#15 Stock Watchlist - 2/2024

#15 Stock Watchlist - 2/2024

Adding a couple of new companies to the watchlist

Dear readers,

thank you for being here and for your interest in my work! If you like this article, if you find this stock watchlist and my deep dives valuable, and if you want to support my work, please feel free to subscribe!

Please note the disclaimer at the end of the article. The fair values I have calculated are only estimates and unfortunately do not mean that they will be achieved. In particular, they should not be interpreted as price targets.

Intoduction

Welcome to the second update of the Stock Watchlist 2024. I won't keep you too long with an introduction this time, as I just want to focus on the stock watchlist and the newly added companies. This time we are adding six companies to the list.

New Companies/Stocks:

Danone

Dominos Pizza

McDonalds

Honeywell

Rollins

The Cheesecake Factory

About the New Stocks on the Watchlist

Danone

Danone S.A. is a major player in the global food and beverage industry with operations across Europe, North America, Latin America, Asia Pacific, Africa, the Middle East, and the Commonwealth of Independent States. The company was founded in 1899 and is based in Paris, France. It is structured into three main segments.

Essential Dairy & Plant-Based: Danone produces a variety of dairy products, including yogurts and milk products, as well as plant-based alternatives. These products are marketed under well-known brands such as Actimel, Activia, Alpro, and Oikos, among others. In addition, Danone offers coffee creamers, beverages, ice creams, frozen desserts, and cheese products, with offerings under international brands like International Delight, SToK, Silk, and So Delicious. Danone also distributes products under a licensed partnership with Dunkin’ Donuts.

Specialized Nutrition: This segment focuses on nutrition products tailored for specific demographics. It includes products for pregnant and breastfeeding mothers, infants, and young children, available under brands like Aptamil, Nutrilon, Gallia, and Cow & Gate. Additionally, it provides medical nutrition products like tube feeding solutions under the Nutrison brand and oral nutritional supplements under Fortimel and NutriDrink. The segment also offers hypoallergenic products for children with allergies under brands like Aptamil ProSyneo.

Waters: Danone produces a range of water and beverages, including naturally extracted water and fruit juices enriched with vitamins. Notable brands in this segment include Evian, Volvic, Aqua, and Bonafont.

Danone distributes its products through a variety of channels, including retail chains, traditional markets, convenience stores, hospitals, clinics, pharmacies, and increasingly through e-commerce platforms.

