#23 Kraft Heinz - King of Impairments

#23 Kraft Heinz - King of Impairments

Can the new CEO turn things around?

Dear readers,

thank you for being here and for your interest in my work! If you like this article and if you want to support my work, please feel free to subscribe! Please read the disclaimer at the end of this article. This is not an investment advice!

Introduction

The Kraft Heinz Company, listed on Nasdaq as KHC 0.00%↑, is a leading food and beverage corporation with a declared mission of making life delicious. In 2023, the company reported net sales of approximately $27 billion, highlighting its dedication to growing both iconic and emerging brands on a global scale. Kraft Heinz emphasizes consumer-centric strategies, scalability, and agility to expand its presence across six product platforms, all while committing to sustainable and ethical practices aimed at contributing positively to global health and food accessibility.

The company's genesis stems from the merger on July 2, 2015, between Kraft Foods Group, Inc. and H.J. Heinz Holding Corporation, resulting in the formation of The Kraft Heinz Company. This rebranding also included the renaming of H.J. Heinz Company to Kraft Heinz Foods Company (KHFC).

Kraft Heinz operates on a fiscal year basis, ending on the last Saturday of December each year, with the report mentioning fiscal years 2021 through 2023 as examples. The company is structured into two main geographic segments: North America and International. However, significant organizational changes were announced in the fourth quarter of 2023, leading to a segmentation strategy that divides the International segment further into Europe and Pacific Developed Markets (EPDM or International Developed Markets), West and East Emerging Markets (WEEM), and Asia Emerging Markets (AEM). Starting in the first quarter of 2024, the company plans to reorganize its reporting segments into North America and International Developed Markets, with WEEM and AEM being combined into a single Emerging Markets segment.

Intellectual property, including trademarks and patents, is considered a critical asset for Kraft Heinz. The company owns significant trademarks such as Kraft, Oscar Mayer, and Heinz in North America, and Heinz, ABC, and Master internationally. These trademarks are essential for the business's operation and are protected as long as they remain in use or their registration is maintained. Additionally, Kraft Heinz licenses brands like Capri Sun for the North American market and has granted and received perpetual licenses for specific intellectual property rights, including for the Kraft and Velveeta brands in certain cheese products, as part of its agreement with Groupe Lactalis.

Kraft Heinz also holds numerous patents worldwide, covering a range of inventions from packaging techniques to product-specific processes. While the patent portfolio is significant to the company's business, the loss of one or a group of patents is not expected to materially impact the company adversely. This emphasis on intellectual property underlines Kraft Heinz's focus on innovation, brand strength, and the strategic protection of its products and processes.

Kraft Heinz sells its products through a combination of its own sales organizations and independent brokers, agents, and distributors, catering to a wide range of outlets including grocery stores, convenience stores, pharmacies, mass merchants, foodservice distributors, institutions (like hotels and hospitals), and various e-commerce platforms. The company has a significant global presence, with sales in different regions around the world. In 2023, the five largest customers in its North America segment represented about 46% of the segment's net sales, while the top five customers in the International segment accounted for 14% of its International net sales. Notably, Walmart Inc. was Kraft Heinz's largest customer, accounting for approximately 21% of the company's net sales in 2023 and 2022, and about 22% in 2021, indicating a substantial reliance on Walmart across both North American and International segments.

As of the end of 2023, Kraft Heinz organized its sales around six consumer-driven product platforms: Taste Elevation, Fast Fresh Meals, Easy Meals Made Better, Real Food Snacking, Flavorful Hydration, and Easy Indulgent Desserts. These platforms are designed to cater to specific consumer needs and preferences, and they play a crucial role in the company's strategic planning and resource allocation. Each platform is assigned a specific role—Grow, Energize, or Stabilize—indicating its expected contribution to the business, with these roles varying by segment and market. This structured approach allows Kraft Heinz to effectively manage and organize its vast product categories and brands. The company is also reviewing these platforms and roles to ensure they align with its future growth strategies, hinting at possible adjustments to better meet evolving consumer demands and market dynamics.

