#9 Stock Watchlist - 2/2023

#9 Stock Watchlist - 2/2023

Valuation Updates on Walt Disney, Mondelez, Adobe and PUMA

This Stock Watchlist update focuses on four diverse yet impactful players: Disney, Adobe, Mondelez, and PUMA. Each of these companies holds a unique position in their respective industries, from entertainment and digital media to consumer goods and sports apparel.

Disney, Adobe, and Mondelez are all companies that have successfully navigated the changing media and consumer landscape. Disney, a well-known entertainment company, offers a variety of content and streaming services. Adobe is a leader in creative software, and Mondelez is known for its snack brands. These companies demonstrate the enduring demand for consumer products. Finally, PUMA, a significant player in the athletic and fashion industries, demonstrates the convergence of sports, lifestyle, and performance. Let us examine each company's latest developments and update our estimates of its intrinsic value.

Here you can download the latest Stock Watchlist:

Before discussing the four different companies, I want to highlight a great quote from the recently passed investor legend Charlie Munger:

All intelligent investing is value investing – acquiring more than you are paying for. You must value the business in order to value the stock.

Walt Disney

Several weeks ago, The Walt Disney Company DIS 0.00%↑ reported its FY 2023 earnings and released its 10-K.

In fiscal year 2023, the company underwent a significant reorganization, consolidating its operations into three primary business segments: Entertainment, Sports, and Experiences. The restructuring involved integrating the former Disney Media and Entertainment Distribution segment into the newly formed Entertainment and Sports segments. Furthermore, a portion of the Consumer Products revenue is now recognized under the Entertainment segment, in line with royalties from merchandise licensing revenue generated on intellectual property created by this segment.

Financially, Disney's performance in 2023 was mixed. The company reported a 7% increase in revenue, amounting to $88.9 billion. However, net income attributable to Disney declined, falling by $0.8 billion to settle at $2.4 billion, in contrast to $3.1 billion in the prior year. This decline was also reflected in diluted earnings per share (EPS) from continuing operations attributable to Disney, which decreased to $1.29 from the previous year's $1.75. Factors that contributed to the decrease in EPS included increased restructuring and impairment charges, as well as reduced operating income in the Entertainment segment. However, these were partially offset by higher operating income in the Experiences segment and gains from investments, which contrasted with investment losses in the previous year.

In terms of revenue, service revenues for fiscal year 2023 increased by 7% to $79.6 billion. The company's growth was driven by increased activity in theme parks and resorts, higher subscription revenue, a surge in theatrical distribution revenue, and a comparison to the previous year's revenue reduction due to the Content License Early Termination. However, these gains were partially offset by declines in advertising revenue, TV/VOD distribution sales, and affiliate revenue.

Product revenues increased by 10% to $9.3 billion, driven mainly by higher sales volumes of merchandise, food, and beverages at theme parks and resorts. However, this was partially offset by lower home entertainment volumes.

Expenditures for fiscal year 2023 increased by 9% to $53.1 billion, reflecting higher programming and production costs, inflation, and expanded volumes at theme parks and resorts. Additionally, the cost of products increased by 11% to $6.1 billion, mainly due to higher sales volumes and cost inflation at theme parks and resorts. It is worth noting that selling, general, administrative, and other costs decreased by 6% to $15.3 billion, primarily due to reduced marketing expenses in Entertainment Direct-to-Consumer. This was slightly offset by heightened theatrical marketing costs and an increase in marketing expenses at theme parks and resorts.

The company experienced a 4% increase in depreciation and amortization, totaling $5.4 billion. This was due to higher depreciation at domestic parks and resorts, including accelerated depreciation related to the closure of Star Wars: Galactic Starcruiser, and depreciation for the Disney Wish.

In fiscal year 2023, restructuring and impairment charges amounted to $3,892 million, a significant increase from the $237 million recorded in fiscal year 2022. The increase was primarily due to severance costs and various impairments resulting from exiting businesses in Russia.

Additionally, Disney's investment in DraftKings resulted in a gain of $169 million, which was sold in the current fiscal year. This is a significant improvement from the $663 million non-cash loss recorded in fiscal year 2022.

Net interest expense increased because of higher average rates, while equity in the income of investees slightly decreased to $782 million. The effective income tax rate for fiscal year 2023 was 28.9%.

