#47 SoFi Technologies

Isn't it just a bank?

Dear Readers,

Thank you for being here and showing interest in my work! Your support means the world to me. If you enjoyed this article and would like to see more, please consider subscribing and giving it a like—it really helps grow our community of investors.

For those interested in accessing exclusive premium content, consider upgrading to the paid tier for full access. Your support enables me to continue providing valuable insights and content.

Thank you for your continued support!

And if you want to get a free premium subscription, here is your chance! Share this post with your friends or click the Refer button. For three referrals you will get 1 month of free premium, for 5 referrals 3 months and for 25 referrals 6 months!

Please read the disclaimer at the end of this article. This is not an investment advice!

About SoFi Technologies

Ticker: SOFI 0.00%↑

Market cap: $7.8 billion

SoFi describes itself as a member-centric, one-stop shop for financial services that provides a wide array of products enabling its members to borrow, save, spend, invest, and protect their money. The company’s mission is to help its members achieve financial independence to realize their ambitions. Importantly, SoFi defines financial independence not merely as wealth but as the ability for its members to meet personal goals at various life stages, such as buying a home, starting a family, or pursuing a desired career. Their overarching goal is to empower members to “Get Your Money Right.”

This description aims to clearly distinguish SoFi from a traditional banking business. Unlike conventional banks that typically rely on physical branches, SoFi operates almost entirely online through its mobile app and website. This digital-first approach enables a more streamlined, user-friendly experience, particularly appealing to tech-savvy consumers.

SoFi leverages cutting-edge technology to innovate and set itself apart from traditional banks. As a fintech company, it offers advanced services such as robo-advisors for investing, cryptocurrency trading, and personalized financial planning tools—features that are not commonly available at traditional banks.

Moreover, SoFi’s strategy centers on building a comprehensive ecosystem where users can manage nearly all aspects of their financial lives. The company actively promotes cross-selling its products, providing incentives for customers who use multiple SoFi services. This approach results in a more holistic and integrated financial experience than what most traditional banks can offer.

This is what SoFi wants us to think when we read their business description in the 10-K, but what is the real business like? Let's take a look.

Business Model Analysis - Bank or “fintech”?

