#86 Spotify - A revisit

Spotify’s Last 3 Years: From Hyper-Growth to First Profits

Spotify’s Last 3 Years: From Hyper-Growth to First Profits

Revisiting Spotify: From Digital Music Giant to Profitability Powerhouse

Over a year ago, I delved into Spotify's position as a dominant force in the digital music landscape, highlighting its expansive user base, innovative features, and the challenges it faced in achieving profitability. At that time, Spotify was investing heavily in content diversification and global expansion, striving to balance growth with financial sustainability.

Fast forward to today, and Spotify has not only sustained its growth but has also reached a significant milestone: its first full year of profitability. With over 675 million monthly active users and 263 million paying subscribers, the company reported a net income of €1.14 billion in 2024. This achievement underscores Spotify's successful strategies in monetization and operational efficiency.

In this follow-up post, we'll analyze the developments that have propelled Spotify to this new level, examining key financial metrics, strategic initiatives, and the broader implications for the streaming industry. Let's explore how Spotify's evolution over the past year reflects its adaptability and foresight in a rapidly changing digital environment.

Growth Trajectory: Rapid Users and Revenue Uptick

Spotify has enjoyed robust growth in users and revenue over the past few years. Its monthly active users (MAUs) nearly doubled from about 345 million at the end of 2020 to 489 million by 2022, and then surged further to 675 million MAUs as of year-end 2024 – a 12% year-over-year jump that year. Paying subscribers (“Premium” users) have climbed alongside the total audience: from 155 million in 2020 to 205 million in 2022, reaching 263 million Premium subscribers by the close of 2024 (11% growth in 2024). This expanding user base underscores Spotify’s success in converting free listeners into paying customers globally.

Revenues have risen in step with user growth. Annual sales grew ~21% in 2021 and another 21% in 2022, reaching €11.73 billion in 2022. This momentum carried through 2023 and 2024 as Spotify continued to add users and nudged prices upward. By 2024, Spotify’s revenue was at an all-time high (€15.67 billion), helped by Premium subscriber gains and a boost in average revenue per user (ARPU) from price increases. In short, Spotify’s top line has maintained a strong growth trajectory over the past three years, fueled by both a larger audience and improved monetization of that audience.