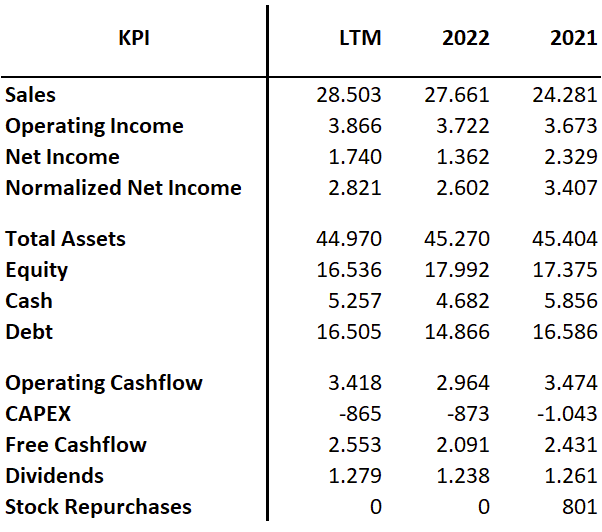

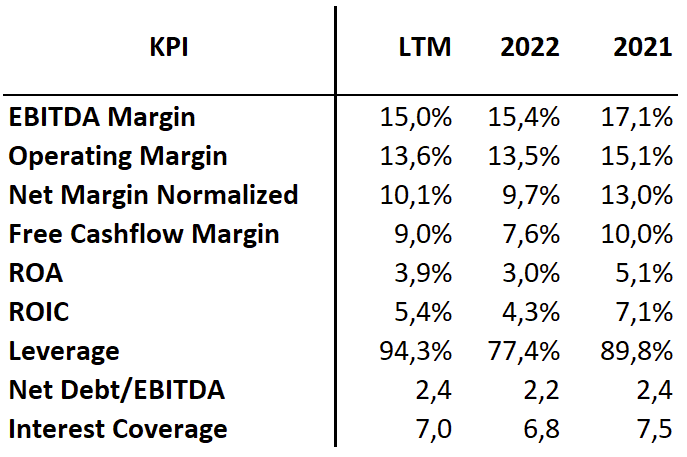

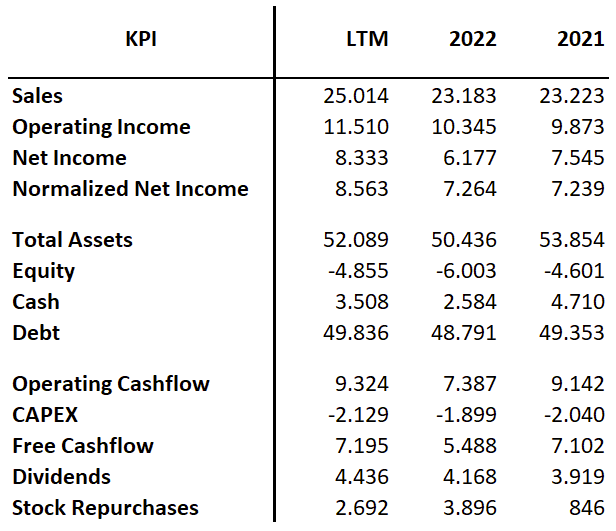

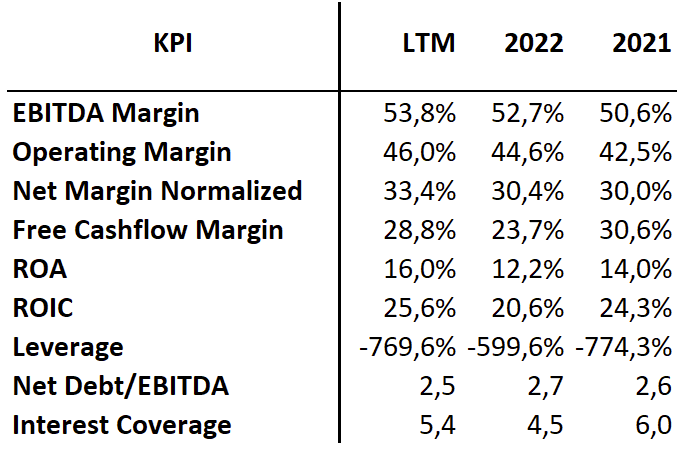

Key Figures

Valuation and Investment Thesis:

Estimated Fair Value:

Base case: € 55

Bull case: € 59

Bear case: € 52

Current price: € 61

Danone's current stock valuation suggests a premium, potentially positioning it as overvalued in the short term. However, the company's fundamental qualities designate it as a high-quality candidate for long-term watchlist inclusion. Danone's portfolio, marked by its robust brand presence and resilience, has demonstrated considerable pricing power, a testament to its market influence and strategic pricing capabilities.

The company's response to various challenges, such as the complex developments in Russia, demonstrates its adaptability and strategic foresight. The placing of its Essential Dairy and Plant-Based (EDP) business under temporary external administration in Russia has required a dynamic approach to its regional operations and financial strategies. Despite these challenges, Danone has been able to maintain operational continuity and prioritize the safety and well-being of its employees, demonstrating its crisis management expertise.

Additionally, the company's ongoing business transformation, especially in the European market, reflects a proactive approach to market shifts and consumer trends. This transformation is a strategic overhaul to reposition its EDP segment, targeting key areas such as health, indulgence, kids, and everyday nutrition. The focus on portfolio optimization and innovation in Europe is a clear move towards sustaining long-term growth and enhancing market competitiveness.

