#93 American Express - A Stock Analysis

The Kind of Company You’d Be Happy to Hold Forever

American Express

American Express is one of those rare businesses that seem to get better with time. I’ve been personally invested in this company for years, and it remains one of the few stocks I’ve never felt the urge to sell. It’s a brand built on trust, loyalty, and premium customer relationships — the kind of qualities that don’t show up in quarterly reports, but matter enormously over decades.

Warren Buffett famously opened his position in Amex during the so-called “salad oil scandal” of the 1960s, when a confidence crisis temporarily shook the company’s stock price. What he saw then still holds true today: a resilient franchise with an enduring moat, strong customer economics, and management that plays the long game.

In this post, I break down the current state of American Express for long-term investors — its financials, business model, competitive position, and what the next few years could look like.

Overview and Brief History

American Express (NYSE: AXP) AXP 0.00%↑ is a global financial services company best known for its credit and charge cards. Founded in 1850 as an express mail business, it reinvented itself over the decades into a premium payments and lifestyle brand. Amex introduced its first charge card in 1958 and later launched iconic products like the Gold Card (1966), Green Card (1969), Platinum Card (1984), and ultra-exclusive Centurion “Black” Card (1999). The company built a reputation for “trust, security, and service,”encapsulated by its famous slogan “Don’t Leave Home Without It.”

Today, American Express operates a “closed-loop” network – it issues cards, processes transactions, and lends to cardmembers, unlike networks like Visa or Mastercard that only handle processing. This integrated model, focused on high-spending, creditworthy customers, has made Amex’s brand a symbol of premium status in payments. It is the fourth-largest card network globally by purchase volume (after UnionPay, Visa, and Mastercard) with 141 million cards in force and over $1.7 trillion in annual cardmember purchase volume. Despite its global reach (accepted in over 200 countries), Amex maintains a selective prestige – it’s accepted at 99% of U.S. merchants that take credit cards, but still faces more limited acceptance overseas in some markets. Overall, American Express’s long history and strong brand equity provide a solid foundation for its business.

Latest Financial Results Highlights

American Express recently delivered strong financial results. In the first quarter of 2025, revenue (net of interest expense) was $17.0 billion, up 7% year-over-year (8% on a currency-adjusted basis). This top-line growth was driven by higher net interest income (as cardmember loans grew), increased cardmember spending, and continued growth in card fee revenue. Net income for Q1 2025 was $2.6 billion, up 6% from the prior year, and diluted EPS came in at $3.64 (vs. $3.33 a year ago, a 9% increase). Notably, cardmember spending rose 6% (7% adjusted for an extra day in the prior leap year) reflecting solid demand, especially in travel and entertainment categories. Credit metrics remain healthy – net write-off rates were stable at 2.1%, and provisions for credit losses actually ticked down vs. last year due to some reserve releases.

On the cost side, expenses rose about 10% as Amex spent more on customer engagement (e.g. rewards and travel benefits usage increased) and continued to invest in marketing and new card acquisitions. Management reaffirmed its full-year 2025 guidance of 8–10% revenue growth and EPS of $15.00–$15.50, signaling confidence in the momentum of the business. These latest results extend Amex’s strong 2024 performance: last year, revenues hit a record $65.9 billion (up 9%) and EPS grew 25% to $14.01. In short, American Express is entering 2025 with solid growth, strong credit quality, and continued premium customer demand, despite a moderating economic backdrop.

Business Model and Revenue Streams

American Express operates a unique business model that combines aspects of a bank, a card issuer, and a payment network. Its revenue comes from a diverse set of streams:

Discount Revenue (Merchant Fees): This is Amex’s largest revenue source, representing the fees charged to merchants for processing Amex card transactions. Unlike Visa or Mastercard (who pass interchange fees to issuing banks), Amex both issues the card and runs the network, so it earns and retains the merchant discount fee minus any partner payouts. For 2024, Amex’s discount revenue was $35.2 billion, about 53% of total revenue. The merchant discount rate (fees as a % of transaction) is higher for Amex (roughly ~2.3%), reflecting its premium customer base, though competitive and regulatory pressures have gradually narrowed the gap in some markets.

