#41 Albertsons - What’s the right price tag?

An exciting investment case

Dear readers,

thank you for being here and for your interest in my work! If you like this article and if you want to support my work, please feel free to subscribe and like! Please read the disclaimer at the end of this article. This is not an investment advice!

As a longtime shareholder of Kroger, I have been interested in the proposed merger with Albertsons from the very beginning. Initially, my focus was on this transaction from the perspective of the buyer, Kroger. However, I recently came across an article highlighting that hedge funds are heavily betting on a successful merger by acquiring significant amounts of Albertsons stock. The intriguing aspect is that the offered price for Albertsons is higher than its current stock price. This piqued my interest, prompting me to delve deeper into the details of this merger.

For those who are interested, I wrote about Kroger and the merger in this article several months ago. I will not repeat any aspects of it and some issues with the merger. You can find my post here:

Now let's take a look at the merger agreement and Albertsons and the investment case.

The merger

In a significant move within the grocery retail sector, Kroger KR 0.00%↑ and Albertsons ACI 0.00%↑ announced their merger on October 13, 2022. The agreement marked a substantial shift in the industry, with Kroger agreeing to acquire all outstanding shares of Albertsons' common and preferred stock at an initial purchase price of $34.10 per share. This price was later adjusted to $27.25 per share following a $6.85 per share special pre-closing cash dividend paid to Albertsons shareholders on January 20, 2023.

To navigate the complex regulatory landscape and gain the necessary clearances for the merger, Kroger and Albertsons devised a comprehensive divestiture plan. Initially, the plan included the potential creation of a new entity, SpinCo, which would house some of Albertsons' assets. However, this approach evolved, and on September 8, 2023, Kroger and Albertsons entered into a definitive agreement with C&S Wholesale Grocers, LLC. This agreement involved the sale of 413 stores, along with various brands and distribution centers, to C&S. The divestiture plan was further amended on April 22, 2024, adding another 166 stores and additional assets to ensure regulatory compliance and maintain a competitive market landscape.

To finance this ambitious merger, Kroger secured a $17.4 billion senior unsecured bridge term loan facility. As the merger process advanced and alternative financing was arranged, this facility was reduced to $10.65 billion. Additionally, Kroger entered into term loan credit agreements totaling $4.75 billion to cover a significant portion of the merger costs.

The merger faced substantial regulatory challenges. The Federal Trade Commission (FTC) and several states filed suits to block the merger, citing antitrust concerns. This led to a series of preliminary injunction hearings and administrative proceedings scheduled throughout 2024. Kroger and Albertsons committed not to close the merger until these legal issues were resolved, demonstrating their dedication to regulatory compliance.

If the merger agreement is terminated by either party in connection with the occurrence of the Outside Date, and all closing conditions other than regulatory approval have been satisfied at the time of such termination, Kroger will be obligated to pay a termination fee of $600 million to Albertsons.

The investment case

The proposed merger has created a unique situation with from my point of view two bullish points.

Firstly, Kroger's offer of $27.25 per share is significantly higher than Albertsons' current stock price, presenting an upside potential of approximately 36%. If the FTC authorizes this merger, the stock is likely to immediately reach this level, acting as a decisive catalyst to unlock Albertsons' value.

The other point is that I think Albertsons is undervalued at $20. As one of the largest food retailers in the United States, Albertsons operates 2,269 stores across 34 states and the District of Columbia as of June 15, 2024. Their diverse portfolio includes more than 20 well-known banners such as Albertsons, Safeway, Vons, Pavilions, Randalls, Tom Thumb, Carrs, Jewel-Osco, Acme, Shaw's, Star Market, United Supermarkets, Market Street, Haggen, Kings Food Markets, and Balducci's Food Lovers Market. With a dedicated workforce of approximately 285,000 employees, Albertsons serve an average of 36.3 million customers each week. As of June 15, 2024, they also operate 1,725 pharmacies, 1,346 in-store branded coffee shops, 403 fuel centers, 22 distribution centers, 19 manufacturing facilities, and various digital platforms.

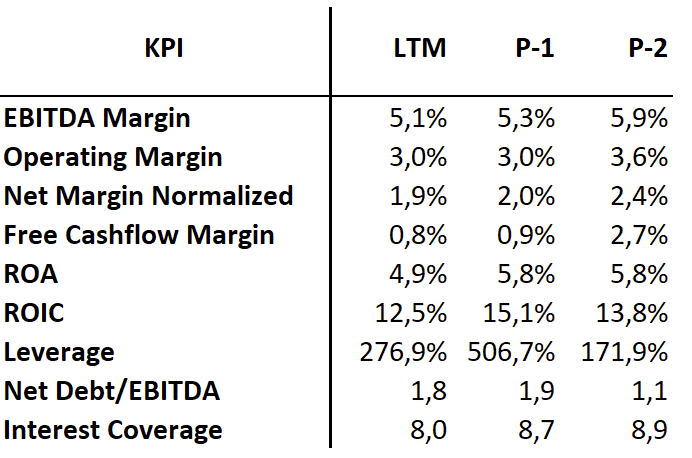

Looking into some financial metrics we see that the company has solid margins and returns. What stands out is the high leverage, thats because of very low equity. In terms of Net debt covered by EBITDA the metrics seems to be ok, but its something that we should keep in mind.

Albertsons' size is easily underestimated, but the company has over $79 billion in sales and $26 billion in total assets.

For my DCF valuation, I assume that sales will grow at a very low CAGR of 1.5% over the five-year planning period, with stable normalized margins and cash flows. Based on this straightforward base case, I estimate a fair value per share of approximately $26, resulting in an equity value for the entire company of about $15 billion, indicating an undervaluation of around 28%.

Analyzing the forward P/E and EV/EBIT ratios, the company is trading at very low levels. While significant growth is not anticipated, the current price is highly attractive for a company with such solid financials. This may not represent an exceptional price for an extraordinary business, but it certainly is a wonderful price for a solid business.

Conclusion

Albertsons is one of the largest retailers in the US and is set to merge with Kroger, which has offered to pay $27 per share, significantly higher than Albertsons' current share price of around $20. While there are substantial risks that the merger might not be approved by the FTC, both parties are making concerted efforts to facilitate its success. If the merger does not proceed, Albertsons will still receive a substantial cash payment of $600 million.

Beyond the merger, I believe the company is undervalued, with an estimated intrinsic value of about $26 per share, aligning closely with Kroger's offer. Despite being a solid company, one major drawback is its largest shareholder, Cerberus Capital Management, which tends to prioritize its own interests over the company's. This is evident from last year's debt-financed special dividend and the company's very low equity.

In my view, the risk-to-reward profile here is promising, as Albertsons' stock is trading at low levels. Therefore, I have decided to invest in Albertsons stock to take advantage of this compelling opportunity.

Thank you once again for being here and for your interest! If you enjoyed my analysis, please consider leaving a "like" and subscribing. Your support means a lot!

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is invested in this stock.

Good insight, as usual. So if I understand you correctly, you are not betting on the merger arbitrage spread - which reflects the likelihood of the deal falling through? (Whether this likelihood is correctly estimated is a different story.)