Additionally, Danone's diversified product portfolio is highlighted by its broad-based growth across its EDP, Specialized Nutrition, and Waters categories, each showing over 5% growth in recent quarters. This diversification not only mitigates risks inherent in specific market segments but also provides multiple avenues for revenue generation.

Furthermore, Danone's financial performance in 2023 further supports the investment thesis. Despite global economic uncertainties and inflationary pressures, the company has successfully navigated a challenging environment. Its recurring operating margin, earnings per share (EPS), and free cash flow have improved, reflecting financial robustness and operational efficiency.

In conclusion, although current market valuations may suggest a premium on Danone's stock, its robust brand portfolio, strategic business transformations, and resilient financial performance position it as a potentially valuable long-term investment. Investors should monitor Danone for favorable entry points, considering its ability to navigate market challenges and capitalize on growth opportunities in the global food and beverage industry.

Dominos Pizza

Domino's Pizza, Inc., DPZ 0.00%↑ established in 1960 and headquartered in Ann Arbor, Michigan, is a renowned pizza company with operations in the United States and internationally. The company functions through three primary segments:

U.S. Stores: This segment encompasses the operations of company-owned pizza stores in the United States.

International Franchise: This segment deals with the company's international operations, primarily through franchised Domino's Pizza outlets.

Supply Chain: This segment manages the supply and logistical aspects to support both U.S. and international stores.

The company operates both company-owned and franchised stores, catering to a diverse customer base. Domino's offers a range of pizzas, as well as oven-baked sandwiches, pasta, boneless chicken and chicken wings, assorted breads and dips, desserts, and soft drinks. Domino's has gained a reputation for its efficient service and diverse menu options, contributing to its prominent position in the global pizza market.

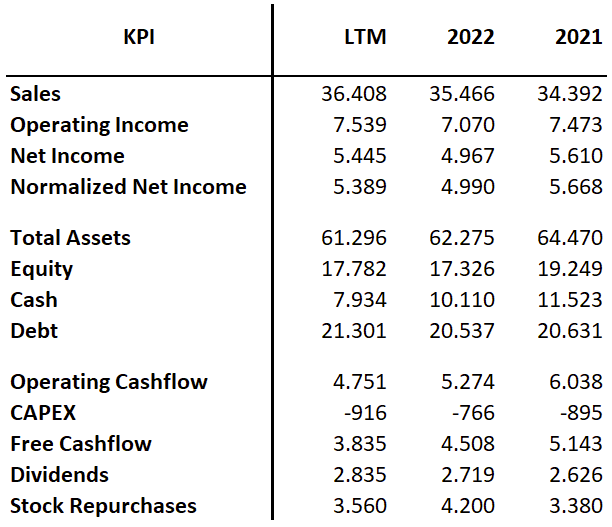

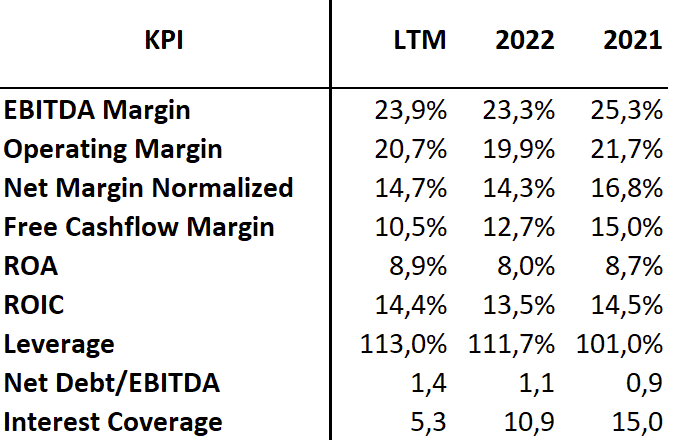

Key Figures

Valuation and my Investment Thesis:

Estimated Fair Value:

Base case: $ 300

Bull case: $ 320

Bear case: $ 280

Current price: $409

Domino's Pizza, Inc. is a significant player in the global pizza delivery industry, known for its substantial market share and prominent brand recognition. The company's successful franchise model and innovative marketing strategies have contributed to sales growth and customer loyalty.