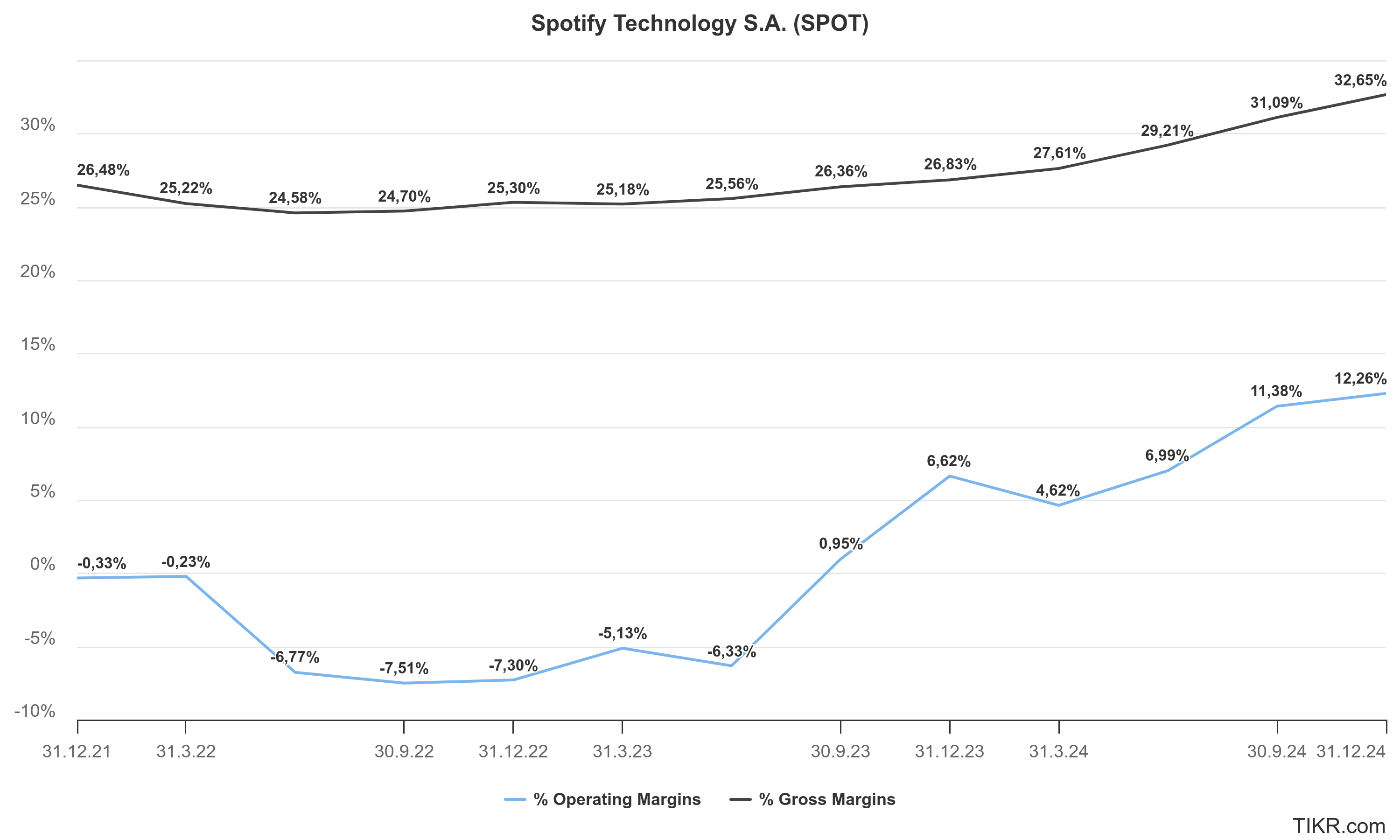

Margin Trends: Gross Margins Up, Operating Losses Down

One of the most impressive shifts in Spotify’s business over the past couple of years has been its gross margin expansion. For a long time, gross margins hovered in the mid-20s — around 25% in 2022 — which isn’t much for a company of Spotify’s size. But by 2024, gross margins had climbed to 30%. That might not sound like a huge leap, but in the world of streaming, where every percentage point is hard-earned, it's a pretty big deal. So, what changed?

A big part of the story is podcasts. Remember when Spotify went on a buying spree a few years back? It spent a ton acquiring studios like Gimlet and Parcast and signed big names to exclusive deals. The problem? These podcast ventures were expensive and didn’t bring in profits fast enough. In 2023, Spotify took a step back, reorganized the whole segment, shut down underperforming content, laid off staff, and got much leaner. This helped cut a lot of content-related costs, and since podcasts had been a drag on margins, cleaning that up gave gross margins a nice lift. The ad-supported segment — which had barely any margin before — even managed to pull off a 12% gross margin by 2024. Not bad for something that was practically break-even not long ago.

Then there’s the pricing. Spotify finally raised its Premium prices in a bunch of countries, including the US and much of Europe. And guess what? People didn’t cancel. Subscriber growth kept chugging along, which means higher revenue per user without higher content costs (since royalties are usually a percentage of revenue). More revenue per user = better margins. Simple as that.

The company also got serious about efficiency. After years of chasing growth at all costs, Spotify started to trim the fat. It cut over 1,500 jobs between 2023 and 2024, pulled back on some marketing spend, and tightened its focus on what’s actually working. That kind of discipline helps margins too, especially when it impacts cost of content delivery and platform operations, which are baked into gross profit.

Lastly, Spotify has been quietly leveling up its ad-tech. Things like dynamic ad insertion in podcasts and self-serve ad tools are helping it squeeze more money out of the same audience — particularly on the free tier. That boost in ad monetization helps push gross margins up without dramatically increasing costs.

Now the big question: is this margin improvement sustainable? In the short term, yeah — these aren’t fluke results. Spotify has been improving margins steadily over multiple quarters, and the shifts in cost structure and pricing are real. But long term, it gets trickier. About 70% of music revenue still goes straight to rights holders, and that dynamic is hard to change. Unless Spotify finds ways to cut out the middlemen, negotiate better deals, or add high-margin revenue streams (like audiobooks or creator tools), gross margin may hit a ceiling around the low-30s.

So while it’s great to see Spotify finally proving it can run a profitable, cash-generating business, investors shouldn’t assume gross margins are going to hit 40% or anything wild like that. For now, though, it’s a big step in the right direction — and a sign that Spotify is maturing into a real business, not just a growth story.

The improvement in profitability is even clearer at the operating level. After years of operating losses, Spotify’s operating income swung from a €659 million loss in 2022 to a positive €1.365 billion in 2024. In other words, the company went from roughly -5.6% operating margin in 2022 to +8.7% in 2024. This dramatic turnaround was enabled by cost-cutting (Spotify pared back staff and content spending in 2023) and operating leverage as revenue grew. 2024 marked Spotify’s first full year of operating profit ever. Additionally, net income turned positive (€1.1 billion in 2024) after years of red ink. In sum, Spotify’s margins are trending in the right direction – gross margins have crept up and the company finally demonstrated it can generate an operating profit after prioritizing growth for so long.

Free Cash Flow: From Breakeven to a Cash Machine

Spotify’s ability to generate free cash flow (FCF) has vastly improved. The company was essentially at cash-flow breakeven a couple of years ago – free cash flow was only €21 million in 2022, a trivial amount for a multi-billion euro business. In 2023, FCF increased to €678 million as operating losses narrowed. Then in 2024, Spotify’s cash generation leapt dramatically: free cash flow jumped to €2.285 billion. This nearly quadrupled FCF vs. 2023, reflecting higher profits and working capital benefits. The business inherently has low capital expenditure needs (Spotify doesn’t spend much on physical infrastructure or hardware), so once it reached profitability, cash flow surged. This FCF can be reinvested into new content, product development, or simply bolster Spotify’s balance sheet – a welcome development for long-term investors who have waited for the model to translate growth into cash.