Net Card Fees: These are the annual membership fees cardmembers pay on charge and credit cards. Amex has a large portfolio of fee-based products (from the $250/year Gold Card to the $695 Platinum Card, etc.), and customers pay for the generous rewards and perks. Net card fee revenue has been growing at a double-digit clip for years; in 2024 it reached $8.45 billion (16% growth) – a record high, reflecting strong new card acquisitions and high retention of existing members.

Net Interest Income: As a bank holding company, American Express earns interest on balances that customers finance. Many Amex customers carry revolving credit card loans or use Amex’s small business loans. In 2024, net interest income was about $15.5 billion (18% higher than 2023). Rising loan balances (especially on revolving credit cards) combined with higher interest rates have boosted this segment. Net interest income now contributes roughly 23% of total revenue. However, unlike pure credit card issuers, Amex’s spend-centric model means a significant portion of customers pay in full, keeping its loan portfolio growth moderate.

Service Fees and Other: Amex earns various fees for services such as foreign currency conversion, travel bookings, network processing fees, and other card-related charges. In 2024, service fees and other revenue were about $5.13 billion. This can include things like late fees, commissions from travel & lifestyle services, partnership revenues, etc. Amex also partners with other institutions for co-branded cards (Delta, Marriott, etc.), which can bring in “business development” payments or joint marketing funds, though these may be netted against expenses rather than shown as gross revenue.

Amex serves several customer segments: consumer cardmembers, ranging from mass affluent individuals to high-net-worth clients (the Platinum and Centurion clientele); small and mid-sized businesses, who use Amex for purchasing and lending products; and large corporate clients for T&E expense cards and corporate purchasing solutions. It reports segments like U.S. Consumer, International Card, and Global Commercial Services, but the common thread is a focus on relatively affluent, creditworthy customers across both consumer and business spheres. This focus is evident in its approval standards – “it’s much harder to get an American Express card than a Visa/Mastercard” because Amex underwrites the credit risk and prioritizes customers with strong credit. The payoff is a customer base that, on average, spends more per card (over $24k annually) and has lower default rates than industry averages.

From a competitive positioning standpoint, American Express sits in an interesting middle ground. It competes with card networks like Visa and Mastercard for payment volume, but also with banks/issuers like JPMorgan Chase, Citigroup, or Discover who issue cards and lend to consumers. Amex’s “closed-loop” model is a key differentiator – it directly manages the relationship with both the card member and the merchant. This allows Amex to capture more value per transaction (via merchant fees and interest spread) and use data insights across the spend spectrum to tailor rewards and offers.

The model, however, has limits: to keep merchants on board, Amex can’t set fees too high without risking acceptance, and to grow volume, it has had to broaden access (e.g. Amex has worked to increase merchant acceptance globally and even allows third-party banks to issue Amex cards in some regions). Overall, Amex’s business model is often described as a “spend-centric” franchise – it makes money when its cardmembers spend freely and pay annual fees, and secondarily when they borrow. This contrasts with a “lend-centric” model (like many bank issuers) that rely heavily on interest and fees from revolving debt. Amex’s model produces a mix of fee, merchant, and interest income that tends to do best when the economy (especially consumer spending on travel and services) is strong.

Strengths of American Express

American Express enjoys several competitive strengths that underpin its investment appeal:

Powerful Brand and Premium Image: Amex’s brand is synonymous with premium service and trust. It consistently ranks among the most valuable global brands. Cardmembers often display strong loyalty – carrying an Amex, especially a Platinum or Centurion card, is viewed as a status symbol. This brand prestige allows Amex to charge higher fees (both to cardholders and merchants) than competitors in many cases.

High-Spending, Loyal Customer Base: Amex cardmembers tend to spend significantly more on their cards than users of other networks. In 2023, the average Amex cardmember spent ~$24,000 annually – a testament to the affluent and business users Amex attracts. The company has been successful in growing among Millennial and Gen Z customers lately (the fastest-growing cohorts, with 16%+ spend growth), indicating the brand’s relevance to younger professionals. Importantly, Amex boasts high customer retention – once customers join (often lured by big sign-up bonuses and perks), they tend to stay and renew their cards.