In summary, Disney's fiscal year 2023 was a year of strategic reorganization and mixed financial performance. The company experienced revenue growth and operational expansions in certain areas, but also faced increased costs, restructuring charges, and variable investment returns.

Management Outlook for FY 2024

For the fiscal year 2024, Disney has outlined several key outlooks and plans:

Experiences Business Growth: Disney is optimistic about the long-term prospects of its Experiences business and plans to make significant investments over the next decade to drive growth. These investments will gradually increase in the first few years and ramp up more substantially towards the latter half of the decade. It is worth noting that some of the investments in theme parks in Shanghai and Hong Kong will be funded through joint venture cash flows.

Performance Expectations: Disney expects strong annual operating income growth in its Experiences segment, driven by continued strong performance at its International Parks and Disney Cruise Line. Solid growth is also expected throughout the year for the Domestic Parks & Experiences, with more substantial growth anticipated towards the end of the year due to challenging comparisons in the first half.

Free Cash Flow Generation: The company anticipates generating around $8 billion in free cash flow, a substantial year-over-year increase, and approaching pre-pandemic levels. This strong growth in free cash flow, combined with a solid balance sheet, will allow Disney to achieve its investment and shareholder return objectives. Additionally, there is a plan to declare a dividend by the end of the calendar year, with the possibility of further increases in shareholder returns as earnings and free cash flow continue to grow.

Capital Expenditures: Disney's projected capital expenditures (capex) for fiscal year 2024 are expected to be approximately $6 billion, which is an increase of about $1 billion from the previous year. The higher spending in the Experiences segment is the main driver of this increase, including investment in the Cruise business in preparation for the launch of three new ships in fiscal years 2025 and 2026.

Theatrical Releases: Disney anticipates a robust theatrical lineup in 2024, featuring several films tied to popular franchises, including 'Deadpool 3 featuring Wolverine,' 'Kingdom of the Planet of the Apes,' 'Inside Out 2,' and new installments from the 'Toy Story,' 'Frozen,' 'Zootopia,' and 'Avatar' franchises. The company views this as an opportunity to further enhance its Disney Experiences into a more successful cash-flow generating business.

Strategic Investments and Growth Focus: Over the past five years, the return on invested capital in Disney's Domestic Parks has almost doubled, with significant increases across the entire Experiences portfolio. The company intends to accelerate growth in its Experiences business through strategic investments over the next decade, utilizing its intellectual property, technology, and creativity. The company aims to drive profitable growth and value creation as it transitions from a period of fixing to a new era of building. It is expected that free cash flow will significantly improve in fiscal 2024, approaching pre-COVID levels.

Valuation Update

The current trading price of Disney stock, approximately $93, appears to be appropriately valued when considered in light of its estimated intrinsic worth.

Current Fair Value: $94

Projected Fair Value in Two Years: $101

This valuation suggests that the market price closely aligns with Disney's current estimated fair value, indicating a well-balanced evaluation of its stock at the moment.

What to keep in mind and look for?

As investors consider Disney's prospects for the upcoming year, there are several key factors to keep in mind:

Strategic Investments and Expansion: Disney has made significant investments in its Experiences segment, particularly in theme parks and the Disney Cruise Line, which are expected to drive long-term growth. It is important for investors to monitor how these investments impact overall financial performance and how they are managed in the context of global economic conditions.

Performance of New Theatrical Releases: The performance of upcoming films from popular franchises could significantly impact revenue. It is important to note that success in the box office can also have a positive effect on merchandise sales and theme park attendance.

Direct-to-Consumer (DTC) Segment Growth: The DTC segment, including Disney+, Hulu, and ESPN+, remains a key focus. Watch for subscriber growth, content development strategies, and how Disney navigates the competitive streaming landscape.

Free Cash Flow Generation: Disney anticipates a significant increase in free cash flow, nearing pre-pandemic levels. This is a crucial metric for evaluating the company's financial health and its ability to sustain dividends and make strategic investments.

Conclusion on Disney

When evaluating Disney's stock, investors must navigate a landscape rich in both potential and challenges. Looking ahead, several pivotal factors shape the company's trajectory.

Firstly, the succession plan following Bob Iger's tenure, concluding in 2026, looms large. Leadership transitions are often watershed moments for corporations, significantly influencing strategic direction and investor sentiment. The capabilities and vision of Iger's successor will be crucial in navigating Disney through the changing media and entertainment landscape.