Buffett as an Indicator for Quality? Not in this case

In 2019, Warren Buffett openly admitted to overpaying for Kraft, highlighting a rare moment of candor about an investment misstep. Despite this acknowledgment, he expressed no plans to reduce Berkshire Hathaway's significant stake, approximately 26.7%, in Kraft Heinz. Since the merger's completion in 2015, Kraft Heinz's stock has seen a substantial decline, shedding 54.2% of its value. The stock has been trading within a range of approximately $30 to $40 since 2019. Typically, an investment by Warren Buffett is seen as a strong endorsement of a company's quality, value, and potential underpricing. However, Kraft Heinz has proven to be an exception, challenging the usual optimism that accompanies Buffett's investment choices.

New CEO and Leadership Team

The Kraft Heinz Company is at a critical juncture as it ushers in a new era of leadership, marked by the appointment of Carlos Abrams-Rivera as Chief Executive Officer effective January 1, 2024. This transition occurs in a backdrop of both anticipation and skepticism, as Abrams-Rivera, retaining his current role as President of the North America Zone, steps up to replace Miguel Patricio, who transitions to Non-Executive Chair of the Board after leading the company through years of turbulent market conditions and strategic reorientations since 2019.

The company also announced a revamped Executive Leadership Team, aiming to steer Kraft Heinz towards profitable growth and a more dynamic omnichannel strategy. Yet, these changes prompt a closer examination of the challenges that lie ahead for the new leadership amidst ongoing industry disruptions and evolving consumer preferences.

Pedro Navio's promotion to President of North America, Willem Brandt's appointment as President of Europe and Pacific Developed Markets, Bruno Keller's elevation to President of West and East Emerging Markets, Cory Onell's new role as Chief Omnichannel Sales & Asia Emerging Markets Officer, and Diana Frost's advancement to Chief Growth Officer, collectively represent a significant reshuffling of the deck. However, the real test for these leaders will be their ability to translate strategic visions into tangible results, particularly in revitalizing brand innovation and navigating the complex web of global market dynamics.

While the leadership transition and strategic refocus suggest a proactive approach to tackling the company’s challenges, it remains to be seen how these changes will address the fundamental issues that have plagued Kraft Heinz in recent years, such as brand relevance in a rapidly changing consumer landscape and the need for sustained innovation and market adaptation.

Critically, the effectiveness of this leadership overhaul will be measured by its impact on reversing the trend of underperformance and steering Kraft Heinz towards a path of renewed growth and market leadership. The incoming CEO and the new leadership team face the daunting task of revitalizing a conglomerate that has struggled to find its footing in the face of intense competition and shifting consumer demands. As such, while these appointments herald a new chapter for Kraft Heinz, they also underscore the immense pressure and scrutiny under which these leaders will operate to reinvigorate the company’s legacy brands and forge a successful path forward.

Longterm Prospects according to Kraft Heinz

In presenting its long-term financial strategy, The Kraft Heinz Company has outlined a growth algorithm that largely maintains its previous targets, with a noteworthy shift from focusing on Adjusted EBITDA to setting a new target for Adjusted Operating Income. This move signifies an attempt by the company to better align its organizational metrics with overall shareholder return, promoting a sense of enhanced ownership across the enterprise.

The specified targets include:

Organic Net Sales growth of 2% to 3%, suggesting a modest but steady revenue increase from the company’s core business operations.

Adjusted Operating Income growth of 4% to 6%, indicating an expectation for profit growth from operating activities after adjustments for non-recurring items.

Adjusted EPS growth of 6% to 8%, aiming for a significant rise in profitability as measured on a per-share basis, which is particularly relevant for investors.

A Free Cash Flow Conversion target of approximately 100%, which underscores the company's efficiency in converting profits into free cash flow.

While these targets reflect an optimistic view of Kraft Heinz's future financial performance, they also invite scrutiny. The transition to focusing on Adjusted Operating Income over Adjusted EBITDA could be seen as a move to adopt a metric that potentially offers a more favorable depiction of profitability.

This change, while potentially creating a stronger connection to shareholder returns, may also obscure the impact of significant operational expenses, giving a skewed picture of the company’s operational efficiency and long-term sustainability.

Furthermore, the targets for growth in organic net sales and adjusted EPS, although seemingly robust, must be viewed in the context of the company's recent performance, market position, and the competitive landscape of the food and beverage industry. Achieving consistent organic growth in a mature market requires innovative strategies and a strong competitive edge, both of which Kraft Heinz must continually demonstrate amidst changing consumer preferences and intense competition. The aim for a 100% free cash flow conversion rate is ambitious and highlights the company’s focus on financial efficiency. However, it also sets a high bar that leaves little room for underperformance or unexpected market conditions.