Multiple Revenue Levers & Pricing Power: With its mix of revenue streams (merchant fees, card fees, interest), Amex isn’t overly reliant on just one source. It has shown pricing power in growing card fee revenue – e.g. raising annual fees or introducing premium tiers (and adding value to justify it). Net card fees have grown at a double-digit rate for 26 consecutive quarters as of 2024, reflecting Amex’s ability to get customers to pay for its rewards and services. Similarly, on the merchant side, while Amex has slightly lowered fees to expand acceptance, it still commands a premium in many cases because merchants value access to Amex’s high-spending customers.

Global Reach and Network Expansion: Amex has a presence in over 200 countries and territories, and it continues to expand its merchant network. In 2024 alone, Amex added millions of new merchant locations globally, narrowing the acceptance gap. Its Global Network Services partnerships allow foreign banks to issue Amex-branded cards, extending Amex’s reach without bearing all the risk. As international markets grow wealthier and travel resumes, Amex’s global footprint positions it to capture that upside.

Resilient Credit Performance: Despite catering to borrowers via charge and credit cards, Amex historically maintains industry-low delinquency and loss rates. For example, in mid-2023, only 1.2% of its card loans were 30+ days past due, better than pre-pandemic levels (~1.5%). Its focus on prime credit customers and effective risk management (backed by decades of data on its closed-loop network) gives it an edge in credit quality. This strength was evident during the pandemic downturn, when losses remained manageable and Amex could quickly return to profitability.

Shareholder-Friendly Capital Return: Amex has a long track record of returning capital to shareholders through dividends and share buybacks (more on this below). This discipline has boosted its EPS growth and signals confidence from management in the company’s long-term prospects.

Weaknesses and Risks

Despite its strengths, American Express faces a number of risks and potential weaknesses that investors should consider:

Cyclical Exposure – As a payments and lending company, Amex’s fortunes are tied to consumer and business spending cycles. In an economic downturn or if consumer spending shifts, Amex’s transaction volumes can drop sharply. For instance, during the 2020 pandemic shock, Amex’s revenue fell 17% and EPS plunged over 50% as travel and entertainment spending dried up. A future recession or even a mild slowdown in discretionary spending (especially in travel) could hurt Amex’s growth and credit metrics.

Competition (Networks and Issuers) – Amex is squeezed between major global networks (Visa, Mastercard) and large card-issuing banks. On one side, Visa and Mastercard have ubiquitous acceptance and partner with every bank, giving them scale advantages. Banks like JPMorgan Chase and Citi aggressively court the same affluent customers with rich rewards (e.g. Chase Sapphire Reserve card famously challenged Amex Platinum a few years ago). Co-branded relationships are a battleground: Amex won back the Amazon Business card recently and retained its Delta Airlines partnership through 2029 at a high cost, but it infamously lost the Costco co-brand deal in 2016, which hurt for several years. The risk is that competitors could lure away key partners or customer segments, eroding Amex’s market share.

Merchant Acceptance and Fees – While Amex has expanded acceptance, it still faces acceptance gaps internationally and among smaller merchants who dislike its higher fees. Regulatory actions can exacerbate this – e.g. the EU imposed interchange fee caps that effectively forced Amex to lower some fees to avoid being non-competitive. In the U.S., proposed legislation (like the Credit Card Competition Act) could pressure fees or require network choice that might weaken Amex’s integrated model. If merchant discount revenue is squeezed by regulation or competition, it would directly hit Amex’s largest income source.

Interest Rate and Credit Risk – As a lender, Amex benefits from higher interest rates (improving net interest margin on loans), but only up to a point. If rates rise too high or economic conditions worsen, credit losses can mount and consumers might borrow less or struggle to repay. Amex is somewhat sensitive to interest rate cycles – it funds a lot of its lending via deposits and debt, so higher rates increase its interest expense on funding as well. A rapid change in the rate environment can impact Amex’s net interest yield and credit provisioning needs.