Additionally, the involvement of activist hedge funds, such as Trian Fund Management's recent nomination of Nelson Peltz to Disney's board, may signal changes in the company's strategy or financial practices, potentially marking a new chapter in Disney's corporate governance and strategic approach.

Regarding stock valuation, current assessments indicate that Disney's stock is fairly valued, reflecting its earnings prospects and market positioning. However, this valuation requires continuous reassessment against the backdrop of changing market conditions and the company's financial performance.

Content creation, which is a cornerstone of Disney's success, faces its own set of challenges. The box office performance in 2023 was not up to par, highlighting the challenges of content monetization in a competitive industry. Disney's continued growth depends on their ability to consistently produce attractive and profitable content.

The ongoing strike in Hollywood is an industry-wide issue that adds another layer of complexity, potentially delaying content production and impacting revenue streams from both direct-to-consumer platforms and theatrical releases.

Disney's direct-to-consumer (DTC) business is under pressure due to profitability challenges in the streaming market, despite promising growth in subscriber numbers on platforms like Disney+. To ensure future success, substantial content investment and strategic maneuvering in this segment are crucial.

Despite the challenges, Disney's stock holds substantial potential due to its strong brand legacy, diverse content portfolio, and strategic expansions, particularly in the Experiences segment. However, there are risks ahead. Investors should closely monitor how Disney adapts to industry trends, shifts in consumer behavior, and broader economic conditions.

In conclusion, Disney's stock presents a complex investment picture. The blend of growth potential, driven by a robust content pipeline and strategic investments, is counterbalanced by leadership transition uncertainties, activist investor influences, and profitability pressures in key business segments. For investors, the key will be to balance these elements, aligning them with their investment goals and risk appetite, to navigate the future of investing in Disney.

