#18 Stock Watchlist - 3/2024

#18 Stock Watchlist - 3/2024

Updating fair value estimates during earnings season

Dear readers,

thank you for being here and for your interest in my work! If you like this article, if you find this stock watchlist and my deep dives valuable, and if you want to support my work, please feel free to subscribe!

Please read the disclaimer at the end of this article. This is not investment advice!

Welcome to my third Stock Watchlist update in 2024. It's that time of year when many companies are releasing their earnings reports and annual reports, making it the perfect opportunity to review them and update my fair value estimations. In this update, I've adjusted the fair values for Netflix, Apple, Visa, Mastercard, Costco, and Marsh & McLennan.

Stay tuned for more updates, as I'll soon be publishing additional deep dives into several intriguing companies. My next feature will focus on H&M Group, the popular fashion company from Sweden.

Updated Stock valuations:

Netflix NFLX 0.00%↑

Apple AAPL 0.00%↑

VISA V 0.00%↑

Mastercard MA 0.00%↑

Costco COST 0.00%↑

Marsh McLennan MMC 0.00%↑

Some comments on the updated Stocks

Netflix

I recently published my detailed post on Netflix, so I will not write much here, but just link to my post. Hope you like it!

Apple

Apple is a well-known stock and company, so I believe an in-depth discussion of its business model is unnecessary. Most people are familiar with its most successful products, the services it offers, and the large installed base which serves as a foundation for expanding new services and enhancing existing ones. However, there is a lot of uncertainty surrounding Apple's new innovations. The Vision Pro, Apple's latest product, represents a completely new venture, and while I can imagine it achieving success, I'm not convinced that it will be adopted for daily use by the mass market in the same way as the iPhone or Apple Watch. Moreover, Apple is notoriously tight-lipped about new product innovations, which doesn't make predicting its future potential any easier. Despite this, based on what we do know, I feel confident we can derive a fair value range for the stock. I would like to share my thoughts on the valuation of the stock.

First and foremost, I believe the stock is currently overvalued. My valuation is based on a DCF (Discounted Cash Flow) analysis and the EV/EBIT metric, which is my preferred multiplier. Currently, my calculations assume that Apple will grow its top line in the mid-single digits, while EBIT and Free Cash Flow will grow at a similar rate. Due to share buybacks, the number of shares will decrease, meaning every per-share metric will increase slightly more. Based on this, I estimate a fair value range of between $135 and $145 per share, with a midpoint of about $140 per share. Compared to its current price of $185 per share, the stock appears to be significantly overvalued. Don't misunderstand me; Apple may be the best company in the world, or at least one of the best, with brand strength and an enormous base of loyal customers and devices worldwide acting as a strong moat. However, there is a fair price for every company, based on free cash flow generation, growth assumptions, and risk, and at the moment, I see a mismatch between fair value and trading price.

Mastercard and VISA

I believe Mastercard and Visa are among the best companies in the world, each boasting a unique business model that creates a nearly indestructible moat. I use "nearly" cautiously because it's imprudent to claim anything is completely indestructible; unforeseen events can happen.

When it comes to valuation, I think both are overvalued, but therein lies the dilemma: these companies often appear overvalued. So, the question of whether they are truly overvalued becomes somewhat philosophical. According to my understanding of valuation, they are indeed overvalued, despite the market consistently pricing them high. Mastercard is considered more overvalued than Visa, attributed to differing expectations for future growth. Mastercard is expected to grow slightly more robustly than Visa, leading the market to value it relatively higher. Interestingly, Visa seems to be nearing a point where it could be considered fairly valued for the midterm, at least according to my watchlist projection for the next two years, assuming my assumptions hold true. So, for my baseline scenario, Visa has a fair value of about $249, and Mastercard has a fair value of about $385.