High Dependence on T&E and Premium Segments – A large portion of Amex’s spending volume historically comes from Travel & Entertainment (T&E) and corporate travel (though they’ve diversified more into everyday spend). This was a boon during the post-pandemic travel rebound, but it also means concentration risk. If business travel structurally declines or another shock hits travel, Amex could be more affected relative to competitors with more everyday retail spend. Moreover, Amex’s focus on premium, high-income customers means it isn’t tapping the mass market as much – if wealth inequality or spending patterns shift, Amex could see growth limitations in saturating the ultra-affluent space.

Valuation and Expectations – (Discussed more below in Valuation) Amex’s stock in recent times has reflected a lot of optimism. As of early 2025 it traded at a higher-than-usual multiple of earnings. If the company ever stumbles on growth or the market’s risk appetite changes, valuation could compress, posing risk to shareholders. In short, Amex must continue executing well to justify its premium valuation – any disappointment (e.g. slower card acquisitions, higher losses) could hurt the stock disproportionately.

Technological Disruption – Fintech payment innovations like mobile wallets, “buy now pay later” (BNPL) services, or real-time payments present a long-term risk. Amex has been adapting (e.g. integrating with Apple Pay, launching its own installment payment options), but the payments landscape is evolving. If younger consumers bypass traditional credit cards for alternative payment methods, Amex will need to stay ahead to remain relevant. Likewise, cybersecurity is a risk for any financial firm – a major data breach or tech failure could damage Amex’s trusted reputation.

In summary, American Express’s weaknesses largely stem from the flip side of its strengths: its premium model leaves it exposed to economic swings and competitive attacks. Investors should monitor these risks, though Amex’s history suggests it often navigates challenges and adapts (for example, it rebounded strongly after the 2008 financial crisis and after losing Costco by doubling down on other areas).

Dividend Policy and Share Buybacks

American Express has been a consistent capital return story, using both dividends and share repurchases to reward shareholders. However, its approach tilts more toward buybacks, with a relatively modest dividend yield.

