#42 Target Corporation

When will it hit again?

Dear readers,

thank you for being here and for your interest in my work! If you like this article and if you want to support my work, please feel free to subscribe and like! Please read the disclaimer at the end of this article. This is not an investment advice!

About Target Corporation

Target Corporation is a leading general merchandise retailer in the United States, offering a wide range of products, including food items, apparel, accessories, home décor, electronics, toys, and seasonal merchandise. The company also provides beauty and household essentials, and in-store amenities such as Target Café, Target Optical, and Starbucks. Target sells its products through its 1,963 stores and digital channels, including Target.com. Founded in 1902 and headquartered in Minneapolis, Minnesota, Target continues to be a prominent player in the retail industry.

Targets development in the most recent years

Over the past five years, Target's TGT 0.00%↑ stock experienced significant growth, peaking at around $250 per share in 2021 and 2022. However, it saw a dramatic decline, dropping to approximately $100 per share in 2023. Currently, the stock is gradually recovering, though the journey has been quite volatile. As of now, Target's stock is trading at roughly $150 per share.

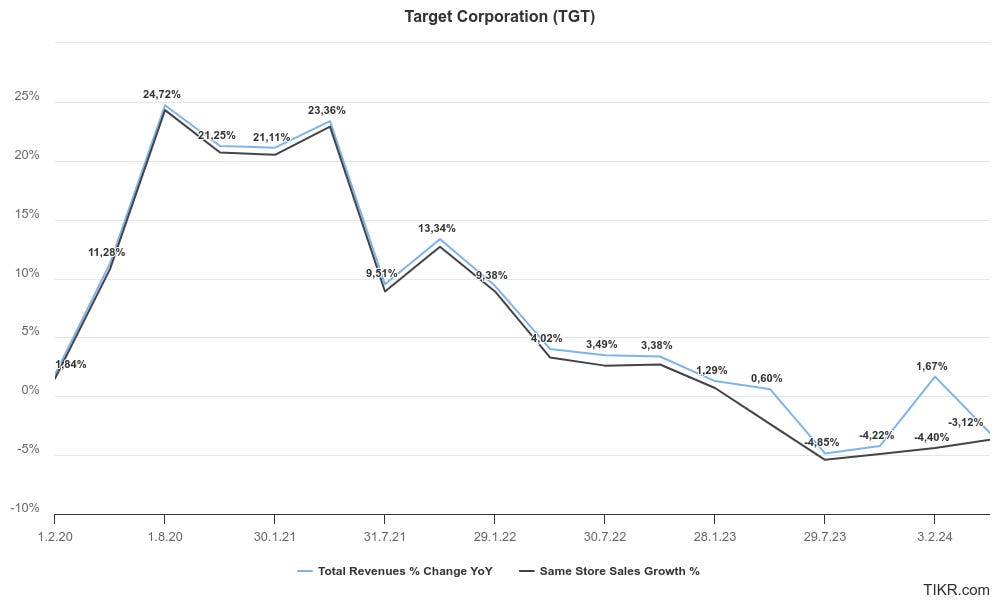

Until 2022, especially during the COVID-19 years, Target experienced an impressive growth trajectory. In 2020, the company increased net sales by nearly 20%, primarily driven by same-store sales, while maintaining high EBIT margins and strong returns on capital.

As conditions began to normalize, Target's growth rates also "normalized" and decreased significantly. In 2022, the world was further destabilized by Russia's attack on Ukraine, plunging the economy into a new crisis before fully recovering from the previous one. Inflation and high interest rates returned, creating a challenging environment for Target. Consequently, sales not only stopped growing but even declined over the past four quarters.

Target's significant exposure to discretionary items posed a major challenge. Only 24% of its sales come from food and beverages, while the remaining 76% are from products that consumers can forgo when finances are tight and they seek more affordable options. Additionally, negative press during Pride Month in June 2023 further contributed to the decline in sales.

This downward trend affected not only net sales but also margins and returns. Both metrics declined rapidly from their peak levels in 2021, nearly halving in value. While this is now part of the company's history, the focus shifts to what can be expected in the near and long term future.

Targets strategy to go forward

In the latest earnings call for Q1 2025, Target's management highlighted several strategic pillars for future success. Here are a few key points that I believe are particularly important.

Loyalty Program Target Circle

Target Circle, Target Corporation's loyalty program, has undergone a significant transformation aimed at enhancing customer engagement and providing greater value to shoppers. Launched initially as a straightforward rewards program, Target Circle was relaunched in April 2024 with a fresh, user-friendly design and a host of additional benefits tailored to meet the needs of its members.

Target's membership options include:

Target Circle: A free membership offering personalized deals, member-exclusive sales, and automatic application of discounts at checkout.

Target Circle Card: Formerly Target RedCard, provides an extra 5% off daily, extended return times, and free two-day shipping on many items.