Future Prospects: Bullish and Bearish Cases

Spotify’s recent progress sets the stage for debates about its future. On one hand, the bullish case has strengthened now that the company is profitable; on the other, skeptics note that challenges remain. Let’s break down both sides:

Bullish case: Spotify is the world’s largest audio platform with 675 million+ users and a strong brand in music streaming. Now that it has achieved scale, each additional subscriber should contribute more to profit, hinting at significant operating leverage ahead. Management has indicated ambitious long-term goals (previously targeting 30–35% gross margins and aggressive revenue growth), and 2024’s results show they’re on the path to those targets. New ventures like podcasts and audiobooks could become high-margin businesses as they mature – Spotify believes podcasting, for example, can eventually reach 30–50% margins. Additionally, Spotify’s recent price hikes in major markets boosted ARPU without a major hit to subscriber growth, suggesting pricing power. With improving margins, strong free cash flow, and still plenty of room to grow (e.g. penetrating emerging markets and converting free users to paid), bulls argue Spotify can compound earnings for years to come.

Bearish case: Despite the optimism, skeptics point out that Spotify still faces formidable headwinds. Competition is fierce – the company must battle deep-pocketed rivals like Apple Music, Amazon Music, and YouTube Music for listeners’ time and money. These competitors often bundle music with other services or hardware, putting pressure on Spotify to keep pricing attractive. Content costs also remain a thorn in the side: the lion’s share of Spotify’s revenue is paid out to record labels, publishers, and artists as royalties. In fact, Spotify shelled out roughly $10 billion in 2024 alone to music rights holders, an enormous expense that inherently caps gross margins. This means Spotify’s margin improvements could level off unless it finds new higher-margin income streams. Moreover, the recent profitability required heavy cost-cutting – any misstep in cost control or a renewed spending spree on content (say, big exclusive podcast deals) could put it back in the red. Growth is also slowing: total MAU growth decelerated to +12% in 2024 from over 20% in prior years. If user growth or engagement disappoints (perhaps due to competition or saturation in key markets), Spotify might have a harder time justifying its rich valuation. In short, bears worry that Spotify’s business model – essentially acting as a middleman between users and content owners – inherently has lower margins and that the company’s best growth days might be behind it.

Valuation Multiples and Investor Sentiment

Spotify’s stock price has skyrocketed alongside its improving financials, which has stretched its valuation multiples. As of early 2025, the company trades at roughly 5.7× enterprise value-to-revenue, a high ratio for a business whose gross margins are only around 30%. In other words, investors are valuing Spotify at about 5–6 times its annual sales. On an earnings basis, the stock also isn’t cheap – because profits have just started to materialize, the price/earnings multiple is lofty (well above market average). Even looking forward, Spotify is priced around 41× EV/EBIT based on 2025 projections, reflecting a lot of optimism for future growth. These rich multiples imply that the market expects Spotify to continue expanding revenue at a healthy clip and further improve margins in the coming years. The stock’s huge run-up in 2024 (when it jumped over 150%) was driven by the narrative of a “turnaround to profitability”.

Now, at near record-high share prices, investors are debating whether that optimism is fully baked in. Long-term investors should be aware that much of Spotify’s anticipated success (scaling up earnings and cash flow) is already reflected in its valuation. Any slip in execution or growth could lead to a significant pullback, while conversely, if Spotify exceeds expectations, the stock could justify its premium. Essentially, buying at these levels requires confidence in Spotify’s ability to keep the positive trend going.

Conclusion

Spotify’s last three years have been transformative. The company went from aggressive expansion with slim margins to finally delivering a meaningful profit and hefty free cash flow in 2024. It has cemented itself as a leader in audio streaming, growing its user base to nearly 700 million globally and branching out into podcasts and other audio formats. For long-term investors, Spotify presents a mix of promise and questions. On the one hand, it now has a proven path to profitability and a dominant platform – a combination that could yield compounding returns if user growth and margin expansion continue. On the other hand, the road ahead is not without obstacles: competition is intense, content costs remain high, and the stock’s valuation leaves little room for error.

In the end, Spotify has evolved from a growth-first story into a more mature business balancing growth with profitability. The bullish case sees this as just the beginning of a new chapter of sustained earnings growth, whereas the bearish case urges caution given the structural challenges and high expectations priced in. As with any investment, it comes down to whether you believe Spotify can maintain its tune of strong growth and improved efficiency in the years ahead. For now, the company has given investors plenty of reason to applaud – but the market will be watching closely to see if Spotify can keep hitting the right notes.

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is invested in the mentioned stock.