Costco

I've never been to a Costco, only seen it through videos and pictures and from reading their annual reports. Yet, it seems to be quite impressive and has even become something of a cultural institution. Costco's unique focus on customers and its management approach have proven successful. Because of this, I'm quite fond of the company and its stock. However, I believe that Costco's stock is significantly overvalued at the moment. When looking at the EV/EBIT for the next twelve months (NTM), it is trading at 33.47x, the highest valuation ever. Additionally, EBIT is expected to grow at a CAGR of about 3% for the next 3 to 4 years. My calculated fair value is about $456, compared to a current stock price of $709.

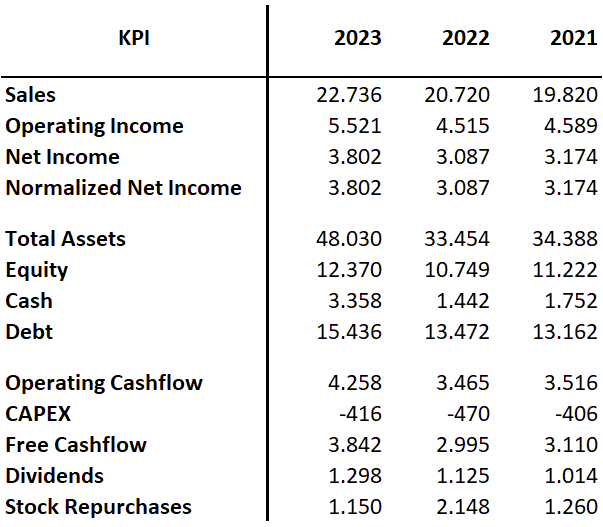

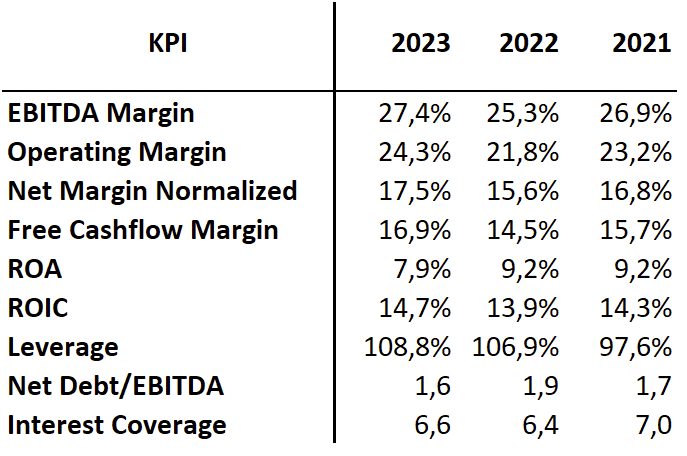

Marsh McLennan

I am not sure how popular Marsh & McLennan is with most investors, so I would like to introduce the company to you.Marsh & McLennan Companies, Inc. is a global professional services firm that offers expertise in risk, strategy, and human capital. It operates through two main segments: Risk and Insurance Services, and Consulting. The Risk and Insurance Services segment delivers comprehensive risk management solutions, including risk advice, risk transfer, risk control, insurance and reinsurance brokerage, strategic advisory, and analytics. It caters to a diverse clientele including businesses, public entities, insurance companies, professional organizations, and private individuals. The Consulting segment, on the other hand, provides a range of services in health, wealth, and career consulting, alongside specialized management, strategic, economic, and brand consulting services. Founded in 1871, Marsh & McLennan is headquartered in New York, New York, emphasizing its long-standing presence and expertise in the industry.

Marsh & McLennan possesses several unique characteristics that contribute to its competitive moat. Key factors that contribute to MMC's moat are Diverse Service Offerings, a Global Presence, a Deep Industry Expertise and Strong Client Relationships. The company is very profitable and growing at a commendable pace. Below are some key figures to note.

Marsh & McLennan is a high-quality company and stock, highly valued by the market. However, from my perspective, it's valued too highly, making the stock overvalued with its current price at $193. My estimated fair value is around $148.

That's all for now. Thank you for reading and showing interest in my posts! Feel free to subscribe to my publication.

Although I didn't calculate a fair value for Spotify, I wanted to share my post here again, just in case you missed it :-).

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is invested in Apple, VISA, Mastercard, Costco.