In response to the geopolitical environment, Domino's decision to strategically withdraw from the Russian market is viewed as a prudent one, aligning with global business standards and ethical practices.

Domino's growth trajectory is centered around the 'Hungry for More' strategy, which includes innovative product development, operational efficiency through technological solutions like Dom OS, delivering outstanding value, and capitalizing on its robust franchisee network. The financial goals of the company are to achieve a growth rate of over 7% in global retail sales (excluding FX). This will be achieved through a combination of same-store sales increment, with a target of 3%+ in the U.S., and substantial store expansion, with a goal of opening 175+ new stores annually in the U.S. and 925+ internationally. The company aims to increase its operating income by $400 million by 2028, supported by a strong projected annual cash flow exceeding $500 million, which will enable significant shareholder returns.

Digital innovation is a crucial factor in driving growth for Domino's. The company has upgraded its digital ordering systems and integrated AI to provide personalized customer experiences, meeting the increasing demand for online food services. These technological advancements are expected to improve operational efficiency, enhance customer service, and increase retention.

Additionally, the company's expansion into high-growth markets like China and India presents significant opportunities. Domino's competitive position in these regions is strengthened by its ability to adapt its offerings to local preferences and the advantages of its master franchisee model.

However, caution is advised for investors due to the high market valuation, which is considered high based on a Discounted Cash Flow (DCF) model. This evaluation may not fully consider the range of market risks, such as fluctuating commodity costs, labor market challenges, and intense competition within the QSR landscape, possibly due to optimistic long-term growth projections and discount rates.

In summary, Domino's Pizza, Inc. is a strong investment prospect due to its market dominance, strategic growth initiatives, and commitment to technological innovation. While the DCF analysis suggests overvaluation, the brand's solid track record and long-term objectives make it an attractive option for investors with a longer investment horizon. It is essential to remain vigilant of market trends and the company's strategic implementation.

McDonalds

McDonald's Corporation MCD 0.00%↑ , founded in 1940 and headquartered in Chicago, Illinois, is a globally recognized fast-food chain. The company operates and franchises McDonald's restaurants both in the United States and internationally. These restaurants offer a wide variety of menu items, which include:

Classic fast-food fare such as hamburgers, cheeseburgers, chicken sandwiches, and nuggets.

A range of sides like fries, salads, and shakes.

Frozen desserts, including sundaes, soft serve cones, and other sweet treats.

An assortment of bakery items, soft drinks, coffee, and other beverages.

A breakfast menu featuring items such as muffins, sausage, biscuit and bagel sandwiches, oatmeal, hash browns, breakfast burritos, and hotcakes.

McDonald's is known for its diverse menu that appeals to a wide range of customers, featuring both classic fast-food items and newer, healthier options. The company's franchising model and global reach have made it one of the most recognizable and accessible fast-food chains worldwide.

Key Figures

Valuation and Investment Thesis:

Estimated Fair Value:

Base case: $ 226

Bull case: $ 239

Bear case: $ 212

Current price: $ 293

Despite being overvalued based on DCF analysis, McDonald's Corporation has strong fundamentals and adaptive strategies that make it an appealing long-term investment. The company's focus on value and pricing strategy, especially during challenging economic times, demonstrates its resilience and ability to maintain market leadership. This strategic positioning is essential in light of global inflationary pressures and changes in consumer spending, particularly among low-income segments. McDonald's has been able to maintain or increase its market share across different consumer demographics, demonstrating its strong brand appeal and pricing power.