Target Circle 360: A paid membership featuring unlimited free same-day delivery, free two-day shipping, preferred shoppers, and access to Shipt Marketplace.

Target Circle saw its membership grow by over 1 million new members in the first quarter of 2024. This surge brought the total membership well over the 100 million mark.

From my point of view, a loyalty program is an effective strategy to boost customer loyalty and encourage repeat purchases. Customers are often motivated to buy a little more to earn points or take advantage of promotions. However, the critical challenge is that nearly all retail chains have recognized this strategy and developed their own loyalty programs. To truly stand out, a loyalty program must be exceptionally attractive and unique. I'm not entirely sure if Target's program meets these criteria, but the potential is there.

Invest in stores and new openings

Target's long-term vision is ambitious. The company plans to open more than 300 new stores over the next decade. This is not just about increasing the number of stores; it's about strategically positioning Target to serve communities better and drive profitable growth.

In addition to opening new locations, Target is also committed to continuously investing in the majority of its existing stores. These investments are focused on enhancing the shopping experience, improving operational efficiency, and keeping the stores fresh and appealing to customers.

Target's reputation is already established as having more appealing stores compared to competitors like Costco and Walmart. This distinction can be a significant advantage, but it requires continuous investment and meticulous maintenance. When executed well, it can lead to better margins by attracting more customers and enhancing their shopping experience. However, if not managed properly, these efforts can merely result in higher costs and reduced margins.

Roundel

Roundel is Target's advertising business, crucial in deepening the connection between Target, its guests, and its vendors.

Roundel has been highlighted as the fastest-growing part of Target's business. During the Q1 2025 earnings call, it was noted that Roundel's revenue grew by more than 20% in the quarter.

At the heart of Roundel's success is its ability to leverage Target’s rich customer data to offer personalized and highly targeted advertising solutions. By analyzing purchasing behavior and demographic information, Roundel helps brands reach their desired audiences more effectively.

It is an interesting business opportunity for Target, but I doubt it will significantly contribute to Target's revenue and operating profit in the near term.

Outlook for FY 2025

During the Q1 2025 earnings call, Target Corporation laid out a detailed and optimistic guidance for the upcoming quarter and the rest of the year.

For the second quarter of 2024, Target is projecting a modest but hopeful increase in comparable sales, ranging from 0% to 2%. This cautious yet optimistic outlook underscores Target’s commitment to returning to growth by focusing on key drivers of performance. Additionally, the company is guiding an earnings per share (EPS) range of $1.95 to $2.35, with the midpoint representing a significant growth rate of approximately 20% over the same period last year. This expected improvement reflects Target's efforts to build on the profit rate expansion seen in recent quarters.

Looking at the full year, Target is maintaining its previous guidance of a comparable sales increase between 0% and 2%, a range that captures various economic scenarios and reflects the company’s prudent approach given the current uncertainties. For EPS, Target anticipates a range of $8.60 to $9.60.

Central to Target's strategy is a focus on operational excellence. The company is committed to maintaining appropriate inventory levels, improving in-stock positions, and driving efficiencies across their operations to support sustained profitability.

Investment in growth remains a priority, with Target planning to allocate $3 billion to $4 billion in capital expenditures for the year to open new stores, remodel existing ones, enhance digital capabilities, and modernize the supply chain.

Additionally, Target has seen favorable trends in inventory shrinkage and is optimistic about continuing to improve this metric.