Mondelez International

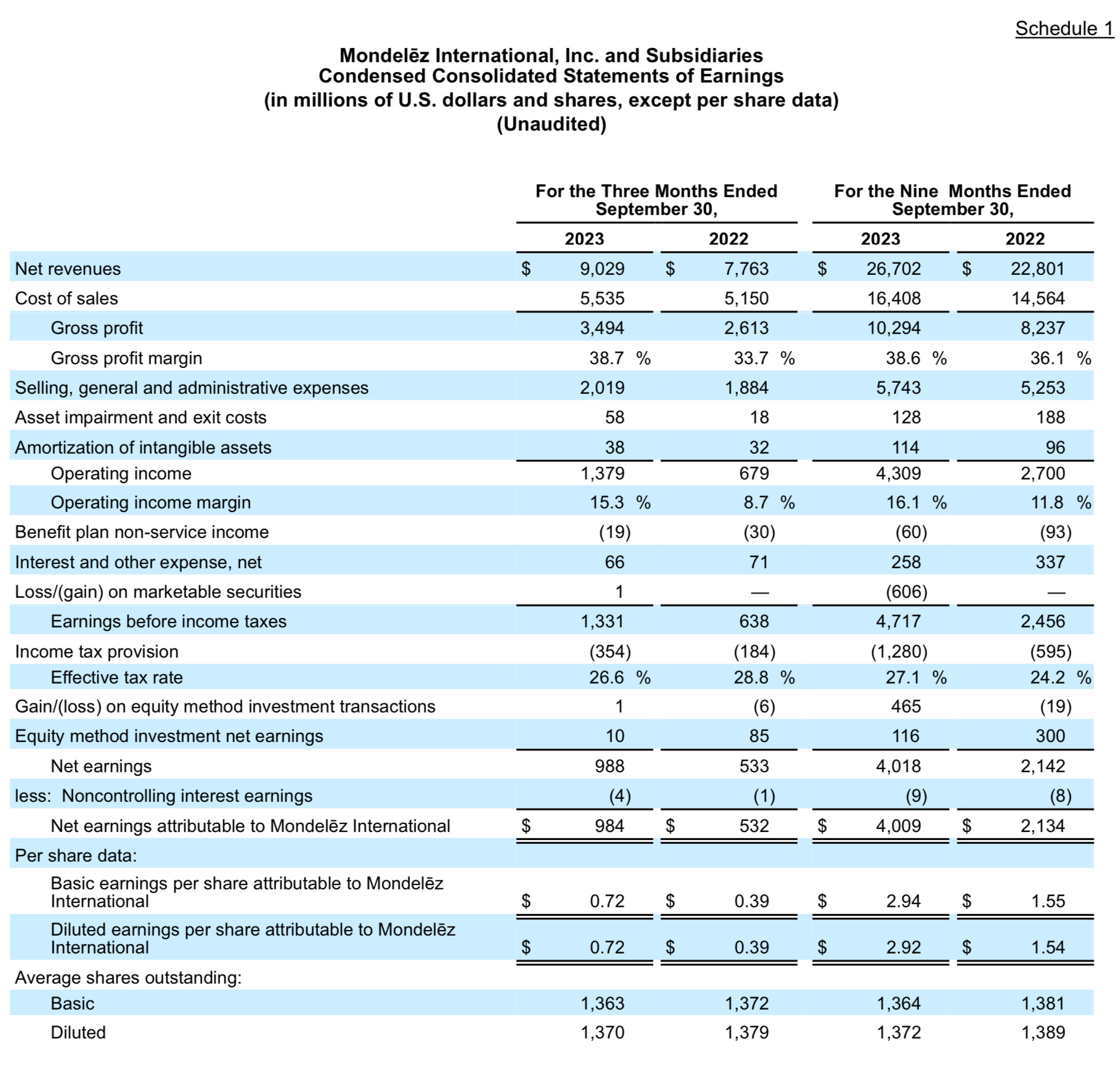

In the first nine months of 2023, Mondelez International MDLZ 0.00%↑ experienced impressive growth in both emerging and developed markets. Net revenues increased by 17.1% to $26.7 billion, while organic net revenue also increased significantly by 17.0% to $26.6 billion. The growth in emerging markets was particularly noteworthy, with a 17.7% rise in net revenues and an even more remarkable 22.5% increase in organic net revenue. Developed markets also performed well, with net revenues and organic net revenues growing by 16.7% and 13.5%, respectively.

The growth was primarily driven by a combination of factors, including organic net revenue growth of 17.0%, contributions from acquisitions, and, to a lesser extent, favorable volume/mix across most regions. It is worth noting that the 2022 acquisitions of Ricolino and Clif Bar contributed a significant $446 million and $529 million, respectively, to the net revenues. However, while there were positive developments, they were partially offset by the impact of a strong U.S. dollar, resulting in unfavorable currency effects and a slight decrease in net revenues due to 2022 divestitures.

On the operational front, operating income increased significantly by 59.6% to $4.3 billion, and adjusted operating income on a constant currency basis rose by 23.6% to $4.6 billion. The company's improvement in net pricing across all regions was driven by carryover pricing from 2022 and new pricing actions in 2023, as well as favorable volume/mix due to strong demand for snack products. However, the company faced increased input costs, primarily from raw materials, which were somewhat mitigated by lower manufacturing costs due to productivity gains.

Unfavorable currency changes, primarily due to the strength of the U.S. dollar, reduced operating income by $183 million. However, the operating income margin increased from 11.8% in the first nine months of 2022 to 16.1% in the same period of 2023. This increase was attributed to various factors, including favorable changes in mark-to-market gains/losses, lower acquisition-related costs, and an improved operating income margin.

Mondelez International's net earnings increased by 87.9% to $4.0 billion. The diluted EPS for the period was $2.92, up 89.6% from the previous year, while the adjusted EPS grew by 13.4% to $2.46. On a constant currency basis, the adjusted EPS increased by 18.9% to $2.58, reflecting the company's strong operational performance and effective management of costs and pricing in a challenging global economic environment.

The financial health of the company is demonstrated by its strong cash flow. Operating activities generated $3.2 billion in cash, while free cash flow increased by $0.5 billion from the previous year to $2.4 billion. Mondelez returned $2.2 billion to its shareholders and successfully divested its developed market gum business for $1.4 billion, which is a shareholder-friendly move.

Looking ahead, Mondelez has positively adjusted its 2023 outlook. The company anticipates an increase in organic net revenue growth from the previously projected 12+ to 14-15%. Additionally, the forecast for adjusted EPS growth on a constant currency basis has been raised to approximately 16%, reflecting a strong year-to-date performance and confidence in the company's market positioning.