McDonald's is experiencing significant increases in app engagement and loyalty memberships due to their commitment to digital engagement and innovative marketing campaigns, such as MONOPOLY and the FIFA Women's World Cup promotions. This digital pivot not only enhances customer experience but also opens new avenues for revenue growth, making McDonald's well-poised to capitalize on evolving consumer trends.

McDonald's has demonstrated its global operational strength by adapting to market-specific challenges in diverse markets such as France, Germany, and Canada. This reinforces its position as a global leader in the fast-food industry.

However, caution is advised due to the overvaluation signaled by the DCF analysis. The market price may not accurately reflect potential risks or the impact of external economic factors, such as legislative changes that affect operational costs. For example, wage increases resulting from legislative changes in California could put pressure on margins. However, McDonald's plans to mitigate these effects through pricing adjustments and operational efficiencies.

Although McDonald's has strong fundamentals and strategic adaptability, the current stock valuation may not be an optimal entry point for investment. Investors may want to wait for a more favorable valuation or use a dollar-cost averaging approach to mitigate risks associated with the current overvaluation.

In conclusion, McDonald's Corporation, with its robust business model, digital transformation, and strong global presence, remains a solid long-term investment. However, investors should approach with caution due to the overvalued stock price indicated by the DCF estimation. It is important to monitor market dynamics and valuation adjustments closely.

Honeywell

Honeywell International Inc. HON 0.00%↑, founded in 1885 and based in Charlotte, North Carolina, is a diversified technology and manufacturing company with global operations. The company operates through four main segments:

Aerospace: This segment provides a wide range of aerospace products and services, including auxiliary power units, propulsion engines, integrated avionics, environmental and electric power systems, engine controls, flight safety equipment, communication and navigation hardware, and more. It also offers radar and surveillance systems, aircraft lighting, advanced systems and instruments, satellite and space components, aircraft wheels and brakes, spare parts, and maintenance services. Additionally, it provides thermal systems and wireless connectivity and management services.

Honeywell Building Technologies: This segment specializes in software applications for building control and optimization. It offers sensors, switches, control systems, and instruments for energy management, as well as products and services for access control, video surveillance, and fire protection. It also provides installation, maintenance, and upgrade services for these systems.

Performance Materials and Technologies: This segment offers a range of products and services including automation control, instrumentation, software solutions, catalysts and adsorbents, and equipment and consulting services. It supplies materials used in various applications like bullet-resistant armor, nylon, computer chips, and pharmaceutical packaging, and offers products based on hydrofluoro-olefin technology.

Safety and Productivity Solutions: This segment provides personal protection equipment, apparel, gear, and footwear; gas detection technology; cloud-based notification and emergency messaging; mobile devices and software; as well as solutions for supply chain and warehouse automation. It also offers custom-engineered sensors, switches, and controls, along with data and asset management productivity software solutions.

Overall, Honeywell's diverse portfolio reflects its strong presence in various sectors, including aerospace, building technologies, performance materials, and safety and productivity solutions. This showcases its role as a multifaceted technology and manufacturing leader.

Key Figures

Valuation and Investment Thesis:

Estimated Fair Value:

Base case: $ 177

Bull case: $ 185

Bear case: $ 168

Current price: $ 200

Honeywell International Inc. presents an investment case that blends recent performance, strategic initiatives from the Analyst/Investor Day, and valuation concerns based on DCF analysis.

The company's pledge to achieve 4% to 7% organic growth. This growth is expected to come from innovative products and solutions, particularly in sustainability and software, with a focus on high-growth regions. The company's investment in innovative technologies and its focus on research and development capabilities demonstrate a forward-thinking approach to growth and market relevance.

Honeywell aims to expand its margin by 40 to 60 basis points, aligning its operational strategy with financial efficiency. This objective is supported by the Honeywell Operating System, which enhances productivity and business processes. Furthermore, Honeywell's target of generating cash in the mid-teens highlights its emphasis on strong financial management and efficient capital allocation.