Dividends and Stock Repurchases

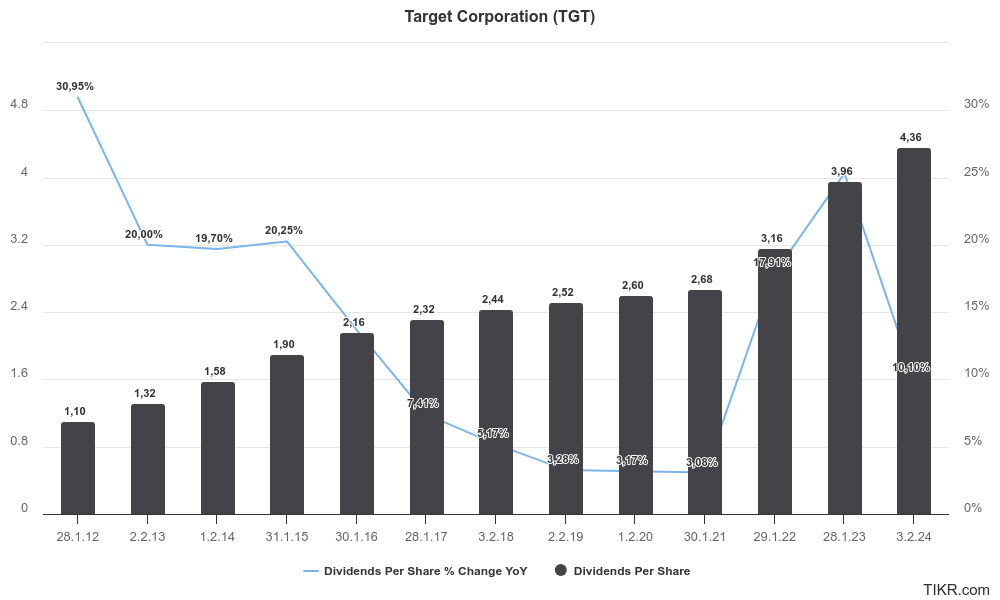

What stands out positively is Targets increases in dividend payments. Notably, the last dividend increase was Target's 228th consecutive dividend since October 1967, and 2024 is set to be the 53rd consecutive year of annual dividend increases.

On August 11, 2021, Target's Board of Directors authorized a $15 billion share repurchase program without an expiration date. Under this program, Target has repurchased 23.8 million shares at an average price of $223.52, totaling $5.3 billion. As of today, $9.7 billion remains available for further repurchases. Target's management is committed to maintaining its debt levels, with stock repurchases not being their top priority. During the Q1 2025 earnings call, CFO Fiddelke mentioned that Target might consider using excess cash for stock repurchases later in the year.

Stock Valuation

Base Case Assumptions

For the time being, I believe that Targets years of strong growth are over and shareholders and investors must accept the fact, that future growth will be max. in the midteens. While same store sales will improve also a little bit the majority of growth will come from new stores and its loyalty program. Margin improvement will come from inventory shrink normalization, slightly improved supply chain and operational efficiencies and from a stronger contribution from own brands. But in general margins will normalize at a level before the COVID highs.

Revenue Growth

In the DCF Model, a five-year detailed planning period is used, projecting a 3.0% Compound Annual Growth Rate (CAGR). This trajectory anticipates Targets revenue to reach about 120 billion in FY 2029.

EBIT Margin

In the last twelve months, Targets EBIT margin was 5.5%. For the DCF Model, I have normalized this margin to an average of 6.0%.

Normalized Net Income Margin

Based on the EBIT margin, the Last Twelve Months (LTM) Normalized Net Income margin stands at 3.9%. Moving forward, it is estimated to stabilize around 4.3%.

Free Cash Flow

My Free Cash Flow assumptions include a Net Capex ratio as a percentage of sales (Net Capex = Capex - Depreciation) of 1.1%, reflecting the average of recent years. Working Capital, expressed as a percentage of sales, is determined by the average Working Capital over the past years, calculated at 4.7% of net sales. The Free Cash Flow estimation does not adjust for stock-based compensation. This results into a normalized free cash flow margin of about 3.3%.

WACC

The Weighted Average Cost of Capital (WACC) is set at 7.5%.

Results

Based on these assumptions, Targets equity value is estimated at $60.4 billion. Dividing this by the current number of shares, we derive a fair value per share of $132. In comparison to its latest stock price of $150 the stock appears slightly overvalued.

Adjusting the WACC to 8.5% would lower the fair value per share to $116, while a decrease in WACC to 7.0% would increase it to $149 per share.

Scenarios

Bull Case Scenario:

In an optimistic scenario, assuming a CAGR for revenue of 4.5%, an EBIT Margin of 7.3%, and a normalized net income margin of 4.8%, the fair value per share would be $150. In this scenario the stock appears to be fairly valued.

Bear Case Scenario:

Conversely, in a pessimistic scenario with a CAGR for revenue of 0.4%, an EBIT Margin of 4.7%, and a normalized net income margin of 3.8%, the fair value per share would be $111. In this scenario the stock also appears to be overvalued.

P/E and EV/EBIT

To further validate the valuation estimate, let's examine my preferred metrics: forward EV/EBIT and P/E. Considering the five-year historical averages of 15.22x for EV/EBIT and 17.86x for P/E, the current valuation of 14.13x EV/EBIT and 15.47x P/E indicates a fair valuation or even a slight undervaluation.

I believe the stock has been significantly overvalued for a long time. Target's long-term growth prospects never justified such high valuations, with the stock trading at over 20 times normalized earnings or more than 15 times EV/EBIT. Consequently, historical averages of these metrics are not particularly useful in this context.

Conclusion

From my perspective, Target has fully recognized its challenges and is optimistic about addressing them. During the Q1 2025 earnings call, the leadership expressed confidence in meeting financial goals for 2024 through strategic investments, operational improvements, and enhanced customer engagement. However, Target has lost market share to competitors like Costco and Walmart. While I believe Target will return to growth, margins will remain under pressure and won't reach the highs of 2021 sustainably. Given the low growth prospects and strong competition, I see better investment opportunities elsewhere. I will retain my position in Target but won't increase it.

Thank you once again for being here and for your interest! If you enjoyed my analysis, please consider leaving a "like" and subscribing. Your support means a lot!

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is invested in this stock.