It will be essential for Kraft Heinz to balance this target with the need for investment in innovation, brand development, and market expansion to sustain long-term growth. In summary, while Kraft Heinz's long-term financial targets project a narrative of growth and operational efficiency, they also necessitate a critical examination of the assumptions underlying these targets and the strategies in place to achieve them. The shift in financial metrics and the ambitious targets underscore the need for transparency, adaptability, and strategic foresight in navigating the challenges of the global food and beverage market.

What about the brands?

A strong brand distinguishes itself through a combination of key attributes that ensure its success and longevity in the marketplace. It features a distinctive identity, complete with a unique logo and visual style, paired with consistent messaging across all communications. The cornerstone of any strong brand is the high quality of its products or services, fostering customer loyalty and encouraging brand advocacy. An emotional connection with the audience, underpinned by shared values and aspirations, elevates the brand experience beyond mere transactions. High brand awareness and a clear competitive advantage, whether through innovation, customer service, or quality, solidify its market presence. Adaptability allows the brand to evolve with changing consumer preferences and trends, maintaining its relevance. Additionally, a positive reputation, cultivated through ethical practices and community engagement, alongside a commanding market position, underscore the brand's strength. Together, these elements form the foundation of a strong brand, capable of navigating challenges and achieving sustained growth.

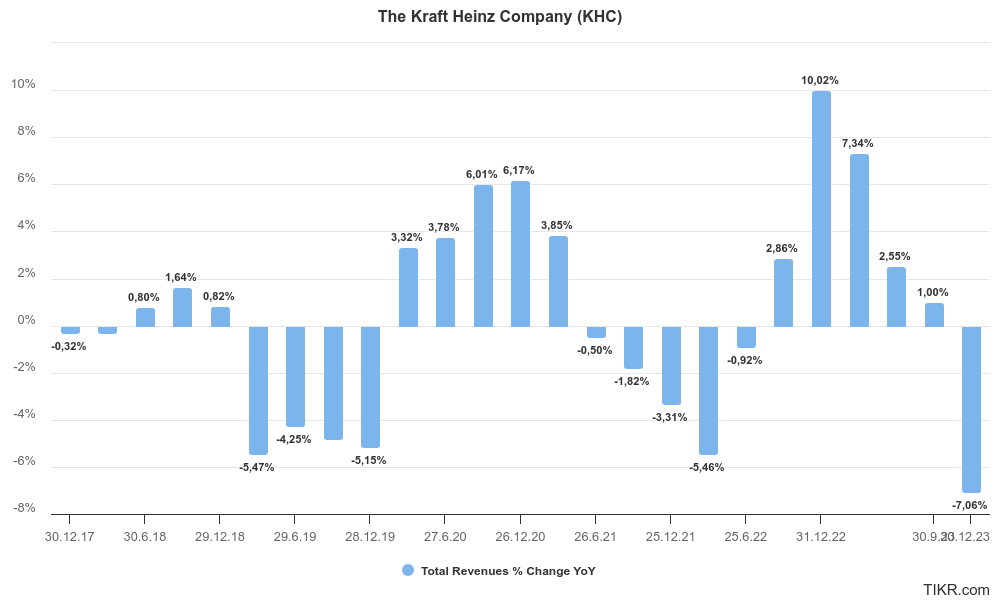

Net Sales and Gross Margin

Pricing power is a crucial indicator of a brand's strength, often highlighted through vivid presentations during earnings calls and analyst days, where Kraft Heinz brands are frequently showcased as leaders in their categories, commanding a strong market position. To evaluate the strength of Kraft Heinz based on available information in the annual report, we will delve into an analysis of its sales and gross margin trends, alongside the valuation of its brands.

Kraft Heinz's annual report provides detailed insights into the factors influencing its Net Sales development, which will be the focus of our examination using data from the last four 10-K reports. From this data, it's evident that Kraft Heinz has been consistently increasing its prices, with notable increases observed in the past two years. However, this strategy has led to significant volume losses over the last three years, particularly within its key North America segment. This trend highlights the challenges and trade-offs associated with wielding pricing power in a competitive market environment.

