#17 Netflix - An astonishing development

#17 Netflix - An astonishing development

Is Netflix the Streaming Wars winner?

Dear readers,

thank you for being here and for your interest in my work! If you like this article, if you find this stock watchlist and my deep dives valuable, and if you want to support my work, please feel free to subscribe!

Please read the disclaimer at the end of this article. This is not investment advice!

Recently, Netflix NFLX 0.00%↑ reported its Q4 earnings, which can be found here. In this short post, I want to write a few words about some key aspects that I noticed that I think are very important for investors to understand. I don't want to repeat the Netflix earnings here because you can find them on Netflix's IR page and there have been several other posts and articles about the actual earnings.

How Netflix became a Cash Flow Machine

Scaling up

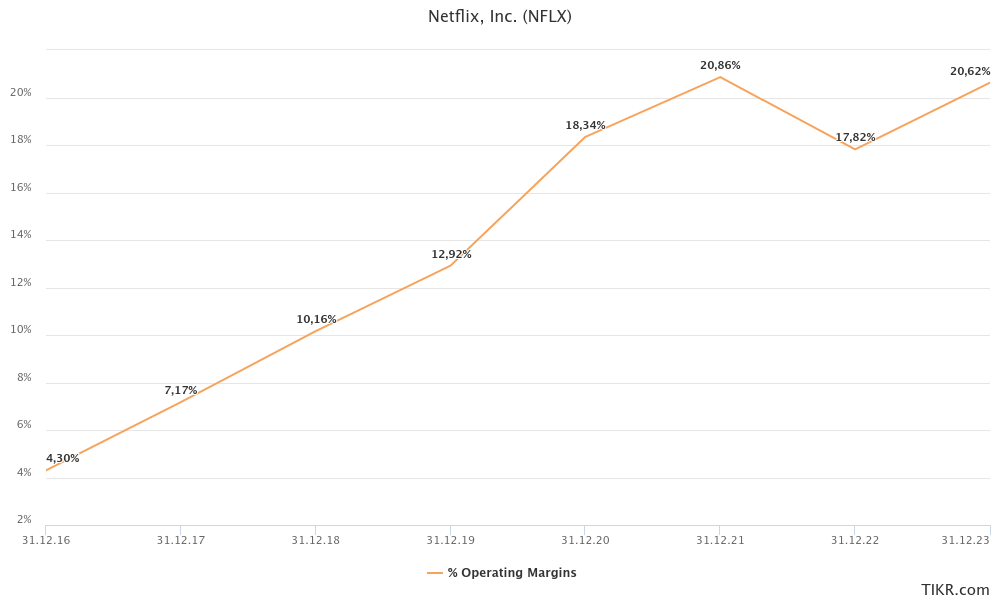

Netflix's performance in recent years seems to be a model example of how to scale a business, taking advantage of the scalability of its platform. Since 2016, Netflix has been steadily improving its operating margin in an impressive manner. Netflix's operating margin increased from 4.3% in 2016 to over 20.6% in 2023.

During this period, Netflix increased its revenues by 282% from $8.8 billion to $33.7 billion (CAGR of 21%), while its cost of sales increased by only 215%, resulting in an increase in gross profit of 444% to about $14 billion (CAGR of 27%). But that is not enough. At the same time, R&D and SGA expenses only increase by 243% and 210%, respectively, resulting in an incredible 1,731% increase in operating income to nearly $7 billion in 2023.

This positive trajectory is an important aspect of Netflix's significant cash flow improvement. Because of its subscription-based business model, its cash flow profile is stable, reliable, and also predictable. The second important point to explain the impressive cash flow improvement is content.

