#45 Expedia - The travel loser?

Can Expedia keep up with Airbnb and Booking Holdings?

Dear readers,

thank you for being here and for your interest in my work! If you like this article and if you want to support my work, please feel free to subscribe and like! Please read the disclaimer at the end of this article. This is not an investment advice!

As announced in my investment journal, this is my first post that includes content exclusively for paying subscribers. However, if you're a free subscriber or prefer to stay on the free tier, don't worry—there will still be plenty of valuable content available at no cost. I truly appreciate your support, and thank you for being part of this community!

About Expedia Group

Expedia Group, Inc. EXPE 0.00%↑ is a major player in the online travel industry, offering a broad portfolio of consumer brands like Expedia, Hotels.com, and Vrbo. These brands provide travelers with a wide range of options to research, plan, and book their trips, including access to over 3 million lodging properties and more than 500 airlines.

Founded over 25 years ago as one of the first online travel agencies, Expedia has grown significantly through strategic acquisitions. However, managing multiple brands became complex, leading to inefficiencies. In 2020, Expedia adopted a platform operating model to streamline operations, optimize marketing, and unify its brand strategy.

Recently, Expedia has focused on building customer loyalty and increasing app usage, resulting in higher engagement. In 2023, the company unified its technology by integrating Hotels.com and Vrbo into the Brand Expedia platform. Expedia also launched One Key, a loyalty program that allows customers to earn and redeem rewards across its brands, further enhancing the customer experience.

Expedia is strongest in North America, where it remains the leading player in this critical and lucrative market. The North American market, particularly in the U.S., is highly mature and dominated by large hotel chains with strong brands, loyalty programs, and significant leverage in negotiations due to their scale and reach. In contrast, more fragmented markets like Europe and Asia—two of the world’s top travel destinations—are where Booking Holdings holds a dominant position.

These conditions present notable challenges for Expedia. However, from an economic standpoint, the U.S. is home to much of the world’s wealth and remains the strongest economic region globally. This translates into substantial potential, with a large population eager to travel both within North America and abroad.

Let’s take a quick look at Expedia’s recent metrics and performance over the past few years. In the last twelve months, Expedia generated $13.2 billion in revenue, reflecting a year-over-year growth of 8.2%.

Expedia’s Gross Booking Volume is a key driver of its revenue. Over the last twelve months, this volume reached $106 billion. The revenue margin, which represents the percentage of gross booking volume that translates into revenue for Expedia, can vary significantly throughout the year. In 2023, this margin stood at 12.3%, surpassing pre-pandemic levels of around 11.3%. This increase highlights Expedia’s ability to capture more value from its bookings as the travel industry continues to recover.

The return on invested capital (ROIC) has also seen a slight uptick, currently at 4.3%, though this figure remains relatively modest. The company’s operating margin peaked in Q2 2024, reaching 12%. Meanwhile, its net profit margin stands at 6.1%, marking an improvement compared to its average since 2022.

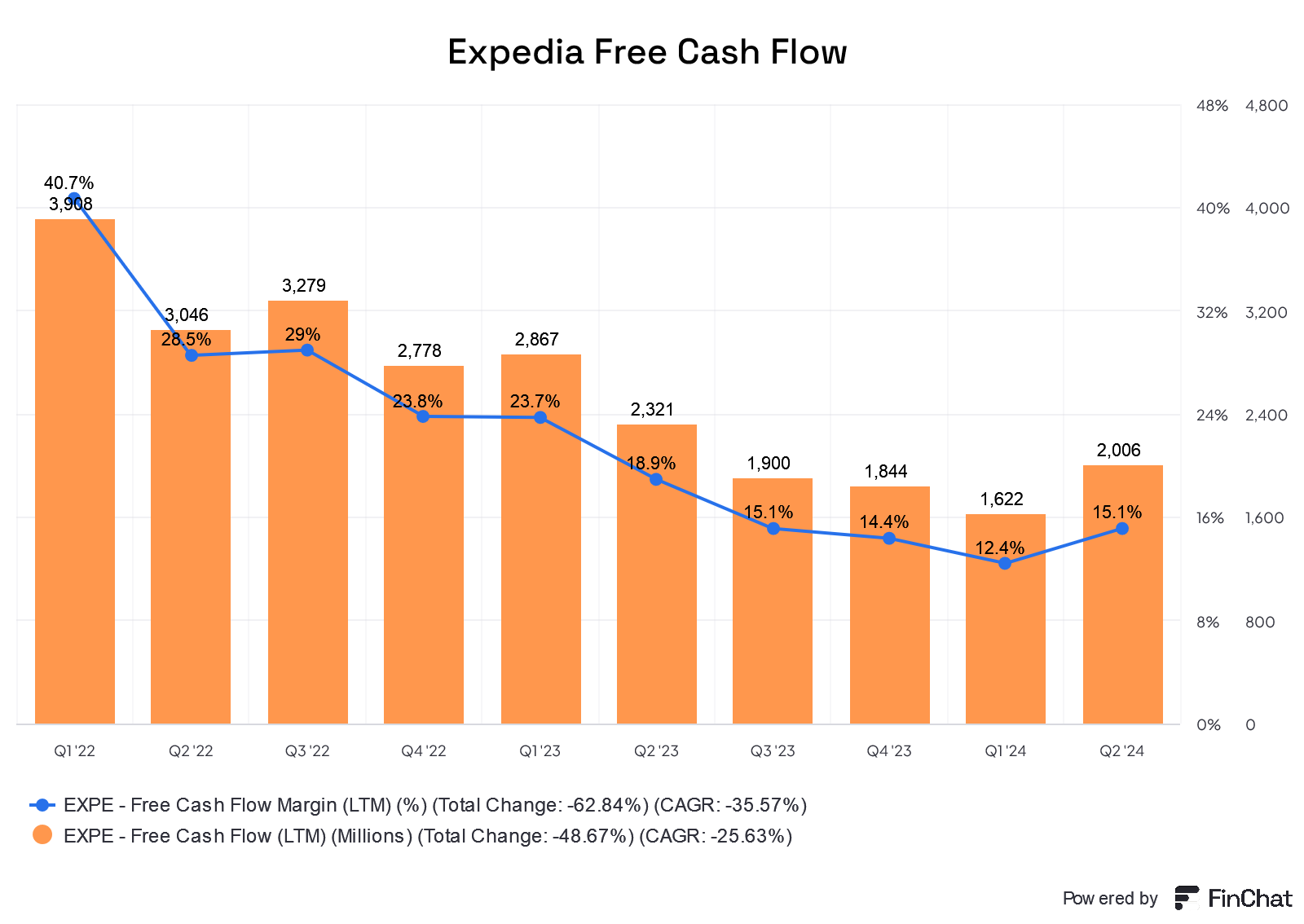

One of Expedia’s key strengths is its ability to generate robust free cash flow, largely due to its strong emphasis on the merchant model, where payments are collected upfront. While it may appear that free cash flow has decreased over time, this is primarily due to the normalization of growth as the travel industry recovers. As growth stabilizes, the impact of changes in deferred merchant bookings has diminished, which naturally leads to a lower free cash flow compared to the rapid recovery period. However, this does not undermine the company’s strong cash generation capabilities..

What is the case for investing in Expedia and what is the case against?

Keep reading with a 7-day free trial

Subscribe to Kroker Equity Research to keep reading this post and get 7 days of free access to the full post archives.