Kraft Heinz has demonstrated its capability to raise prices to a certain extent, but does this effectively offset rising costs? To assess this, examining the Gross Profit Margin is crucial. The margin exhibits significant fluctuations, underscored by a discernible downward trend. Since 2017, Kraft Heinz has experienced a decline of approximately 3 percentage points in its Gross Margin.

What does this imply? The pricing power of Kraft Heinz brands appears to be constrained. Despite price increases, the company faces volume losses, and these adjustments have not been sufficient to fully counterbalance cost hikes.

Brand Valuation - History of Impairments

Over recent years, The Kraft Heinz Company has navigated the challenging landscape of maintaining the value of its brand portfolio, evidenced by significant non-cash impairment losses recorded from 2018 through 2023. These impairments reflect adjustments based on annual tests and evolving market conditions, underscoring the company's efforts to realign its brand valuation with current market realities. Here's a summary of the impairments during this period:

2023:

Total Impairment Losses: $152 million, attributed to brands including Maxwell House and Cool Whip among others, primarily due to increased discount rates, declining revenue growth, and other market inputs.

2022:

Q2 Impairment Losses: $395 million for Maxwell House, Miracle Whip, Jet Puffed, and Classico, driven by downward revisions in operating margins and increased discount rates.

Q3 Impairment Losses: $67 million for Jet Puffed and Plasmon, related to reduced revenue growth assumptions.

2021:

Initial Impairment Losses: $69 million for Plasmon and Maxwell House, largely due to downward revised revenue expectations and increased discount rates.

End-of-Year Impairment: $1.2 billion for the Kraft brand following the monetization of certain brand portions, highlighting reduced brand valuation.

2020:

Total Impairment Loss: $1.1 billion across nine brands including Oscar Mayer, Maxwell House, and Velveeta among others, with losses attributed to revised revenue and margin expectations and increased discount rates.

2019:

Total Impairment Loss: $474 million affecting brands like Miracle Whip, Velveeta, and Maxwell House, primarily due to an increase in discount rate assumptions.

Additional Maxwell House Impairment: $213 million in the fourth quarter, resulting from specific fourth-quarter conditions.

2018:

Early-Year Impairment: $101 million related to the Quero brand in Brazil due to sales and margin declines.

Mid-Year Impairment: $215 million for Smart Ones, driven by reduced investment expectations and continued sales declines.

End-of-Year Impairment: A significant $8.6 billion loss affecting Kraft, Oscar Mayer, Philadelphia, Velveeta, and ABC, due to deteriorating sales and market conditions.

These reported impairments from 2018 to 2023 highlight the dynamic and challenging nature of brand valuation within the competitive food and beverage industry. The Kraft Heinz Company's strategic responses, including adjusting its brand strategies and operational plans, reflect its commitment to navigating these challenges while aiming for sustainable growth and value creation.

Since 2015 Kraft Heinz has recognized total impairments amounting to $12.6 billion on its brands, yet the company continues to hold indefinite-lived intangible assets valued at over $38.5 billion.

Brand Impairment testing assumptions

An intriguing, albeit less conventional, gauge of brand strength lies in the assumptions used for annual impairment tests, particularly the long-term growth rate. This metric doesn't just heavily influence the calculated fair value of a brand; it also reflects management's expectations for the brand's future trajectory. The evolution of these assumptions over time offers insightful perspectives.

For instance, the impairment test in 2018 revealed that the company anticipated a maximum long-term growth rate of 4.7% for reporting units and between 2.1% and 4.0% for brands. Fast forward to 2023, and these expectations have been adjusted downwards to 2.5% for reporting units and to 1.9% and 2.0% for brands, showcasing a significant shift in the company's outlook.

For investors, this information is crucial. It sets a realistic expectation for sales growth, indicating that surpassing these figures would be either a commendable achievement or a deviation from projected paths. Essentially, these growth rate assumptions serve as a barometer for the company's long-term confidence in its brands, underscoring the importance of scrutinizing these forecasts to gauge potential investment outcomes.

Additional Goodwill Impairments

From 2018 through 2023, The Kraft Heinz Company faced several challenges, leading to substantial goodwill impairment losses, reflecting adjustments in its business outlook and market conditions. Here's a concise overview of the goodwill impairments recorded during this period:

2023:

Total Goodwill Impairment Loss: Approximately $510 million, including $452 million for the Canada and North America Coffee (CNAC) reporting unit within the North America segment, and $58 million for the Continental Europe reporting unit within the International segment. These impairments were primarily due to increased discount rates, higher interest rates, and declines in market capitalization.