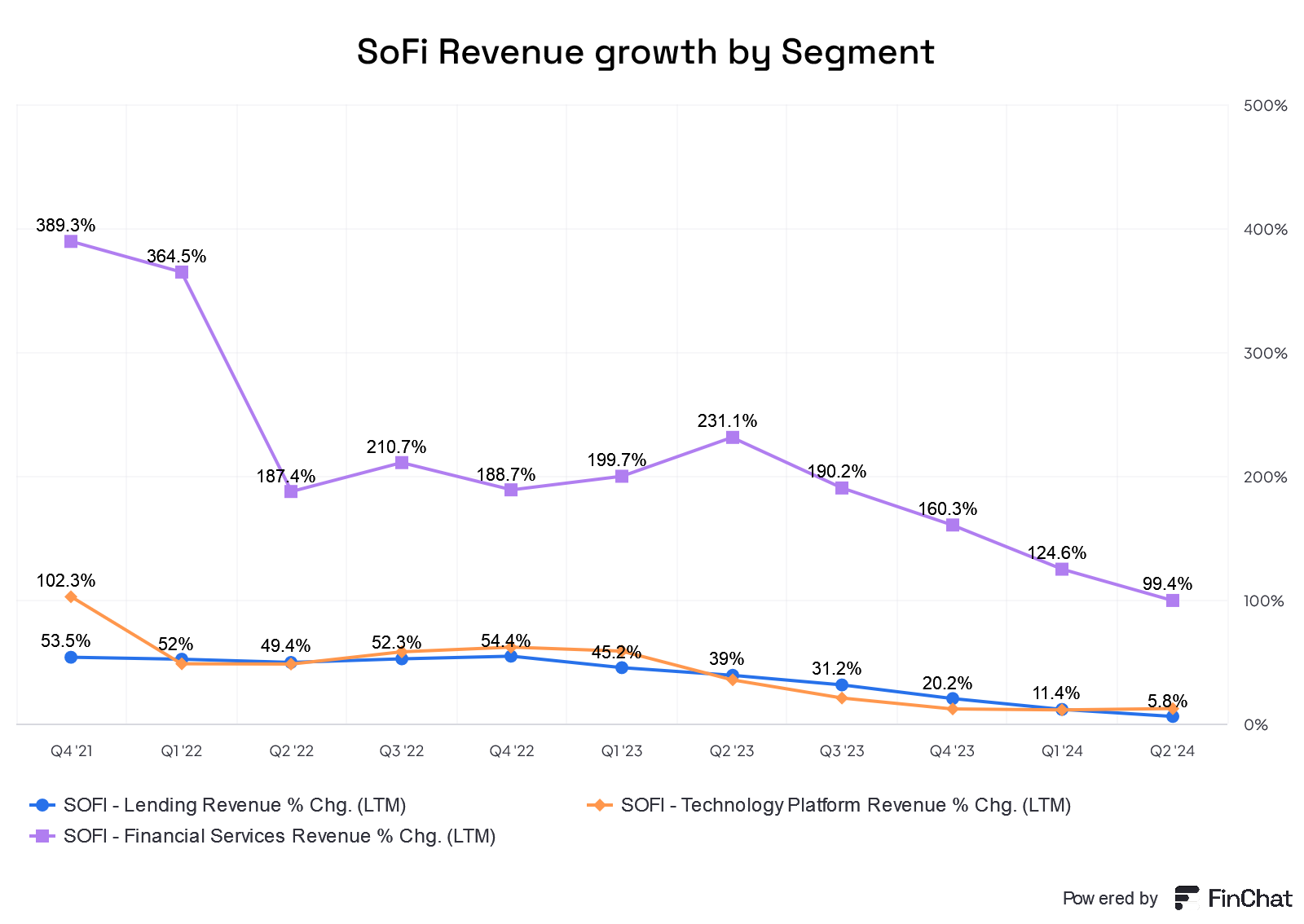

In the last 12 months arround 73% of revenue and 77% of profit contribution came from the Lending segment. The Lending segment at SoFi encompasses three primary products: personal loans, student loans, and home loans, as well as the associated services required to manage these loans. SoFi generates revenue in this segment through several key channels.

First, they recognize gains or losses based on the changes in the value of the loans they hold. These fair values are calculated by themselves (Level 3 fair values) and this practice is very uncommon among financial insitutes, however these changes can create losses and gains. Additionally, SoFi profits from the value changes of portions of these loans that they package and sell as securitization interests. Second, when SoFi sells loans that meet specific requirements, known as true sale requirements, they recognize gains or losses, which also contribute to their revenue.

Another revenue stream comes from servicing fees. SoFi charges fees for managing loans, such as collecting payments or providing customer service, even if they no longer own the loans. The income generated from these fees, along with the changes in the value of their servicing rights, adds to their earnings.

Furthermore, SoFi earns interest on the loans they issue. However, they also incur interest expenses on the money they borrow to fund these loans. The difference between the interest they earn and the interest they pay is known as net interest income, which is a vital component of their revenue in the Lending segment.

From my perspective, these revenue streams look like a traditional bank. What I would like to add here is my personal view on the non-interest income of the lending segment at SoFi. It is significantly driven by fair value accounting and therefore almost impossible to predict. This adds enormous complexity to the business model and to understanding SoFi's overall profitability and business performance.

The Financial Services segment at SoFi includes a variety of products and services that help members manage and grow their money. Key offerings in this segment include SoFi Money, SoFi Invest, the SoFi Credit Card, SoFi Relay, and other financial services like personal finance management and content for both members and financial institutions.

SoFi Money primarily offers checking and savings accounts as well as cash management accounts. These accounts provide a digital banking experience with benefits such as no account fees, early access to paychecks by two days, and a competitive annual percentage yield. SoFi Invest allows members to invest and access financial planning services, making it easier for them to manage their investments digitally. The SoFi Credit Card is another important product in this segment, offering rewards and benefits for everyday spending. Additionally, SoFi Relay helps members manage their personal finances by providing tools and insights.

Revenue in the Financial Services segment comes from several sources. SoFi earns interest income on deposits and pays interest on funds used to provide these services. They also generate revenue through interchange fees, which are small charges paid by merchants when members use their SoFi debit or credit cards. In SoFi Invest, they earn money from pay-for-order flow (a fee from directing trades to specific market makers) and share lending arrangements. Lastly, SoFi earns referral fees when they successfully refer members to other services or products through their platform. Also this segment matches to the business model of a traditionell bank. This segment accounted for 6.5% of revenues and and 11% of contribution profit.

The Technology Platform segment at SoFi focuses on providing the technical infrastructure and solutions that other financial companies need to operate. This segment mainly includes three key components.

First, through Galileo, SoFi offers a platform-as-a-service that provides essential backend services for financial companies. These services include setting up accounts, handling account funding, processing direct deposits, authorizing transactions, managing payments, and checking account balances. Essentially, Galileo provides the technology that powers many of the financial services people use every day.

Second, starting in March 2022, the Technology Platform segment expanded with the acquisition of Technisys. Technisys offers a cloud-native digital and core banking platform, enabling banks and fintechs to build and manage their services more effectively. This addition allows SoFi to generate revenue by selling software licenses and offering related technology solutions.

This segment differentiates SoFi from a “normal” bank as its provides service throughts its platforms Galileo and Technisys. It provides around 20% of revenues of SoFi and 11.5% of contribution profit. The risk here is that Galileo and Technisys are highly dependent on a small number of customers for their revenues. This concentration of revenue creates significant risks for the business. If one of these key customers were to experience financial difficulties, such as bankruptcy, or were to switch to a competitor, this could seriously harm Galileo's and Technisys' financial performance. As many of their customers are fintech and other financial services companies, they are also vulnerable to broader economic challenges that could affect these industries.

Based on this analysis, approximately 80% of revenues and 88% of contribution profit are derived from businesses that are clearly identifiable as banking businesses.

In conclusion, when considering whether SoFi is more of a fintech company or a bank, it appears to lean more towards being a bank than a pure fintech. Why is this distinction important? The valuation of banks and fintech companies differs significantly, with each being assessed based on different criteria and growth potential. Could this perception shift over time? Potentially, if SoFi's technology-driven revenue and contributions were to take a larger share of the overall business. However, based on recent growth trends, this shift does not seem imminent.

Most importantly, SoFi achieved profitability for the first time in Q4 2023 and has successfully maintained it since then. This milestone marks a significant breakthrough for the company.

Now, let’s examine the valuation of SoFi stock and highlight key considerations to watch for.

Keep reading with a 7-day free trial

Subscribe to Kroker Equity Research to keep reading this post and get 7 days of free access to the full post archives.