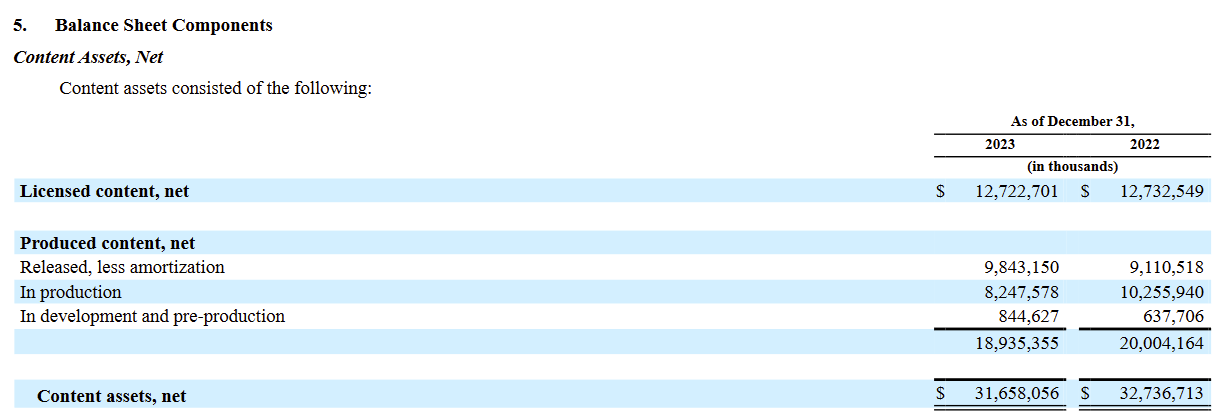

Content Accounting

Netflix has published a detailed presentation on its content accounting, explaining its impact on the balance sheet, income statement and cash flow statement.

What I would like to add here is my opinion on the presentation of content cash flows in the cash flow statement. On the one hand, it is helpful to have all content-related cash flows "close" to each other in the cash flow from operating activities, but in my understanding, the content assets are the expenditures on them, which is clearly something that should be presented in the cash flow from investing activities, comparable to a manufacturing company building a factory. It would also never show the capital expenditure for it as an operating cash flow. But that is not the point I want to make in this chapter.

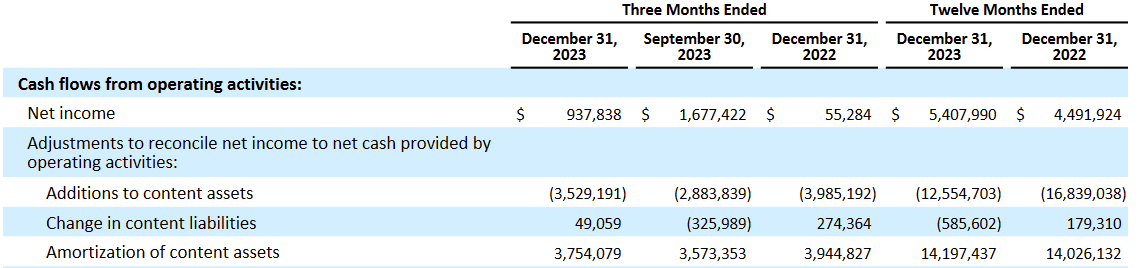

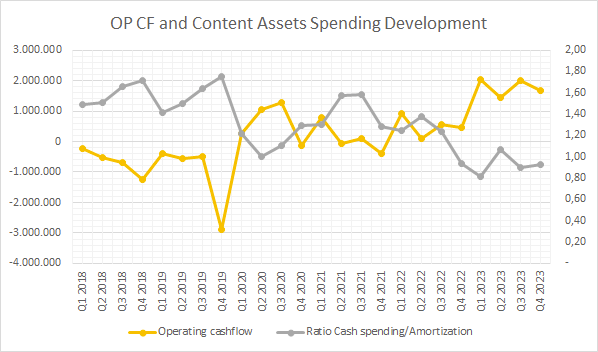

Netflix's spending pattern on content, especially on in-house productions, is upfront, the content asset is capitalized and amortized over its useful life. A useful metric to measure the timing difference between cash out and expense is the ratio of cash spending to amortization expense. A ratio greater than 1 indicates that more cash is being spent than expensed, and a ratio less than 1 logically indicates the opposite. A ratio below 1 can also be seen as a sort of break-even point, as it means that cash expenditures are equal to or less than non-cash expenses, which is positive for Netflix from a cash flow perspective.

When Netflix was investing heavily in new content a few years ago, the ratio was well above 1. However, since Q3 2022, there has been a significant decline and the ratio has been consistently below 1.

In Netflix's Q4 2023 shareholder letter, the company explains that it expects FCF of $6 billion in 2024 and cash spending on content of $17 billion.

“For the full year 2024, assuming no material swings in F/X, we currently expect FCF of approximately $6B. We continue to expect 2024 cash spend on content of up to $17B.”

Content amortization is expected to increase at a high single-digit rate.

It’s why continuing to improve our entertainment offering is so important, and as many of our competitors cut back on their content spend, we continue to invest in our slate. In FY24, we expect a high single digit percentage year over year increase in content amortization.