2022:

Initial Interim Impairment Loss: Around $235 million recognized in the North America segment, including significant losses related to the Canada Retail ($221 million) and Puerto Rico ($14 million) reporting units, driven by revised outlooks for operating margin and increased discount rates due to higher interest rates.

Q3 Impairment Loss: Approximately $220 million related to the CNAC reporting unit, driven by reduced revenue growth assumptions and negative macroeconomic factors, including increased interest rates and unfavorable foreign currency exchange rates.

2021:

Initial Goodwill Impairment Loss: About $35 million related to the Puerto Rico reporting unit within the North America segment, following a revised downward outlook for net sales.

Additional Impairment: A loss of $53 million related to the EMEA East and LATAM reporting units within the International segment, representing all of the goodwill for those reporting units after acquisitions changed their composition.

2020:

Total Goodwill Impairment Loss: $1.8 billion related to the U.S. Foodservice, Canada Retail, Canada Foodservice, and EMEA East reporting units across various segments, primarily due to updated enterprise strategy and five-year operating plan which revised downward revenue growth and profitability expectations.

Reorganization-Related Impairment: Losses of $83 million and $143 million related to the ANJ and LATAM reporting units, respectively, within the International segment, driven by a reporting unit reorganization that affected their fair value.

2019:

First Quarter Interim Impairment Loss: $620 million across three reporting units (EMEA East, Brazil, and Latin America Exports) within the International segment, largely due to circumstances that arose in the first quarter.

Second Quarter Annual Impairment Test: A $118 million loss related to the U.S. Refrigerated reporting unit within the United States segment due to increased discount rate assumptions.

Fourth Quarter Interim Impairment Loss: $453 million for the Australia and New Zealand, and Latin America Exports reporting units within the International segment, attributed to circumstances that emerged in the fourth quarter.

2018:

Second Quarter Impairment Loss: $133 million related to the Australia and New Zealand reporting unit within the International segment, primarily due to margin declines.

Fourth Quarter Interim Impairment Loss: $6.9 billion for five reporting units, including U.S. Refrigerated, Canada Retail, Southeast Asia, Northeast Asia, and Other Latin America, reflecting a reassessment of their fair value due to changing market conditions.

These recorded impairments from 2018 to 2023 highlight the significant impact of evolving market conditions, strategic reassessments, and macroeconomic factors on The Kraft Heinz Company's financial position and its ongoing efforts to align its business strategy with the market realities.

The company has recognized a total impairment of $11.8 billion, yet it still reports a substantial Goodwill balance of approximately $30.4 billion on its balance sheet.