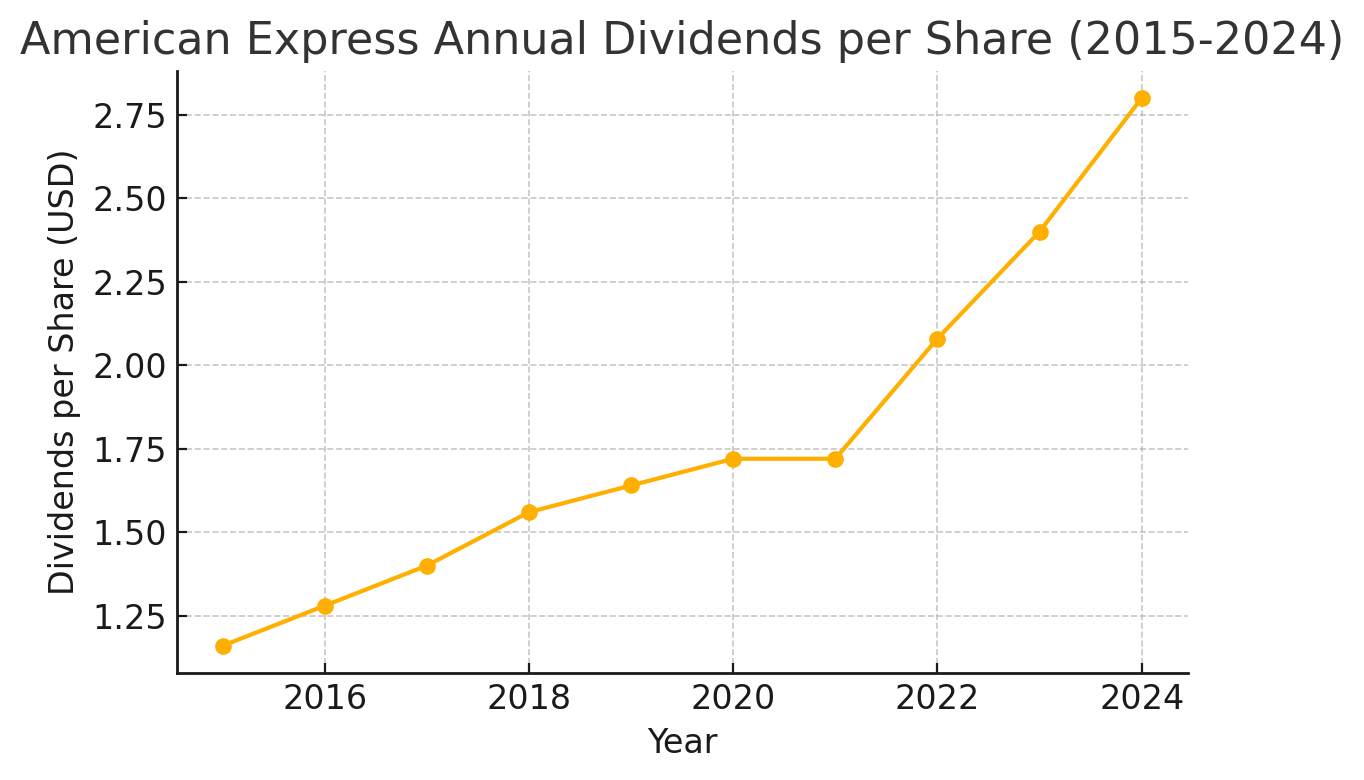

Dividend History: Amex pays a quarterly dividend that has grown substantially in recent years (with a pause during the pandemic). As of 2024, the quarterly dividend was $0.70 per share (recently increased to $0.82 for 2025, a 17% hike). This translated to $2.80 per share in annual dividends in 2024, up from $2.40 in 2023 and $2.08 in 2022. The chart below shows Amex’s dividend growth over the past decade, highlighting a sharp acceleration post-2021 after a brief freeze:

Amex’s current dividend yield is around ~1.1–1.3% (varying with stock price) – not high by market standards, but the dividend increases have been robust (e.g. +15% in 2023, +17% in 2024). During the early COVID period, Amex paused dividend raises (keeping it at $1.72 annually in 2020 and 2021) to conserve capital, but resumed growth in 2022 once conditions improved. The payout ratio remains fairly low (under 20% of earnings), leaving ample room for further increases. Management’s recent move to boost the dividend by 17% for 2025, and commentary about returning excess capital, signals a continued commitment to growing the payout.

Share Buybacks: Share repurchases have been a major component of Amex’s capital strategy. The company has steadily reduced its outstanding share count over time, which boosts EPS and signals confidence in the business. In 2024, Amex repurchased 24 million shares for $5.9 billion (at an average price of ~$242 each). In 2023, it bought back 22 million shares for $3.5 billion, and in 2022 about 20 million shares for $3.3 billion. The buyback pace accelerated significantly in 2021 after the pandemic shock – that year Amex repurchased 46 million shares for $7.6 billion (taking advantage of a relatively low stock price at the time). By contrast, in 2020, repurchases were minimal (~7 million shares, $0.9B) as buybacks were suspended amid the crisis. Over the long run, these buybacks have compounded: Amex had over 800 million shares in 2018, but only ~702 million by the end of 2024 – a 12% reduction in share count in just the past three years. The following chart illustrates the decline in Amex’s shares outstanding:

This share reduction amplifies growth on a per-share basis – for example, even if net income grows moderately, EPS can grow faster due to fewer shares. In 2024 alone, Amex returned a total of $7.9 billion to shareholders via buybacks and dividends, equal to ~76% of the capital it generated that year. The company has indicated it will continue returning excess capital and is willing to adjust the pace of repurchases based on market conditions and its capital needs.

Investors should note that while buybacks can significantly boost shareholder value, they are effective only if done at reasonable valuations and sustained long-term – Amex appears to have managed this well historically, opportunistically slowing or speeding up repurchases as appropriate (e.g., slowing in downturns and resuming aggressively in recoveries).

In summary, American Express’s capital return policy has made it an attractive stock for long-term holders. One gets a growing (if not high) dividend for income and steady buybacks that enhance ownership stake over time. This balanced approach has contributed to double-digit EPS growth in recent years and is a key part of the long-term investment thesis.

The sections on Valuation, Bull vs. Bear Case, Outlook, and Conclusion are exclusively available to paid subscribers.

Keep reading with a 7-day free trial

Subscribe to Kroker Equity Research to keep reading this post and get 7 days of free access to the full post archives.