What exactly does that mean for 2024? Assuming an 8% increase in amortization (I would think that's a high single digit), it will increase to up to $15.3 billion. Compared to a content spend of $17 billion, this would mean that the ratio would go back above 1 (1.11). I could imagine that Netflix management will try to manage and maintain a ratio of around 1 in the long term future to match cash outflows and expenses to have a healthy balance in the cash flow statement.

Back to growth

When the pandemic started in March 2020, Netflix experienced significant membership growth, simply due to the fact that most of the world has to spend most of its free time at home in front of the TV. After that, growth slowed significantly and should return to normal, but when Netflix lost members in two consecutive quarters in 2022, it looked like peak growth was reached and it will be very hard to get back from here.

But thanks to great content and some smooth strategic initiatives, such as monetizing account sharing and advertising business, Netflix got back on track and is now crushing all expectations by adding more than 13 million new members. What comes next is hard to predict. Netflix itself expects to add 1.8 million net new members. But what investors should keep in mind is that Netflix is finding ways to grow its membership base and, because of its great content, is maintaining a really low churn rate of about 2%, much lower than other streaming companies.

Giving back

It is well known that giving back makes you happier than taking. So Netflix started giving back to shareholders through share buybacks. In total, Netflix bought back 14,513,790 shares for about $6 billion in 2023.

In Q4’23, we repurchased 5.5M shares for $2.5B and we have $8.4B remaining under our current buyback authorization.

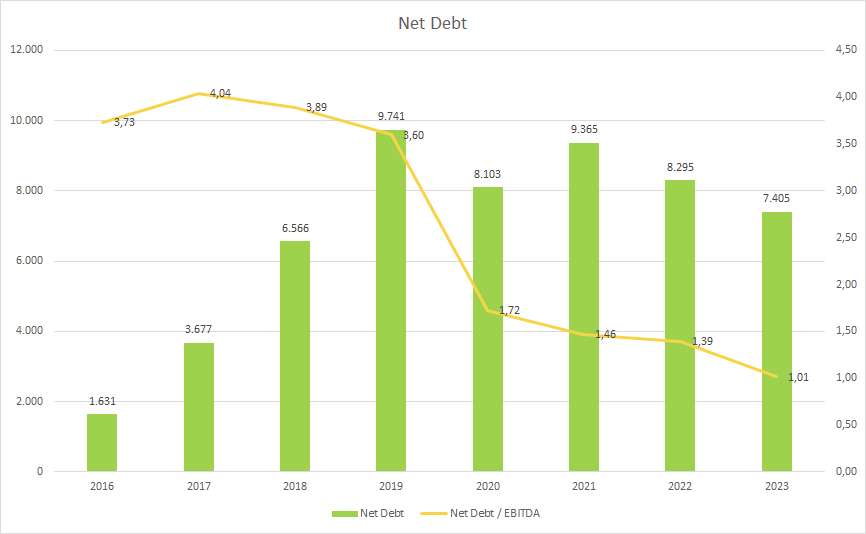

Where is the debt?

The issue of debt was a significant concern for Netflix when its earnings and cash flow were inadequate to manage its obligations. However, the narrative around Netflix's financial health has dramatically shifted since 2020. It's particularly noteworthy how Netflix has successfully reduced its net debt over time and significantly improved its leverage ratio. Specifically, the company managed to decrease its Net debt/EBITDA ratio impressively from 4.04 in 2017 to 1.01. This transformation underscores a strategic financial turnaround, illustrating how Netflix has effectively grown into its current, more sustainable debt levels.

King of Entertainment and Content

Netflix excels at producing consistently high-quality content, including movies, documentaries, and series. What sets Netflix apart is its commitment to sourcing content not only from Hollywood but globally, including notable contributions from my homecountry Germany. This global content strategy distinguishes Netflix from its competitors and has been pivotal to its worldwide success. Highlighting achievements across various genres and formats—ranging from original TV series and blockbuster movies to non-English programming and sought-after licensed titles—Netflix's approach effectively caters to a broad spectrum of viewer preferences, reinforcing its extensive international appeal.

In 2023, according to Nielsen ratings, Netflix reaffirmed its dominance in the entertainment sector in the US, securing the top spot for original TV series for 48 out of 52 weeks, original films for 41 out of 52 weeks—a notable improvement from the previous year—and acquired series for 44 out of 52 weeks.

On the day of its earnings call, Netflix made a significant announcement: a $5 billion investment in live sports, beginning with streaming WWE events. This substantial foray into sports entertainment represents a strategic move to captivate new audiences and expand its subscriber base, leveraging the immense popularity of live sports.