Mondelez International's performance in 2023 indicates a company on the rise, driven by strategic acquisitions, efficient operations, and a strong market presence. This demonstrates the company's resilience in a dynamic market and highlights its potential for sustained growth and value creation in the future.

Valuation Update

Based on careful projections and estimations regarding Mondelez International's future trajectory, I have calculated the following fair values for the company's stock:

Current Fair Value: $67

Projected Fair Value in Two Years: $72

When comparing these figures to the current market price of approximately $70, it is clear that Mondelez's stock is reasonably valued. This assessment is based on a comprehensive analysis of the company's potential growth and market dynamics, indicating that the current stock price accurately reflects its intrinsic value.

Conclusion on Mondelez

In conclusion, Mondelez International is a compelling option for long-term investors seeking a fairly valued stock. The company's portfolio is supported by a range of strong and recognizable brands, which not only command significant shelf space but also hold deep resonance with consumers globally. This brand strength underpins Mondelez's robust pricing power, enabling it to navigate varying market conditions effectively.

Mondelez's recent financial performance demonstrates the company's ability to implement strategic pricing actions, indicating a keen understanding of market dynamics and consumer behavior. This pricing power, coupled with a consistent focus on innovation and market adaptation, positions the company well to sustain and potentially enhance its profitability over the long term.

For investors, Mondelez offers a combination of stability and potential growth, supported by its strong brand portfolio and proven market agility. Its fair valuation adds to its appeal, making it a wise choice for portfolios focused on long-term growth and resilience in the face of market volatility.

Adobe

In 2023, Adobe ADBE 0.00%↑ demonstrated impressive financial prowess, reaching new heights in both its fourth-quarter and full-year earnings. In Q4, the company's revenue increased by 13% year-over-year, reaching an unprecedented $5.05 billion. The GAAP earnings per share (EPS) were $3.23, and the non-GAAP EPS were $4.27, representing growths of 28% and 19%, respectively, compared to the previous year.

Adobe's financial achievements for the full year were also remarkable, with a total revenue of $19.41 billion, reflecting steady 13% growth year-over-year. The GAAP EPS and non-GAAP EPS increased by 17% from the previous year, with values of $11.82 and $16.07, respectively. Adobe concluded the year with $17.22 billion in remaining performance obligations (RPO), indicating a strong outlook for the future.

Adobe's success in 2023 can be attributed significantly to its various business segments. The Digital Media segment, with Creative Cloud and Document Cloud at the forefront, was a key driver of growth. In Q4, Creative Cloud's revenue grew by 14% year-over-year, generating $3 billion. Document Cloud also reported a 17% increase, with $721 million in revenue. The Experience Cloud contributed significantly, with $1.27 billion in Q4 revenue, a 12% increase from the previous year.

Adobe's 2023 growth strategy focuses on AI and generative AI technologies. The company integrated these technologies across its Cloud services, released new Adobe Firefly models, and introduced innovations in Photoshop and Adobe Illustrator. This underscores Adobe's commitment to leading the digital creativity and productivity space.

Adobe aims for a total revenue of $21.30 to $21.50 billion in 2024. Adobe expects to generate approximately $1.90 billion in net new Annualized Recurring Revenue (ARR) from Digital Media. The company projects a GAAP EPS of between $13.45 and $13.85, and a non-GAAP EPS ranging from $17.60 to $18.00.

However, a significant shift in Adobe's strategy was the cancellation of the planned acquisition of Figma. This decision was influenced by resistance from EU and UK regulators, highlighting the complexities of navigating global regulatory landscapes in major corporate mergers and acquisitions. Despite this setback, Adobe remains committed to innovation and market leadership. Its ongoing investments in AI and generative AI, along with a robust financial foundation, position the company well for sustained growth and leadership in the creative software industry.

In conclusion, Adobe's 2023 performance demonstrates the company's ability to thrive in the present while navigating the challenges and opportunities of a dynamic global market. The company's strong financials, commitment to cutting-edge technology, and strategic agility make it a formidable player in the digital media and creative software sectors.

Valuation Update

The current and projected fair values for the stock are as follows:

Current Fair Value: $350

Fair Value in Two Years: $400

Based on these estimations, a stock price above $600 indicates that the stock is overvalued.

