shows stable financial performance with opportunities for revenue expansion through targeted unit growth and sales increases.

Operational Control and Bakery Integration: The integration of bakery operations enhances quality control and cost management, contributing to revenue through both internal and external sales.

Consumer Packaged Goods Potential: Ventures into consumer packaged goods open additional revenue streams and enhance brand visibility.

However, potential investors must weigh these positives against various risks:

Economic Sensitivity: The restaurant industry's vulnerability to economic shifts can impact consumer spending and revenues.

Competitive Landscape: Operating in a highly competitive market poses challenges to maintaining market share and profitability.

Rising Operational Costs: Inflation and supply chain issues could lead to increased expenses not fully offset by menu pricing strategies.

Health and Dietary Trends: Evolving consumer health trends may not align with The Cheesecake Factory's menu, affecting customer traffic.

Labor Market Challenges: Hiring and retaining skilled staff in a tight labor market can impact operations and costs.

Pandemic and Health-Related Risks: Public health crises like the COVID-19 pandemic can cause operational disruptions and reduced customer traffic.

Short interest: According to TIKR.com, the stock has a short interest of approximately 12.4%.

In conclusion, while The Cheesecake Factory presents an investment opportunity with its brand strength, growth potential, and operational efficiency, these factors must be carefully balanced against inherent industry risks and the perceived lack of a distinct competitive moat.

Conclusion

In conclusion, our analysis of The Cheesecake Factory provides a comprehensive evaluation of its investment potential. The company has a strong product offering with a well-known and popular brand, particularly recognized for its diverse menu and signature cheesecakes. These positive brand perception and product quality are undeniable assets in the competitive restaurant industry.

However, the absence of a clear competitive advantage raises concerns about its long-term strategic position against rivals. Additionally, the observed decline in margins over the years is a critical factor that potential investors should consider. Although the stock currently seems undervalued, offering a potentially attractive entry point, there are inherent risks involved. The future performance of the stock and its ability to reach the calculated value is uncertain, particularly given the broader economic landscape and market dynamics.

However, there is potential for margin improvement as the economic situation stabilizes and improves. This could enhance the company's financial health and increase its investment appeal. However, investors should approach The Cheesecake Factory with a balanced and objective view, considering its strong brand and product appeal in light of the challenges posed by the lack of a clear competitive advantage, fluctuating margins, and the uncertain economic outlook. As with any investment, it is crucial to conduct thorough due diligence and carefully consider both the opportunities and risks before making an informed decision.

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is invested in CAKE.