Netflix's venture into gaming is still in its infancy but has shown promising signs of growth, with engagement tripling over the past year. The launch of the Grand Theft Auto trilogy by Rockstar Games stood out as the platform's most successful game launch to date in terms of downloads and user engagement, indicating the potential of Netflix's gaming initiative to further diversify and enrich its entertainment ecosystem.

Some thoughts on valuation

Netflix is focused on executing well and driving continuous improvement across its content slate, user experience, and fandom, while also venturing into new areas such as advertising and gaming. The company sees significant growth potential in these areas, with the overall entertainment market presenting a $600+ billion revenue opportunity. Netflix currently captures only about 5% of this market and less than 10% of TV viewing share in any country, indicating substantial room for growth.

Predicting the future trajectory of Netflix, including membership growth, the success of new content initiatives, and the financial impact of its ventures into sports, gaming, and advertising, presents a considerable challenge. The variability and uncertainty inherent in these areas render traditional Discounted Cash Flow (DCF) analyses highly speculative, leading to a broad range of potential outcomes. Consequently, this complexity suggests that relying on valuation multipliers might offer a more practical approach to estimating Netflix's fair value, providing a clearer sense of its market valuation amidst the uncertainties.

Thats what we know about Netflix Outlook for 2024:

Entering 2024 with strong momentum, expecting healthy double-digit revenue growth on a foreign exchange (F/X) neutral basis.

Growth driven by continued membership growth and improvements in F/X neutral Average Revenue per Membership (ARM) through price adjustments.

Plans to further invest in and develop the advertising business, expecting strong growth in 2024, though it's not yet a primary revenue driver.

Aiming to make advertising a more substantial revenue stream for sustained growth in 2025 and beyond.

Operating margin forecast for the full year 2024 increased from 22%-23% to 24%, reflecting a weaker US dollar and better-than-expected performance in Q4 2023.

For 2024, assuming stable F/X rates, Netflix expects Free Cash Flow (FCF) of approximately $6 billion.

Let's conduct two straightforward valuation calculations:

First, assuming a revenue growth of approximately 13%-14%, we anticipate revenues to be in the range of $38.1 billion to $38.4 billion. Adopting a cautious approach, let's calculate with a 23% operating margin for 2024, which would result in an operating income (EBIT) of around $8.8 billion. With Netflix's Enterprise Value (EV) currently around $260 billion, we arrive at an EV/EBIT ratio for 2024 of approximately 29.5.

Next, let's examine the Free Cash Flow (FCF) Yield, defined as FCF divided by Market Cap. With the current Market Cap at about $250 billion and considering management's forecast of $6 billion in FCF, this results in a FCF yield of 2.4%.

From this analysis, an EV/EBIT ratio of about 29.5 for 2024 seems relatively steep, especially with revenue growth projections of 13%-14%. Although an increase in EBIT is anticipated due to a projected improvement in margins—and potentially even higher Earnings Per Share (EPS) owing to share repurchases—the valuation of 29.5 suggests that significant future growth is already factored into the price. This raises questions about Netflix's ability to sustain such growth levels to justify the current valuation. Given the limited margin of safety, my valuation estimate places the fair value of Netflix's shares somewhere between $375 and $450. This reflects a cautious stance towards the company's valuation, considering the high expectations embedded in its current market price.

Conclusion

Netflix has demonstrated a commendable churn rate and customer loyalty, which, from a personal standpoint, makes it a more valuable subscription than Amazon Prime or Disney+—the latter of which I have recently canceled. This preference stems from Netflix's consistent delivery of compelling and entertaining new content, which distinguishes it significantly from its competitors.

When considering room for growth, the landscape appears complex. Competition within the streaming industry often seems to revolve around platforms vying against each other rather than directly challenging Netflix. Netflix's development trajectory—in terms of membership growth, profitability, and content success—appears to significantly outpace that of competitors like Disney+. This observation leads to the inference that Netflix may have transcended the so-called "streaming wars," positioning itself in a league of its own.

Reflecting on the company's performance over recent years, it's clear that Netflix's management has made several strategic decisions that have steered the company towards success. However, when evaluating the stock from a financial perspective, with fair value estimates ranging between $375 to $350, my intuition and a personal margin of safety suggest that Netflix's stock is currently overvalued. Despite this, given the company's strong performance and potential for future growth, Netflix remains a prominent entity on my watchlist.

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is not invested in Netflix .