Conclusion on Adobe

In conclusion, Adobe presents a compelling investment case for long-term investors. This is underscored by its robust market position, significant potential in AI, and the unexpected benefit of the cancelled Figma acquisition.

Adobe's enduring market position is evident from its consistent financial performance, notably in 2023, when it achieved record revenues and earnings growth. The substantial increase in Adobe's Annualized Recurring Revenue (ARR) and healthy forward-looking RPO indicate a strong business foundation. Adobe's market leadership in creative and productivity software is a testament to its past successes and potential for future growth.

The company's commitment to AI and generative AI is particularly noteworthy. As technology continues to evolve and become more integral to various industries, Adobe's early and focused investments position it at the forefront of this transformation. The integration of AI across its product suite, notably in Creative Cloud and Document Cloud, not only enhances its existing offerings but also opens avenues for new, innovative products. This technological edge could be a key driver of Adobe's long-term growth and market dominance.

The cancelled acquisition of Figma, initially perceived as a setback, may actually benefit investors. This decision has freed up significant capital and resources, which Adobe can now allocate to other strategic initiatives, such as further AI development, organic growth opportunities, or even other acquisitions that face fewer regulatory hurdles. The decision also mitigates the risk of integrating a large acquisition and navigating potential regulatory challenges in different jurisdictions. For investors, this suggests a more concentrated and potentially less hazardous path to growth.

In general, Adobe's robust market position, strategic emphasis on AI and technological innovation, and the unforeseen advantages resulting from the terminated Figma acquisition, present a promising outlook for long-term investors. The company's potential for growth and stock performance in the long run depends on its ability to adapt to market changes, financial robustness, and commitment to innovation. However, the current stock valuation appears to be significantly overvalued.