Deteriorating Margins, low Return on Capital

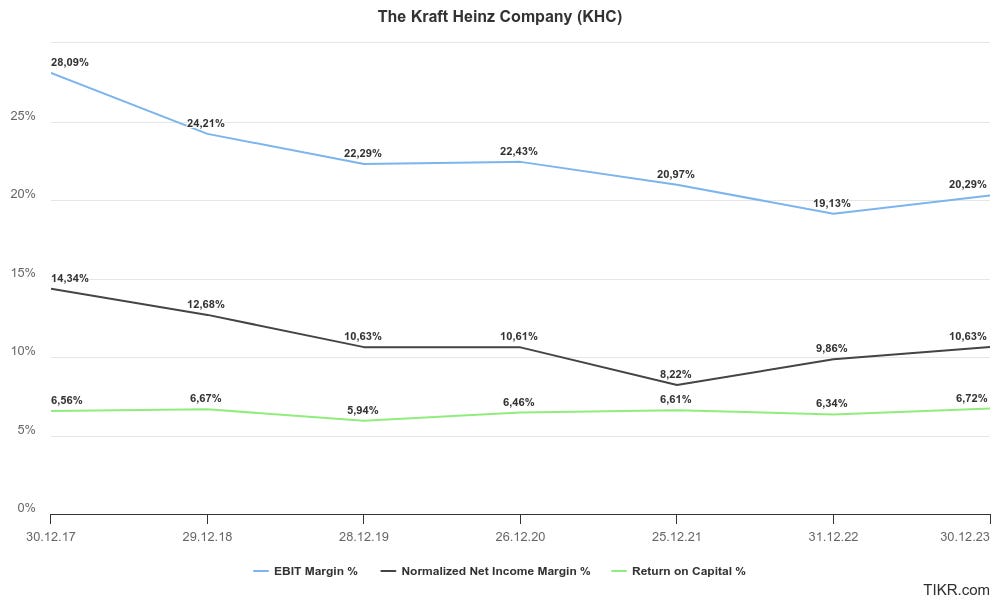

Let's delve into the concrete financial metrics of Kraft Heinz. An examination of the numbers reveals a steady erosion in both EBIT Margin and Normalized Income Margin since 2017. Over the past seven years, there's been a significant downturn, with the company losing nearly 8% of its EBIT Margin—a situation that can only be described as disastrous. Despite this, the Return on Capital (ROIC) has remained surprisingly stable, oscillating between 6% and 7%. However, a 7% ROIC, in my analysis, falls short of the mark for what would be considered robust for a high-quality business. This level of return is, from my perspective, too modest and underscores the financial challenges facing Kraft Heinz.

Share Repurchases and Dividends

On November 27, 2023, Kraft Heinz announced a Board-approved share repurchase program, enabling the company to buy back up to $3.0 billion of its common stock through December 26, 2026. As of December 30, 2023, approximately $2.7 billion remained available for repurchase under this program. This initiative is separate from any share buybacks aimed at mitigating the dilutive impact of equity-based compensation.

Calculating the expenditures, Kraft Heinz allocated $300 million to acquire approximately 8.3 million shares. As of December 2023, there were around 1.227 billion shares outstanding. This purchase effectively decreased the total number of shares by roughly 0.6%. Extrapolating from the cost of repurchasing shares for $300 million, Kraft Heinz has the financial capability to buy back approximately 75 million more shares. Such an action would lead to a 6.1% reduction in the total number of outstanding shares.

Without preempting the discussion on the stock's attractive valuation, this repurchase program appears to be a very sensible move to me.

Kraft Heinz has been consistently distributing a quarterly dividend, culminating in an annual payout of $1.60 per share since 2019. This approach was adopted after a challenging year in 2018 when the company decided to scale back on dividend payments as a strategy to decrease its debt levels. Currently, the dividend yield is approximately 4.7%, aligning with the historical average.

Valuation

In the realm of investing, everything ultimately boils down to the valuation of the business. With Kraft Heinz displaying relative stability in revenue growth (or lack thereof) and margin trends (downward but stabilizing), conducting a DCF (Discounted Cash Flow) valuation was relatively straightforward. Employing conservative assumptions that are more cautious than Kraft Heinz management's long-term outlook—for instance, a long-term growth rate of 0.8% in my model versus the 2-3% expected by management—and assuming stable margins (with no improvement anticipated on my part), the stock emerges as attractively valued. I calculated the fair value of the stock to be in the range of $41 to $46 per share. Considering the current price of $34, this presents a significant margin of safety of about 128% (average fair value of $44 compared to the current $34).

Turning to my preferred valuation metrics, EV/EBIT and P/E ratios, based on normalized earnings, the stock appears inexpensive relative to the average of the past three years. With current multiples standing at 11.21x and 11.31x compared to historical averages of 13.29x and 13.89x, this suggests a potential upside of approximately 17%.

In summary, the valuation analysis of Kraft Heinz points to the company being undervalued, even when taking into account the previously discussed business challenges.

Conclusion

Since its creation through a merger in 2015, Kraft Heinz has experienced a steady decline in both its operational performance and stock price. Warren Buffett, as its largest shareholder, remains committed to the company, though the strength of its brands may not be as robust as the management team suggests. A history of impairments and management and accounting challenges point to deep-seated issues within the company. The new CEO faces significant hurdles ahead. The long-term prospects outlined by management do not seem particularly ambitious, yet they still present a considerable challenge for Kraft Heinz to achieve. I am skeptical about the possibility of significant improvement in the coming years, given the current state of the brand portfolio, which appears to lack the necessary strength. Despite these challenges, the stock appears to be undervalued, indicating that the market is exercising caution.

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is not invested in KHC.

Good points about impairments and changes in the assumptions.