The company's strategic approach to mergers and acquisitions revolves around focused acquisitions that complement its growth trajectory. Targeting acquisitions with characteristics such as above-average industry growth and high gross margins indicates a strategic intent to enhance the company's portfolio and shareholder value. The company's Accelerator Operating System emphasizes effective integration, suggesting a methodical approach to growth through acquisitions.

Additionally, the company's commitment to ESG principles, demonstrated by significant investments in sustainable technologies, positions it well in a market that increasingly values sustainability. The company's initiatives in energy efficiency, renewable energy, and carbon capture align with global sustainability goals and open new market opportunities.

The optimization of operations through the Honeywell Operating System aims to improve productivity and customer experience, which is crucial for long-term success across its diverse business segments.

Honeywell's aerospace segment has shown substantial growth, with a significant backlog indicating sustained future revenue potential. The resilience demonstrated in a challenging macroeconomic environment adds to the company's appeal, showing potential for risk mitigation in economic downturns.

Despite the strategic and operational strengths, the DCF analysis suggests that Honeywell's stock might be overvalued. It is important to note, however, that this evaluation is based on objective analysis and not subjective opinions. The market may have already factored in the company's growth prospects, which should be taken into consideration. This aspect calls for caution among investors, suggesting that a more attractive entry point could emerge if the market adjusts its valuation.

The company's strategic focus on automation, the future of aviation, energy transition, and digitalization aligns with current and future market trends. However, investors should consider macroeconomic factors, global supply chain challenges, and geopolitical risks that could impact Honeywell's performance.

Honeywell's strategic direction, which focuses on innovation, sustainability, and operational excellence, combined with its performance in key segments, provides a solid foundation for long-term investment. However, potential investors should exercise caution due to current valuation concerns based on DCF analysis. The optimal approach is to monitor the company's execution of its strategic initiatives and market dynamics, seeking opportunities where the market valuation aligns more closely with the intrinsic value. This provides a more favorable investment entry point.

Rollins

Rollins, Inc., ROL 0.00%↑ established in 1948 and headquartered in Atlanta, Georgia, specializes in providing pest and wildlife control services. The company operates both in the United States and internationally, and its services are extended through its subsidiaries. The main offerings of Rollins, Inc. include:

Residential Pest Control: The company provides pest control services for residential properties, protecting against common pests like rodents, insects, and wildlife.

Commercial Pest Control: Rollins, Inc. also caters to commercial customers, offering workplace pest control solutions across various industries such as healthcare, foodservice, and logistics.

Termite Protection and Ancillary Services: In addition to general pest control, the company offers termite protection services and a range of ancillary services related to pest management.

Rollins, Inc. provides pest control solutions directly to clients and through franchisee networks, catering to a diverse customer base. The company's extensive experience and expertise in the industry make it a prominent provider of pest and wildlife control services.