PUMA

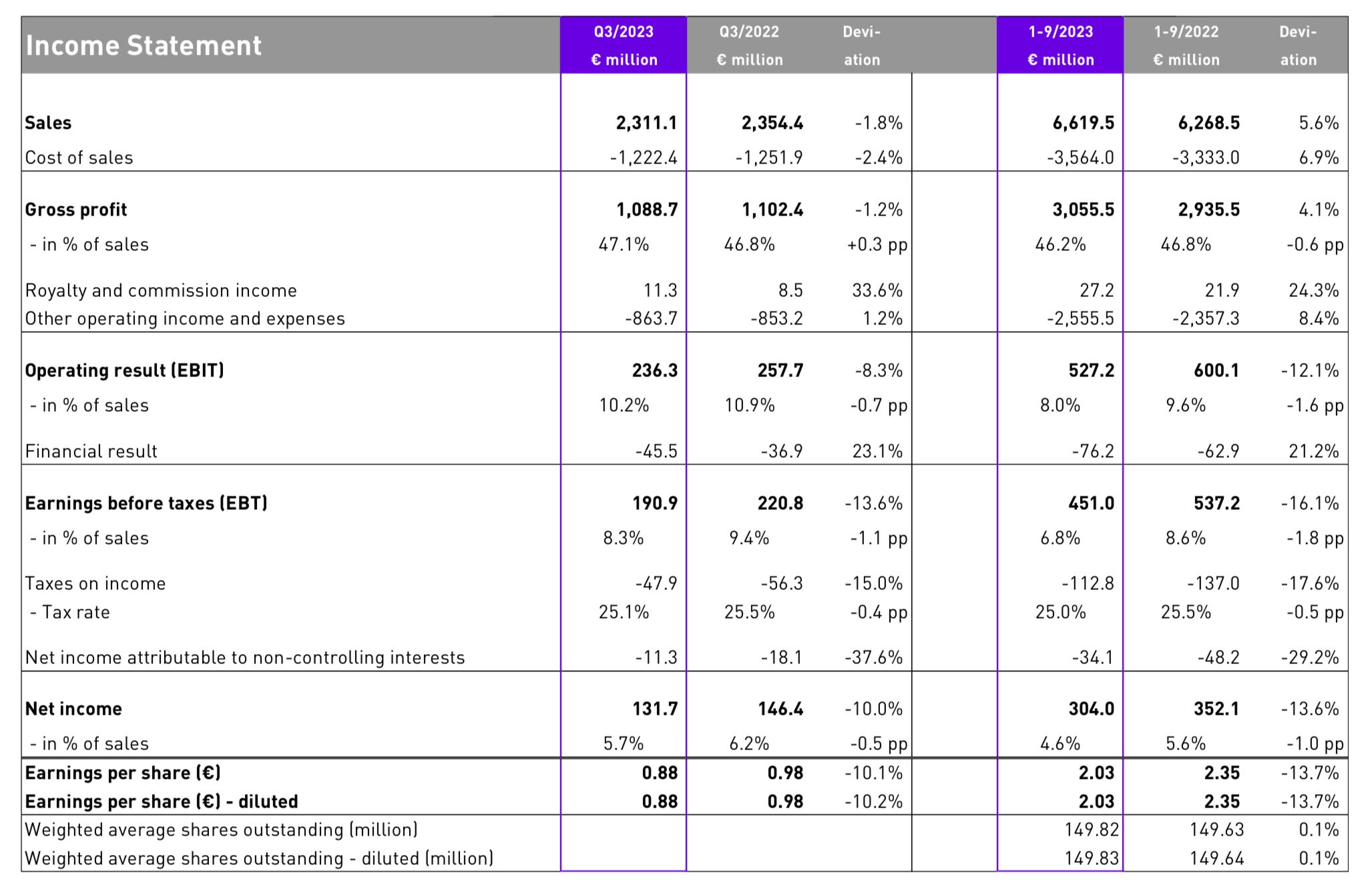

In the first nine months of 2023, PUMA, the German sports brand, experienced a significant 10.3% increase in sales, reaching €6,619.5 million. The growth was primarily driven by the EMEA and Asia/Pacific regions. Sales in the Americas experienced a slight decline due to macroeconomic challenges and PUMA's reliance on the off-price Wholesale business in the U.S. However, the Wholesale segment grew by 7.3% to €5,113.7 million. Additionally, Direct-to-Consumer (DTC) sales surged by 22.0% to €1,505.8 million, driven by strong performance in both retail stores and e-commerce.

Footwear was the leading product category with a growth of 19.0%, while Apparel and Accessories experienced only modest increases. Despite these gains, PUMA's gross profit margin slightly decreased to 46.2% due to adverse currency effects, industry-wide promotions, and increased sourcing and freight costs. However, strategic price adjustments and an advantageous mix of geographical and distribution channels partially offset these negative impacts.

Operating expenses increased to €2,555.5 million, an 8.4% rise, due to higher distribution costs, growth in the DTC channel, and intensified marketing investments. As a result, the operating result (EBIT) decreased by 12.1% to €527.2 million, leading to a reduction in net income to €304.0 million.

PUMA's working capital increased substantially, which was attributed to reduced inventories and higher trade receivables. The outlook for 2023 is cautiously optimistic despite geopolitical and macroeconomic uncertainties. PUMA confirms its expectation of high single-digit sales growth and an unchanged operating result (EBIT) for the year. The focus is on overcoming short-term challenges while maintaining long-term brand momentum.

Valuation Update

Current Fair Value: €54

Projected Fair Value in Two Years: €61

As the stock trades at €54, PUMA seems to be fairly valued.

Conclusion on PUMA

In conclusion, PUMA's stock currently presents a scenario of tempered expectations. The company has demonstrated resilience and adaptability in a challenging market, but is signaling weaker growth in the upcoming quarters compared to its previous performances. This deceleration can be attributed to a combination of factors, including macroeconomic headwinds, geopolitical uncertainties, and intense competition in the sportswear industry.

PUMA's stock seems to be fairly valued at present, reflecting a balanced view of the company's strong brand presence and operational agility, despite potential market volatility and constrained consumer spending. It is important to note that PUMA is operating in a highly competitive landscape, competing against industry giants with substantial market share and brand influence. PUMA's market position and financial performance may face additional strain due to competitive pressure and external economic factors.

Although PUMA has made commendable efforts to drive growth through its Direct-to-Consumer channels and product innovation, particularly in footwear, the broader industry challenges and slow pace of growth suggest that investors should take a cautious approach. The company's strategic focus on long-term brand momentum and market share gains, despite short-term profitability concerns, suggests a commitment that could lead to positive results in the future. However, the stock may face pressure in the near term as the company navigates complex market dynamics.

Investors should monitor PUMA's strategic initiatives and market conditions objectively, balancing the potential for growth against the risks inherent in a competitive and uncertain global economic environment.

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is invested in Adobe.