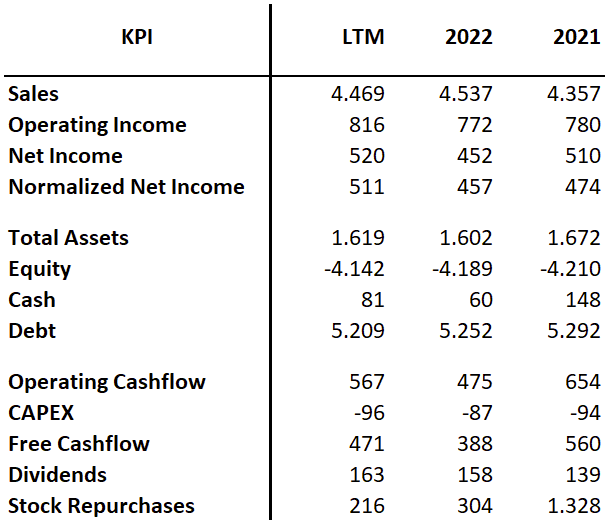

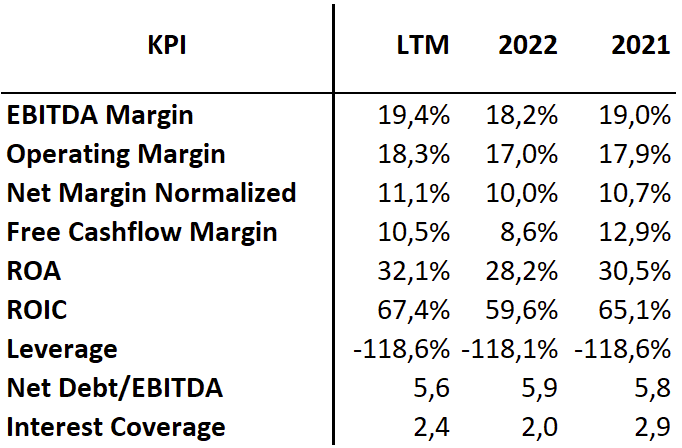

Key Figures

Valuation and Investment Thesis:

Estimated Fair Value:

Base case: $ 29

Bull case: $ 31

Bear case: $ 28

Current price: $ 44

Rollins, Inc. is a pest control services leader with a remarkable track record of consistent revenue growth and operational strength. In the third quarter of 2023, the company reported a notable 15% increase in revenue, driven by its diversified portfolio across residential, commercial pest control, and termite services. This diverse service offering highlights Rollins' ability to cater to a broad customer base, a key strength in the industry. Additionally, Rollins' organic growth exceeded 8% in Q3 2023, demonstrating the company's resilience and adaptability in various market conditions.

Strategic acquisitions are a crucial part of Rollins' expansion strategy. The recent acquisition of Fox Pest Control, along with 18 other tuck-in deals, not only enhances its market reach but also creates opportunities for operational synergies and efficiency gains. The company's approach to mergers and acquisitions is disciplined, ensuring targeted growth that aligns with its strategic objectives and reinforcing its market position.

Rollins is also well-positioned to leverage prevailing industry trends. The shift from do-it-yourself (DIY) to professional pest control services, coupled with the growing emphasis on hygiene and sanitation in both residential and commercial sectors, presents significant growth opportunities. The company's market standing is further solidified by its efforts to expand its digital footprint and diversify customer acquisition channels.

Rollins' strategy also emphasizes operational efficiency, which is supported by the recent restructuring initiative aimed at streamlining operations and reducing overheads. This is expected to yield improved profitability and margins in the long term. Rollins' commitment to continuous improvement, coupled with strategic investments in technology and human resources, underscores its focus on sustainable growth.

From a shareholder value perspective, Rollins exhibits financial stability and a commitment to delivering returns. The decision to increase dividends and engage in share repurchases reflects confidence in its financial health. Although Rollins has strong free cash flow generation and prudent capital allocation strategies, the DCF model indicates overvaluation. It is important to consider this concern despite the company's security against market fluctuations.

Additionally, the market's high expectations for Rollins' future performance introduce a risk element, particularly if the company's growth trajectory does not align with these projections. Investors may want to approach with caution, considering the potential for a market correction in light of the company's strong fundamentals. They could seek a more attractive entry point or view the stock as a long-term hold, anticipating that Rollins' operational strengths will eventually bring its stock valuation in line with its intrinsic value.

In conclusion, Rollins, Inc. is a strong company with a solid market presence, a consistent growth trajectory, and strategic expansion plans. The company's operational efficiency, strategic acquisitions, and commitment to shareholder value are key positives. Investors should consider both the short-term market risks and the long-term potential inherent in Rollins' business model, while being mindful of the current overvaluation.

The Cheesecake Factory

I recently published an in-depth analysis of CAKE 0.00%↑ .

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is invested in DPZ und CAKE .