Dear readers,

thank you for being here and for your interest in my work! If you like this article and if you want to support my work, please feel free to subscribe and like! Please read the disclaimer at the end of this article. This is not an investment advice!

The last time I took an in-depth look at Alphabet was in September 2023, almost a year ago. It's time to update my assessment of the stock's value and take a look at the performance of this outstanding company.

About Alphabet

Almost everyone reading this will be familiar with the company and its business. Just a very brief description:

Alphabet Inc. offers a wide range of products and platforms across the world. Incorporated in 1998, Alphabet Inc. is headquartered in Mountain View, California. The company operates through three main segments: Google Services, Google Cloud, and Other Bets.

The Google Services segment encompasses products and services such as ads, Android, Chrome, devices, Gmail, Google Drive, Google Maps, Google Photos, Google Play, Search, and YouTube.

The Google Cloud segment provides infrastructure, cybersecurity, databases, analytics, AI, and other services, including Google Workspace, which offers cloud-based communication and collaboration tools for enterprises such as Gmail, Docs, Drive, Calendar, and Meet. The Other Bets segment focuses on healthcare-related and internet services.

To highlight Google's and Alphabet's enormous reach, I want to refer to this quote from the latest earnings call:

“We have six products with more than two billion monthly users, including three billion Android devices. Fifteen products have half a billion users. And we operate across 100-plus countries.”

From a financial standpoint, Alphabet is not just a giant but also incredibly profitable, debt-free, and still growing at a respectable pace.

Reviewing the growth figures for the last four quarters on TIKR, I am very pleased with the development. Revenue, gross profit, and operating income have increased significantly. As operating income has grown faster than revenues, profitability has logically improved. This will be evident in the next graph, which shows significant improvements in both EBIT margin and net income margin.

Additionally, the return on invested capital (ROIC) for Q1 2024 ticked up to an impressive 29%.

Alphabet's free cash flow generation is remarkable, but what truly stands out is the increased capital expenditure, primarily due to investments in their infrastructure for AI applications.

In the following steps, I aim to delve into specific topics that stand out to me and are crucial for making an informed investment decision at this moment.

Cloud business is finally profitable

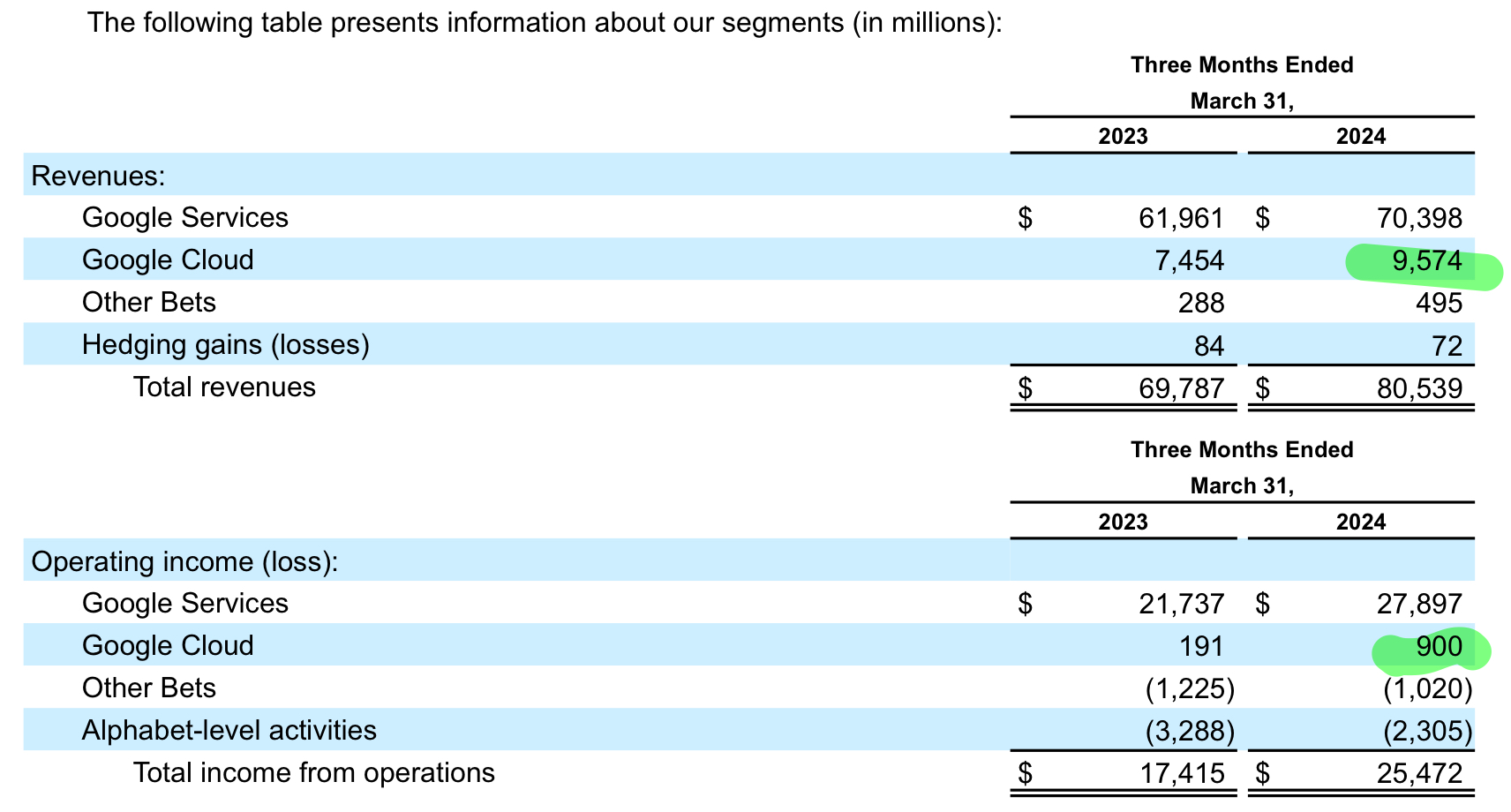

The operating income of Google's Cloud segment has undergone notable changes in recent years. In 2021, Google Cloud reported an operating loss of $3.1 billion, which slightly improved to a loss of $1.9 billion in 2022. The most significant development occurred in 2023, when Google Cloud turned profitable, achieving an operating income of $1.7 billion. This transition from a loss of $1.9 billion in 2022 to a positive operating income of $1.7 billion in 2023 marks an impressive $3.6 billion improvement. The increase in operating income was primarily driven by higher revenues and cost reductions due to changes in the estimated useful lives of servers and network equipment, partially offset by increased compensation expenses due to headcount growth. In Q1 2024, Google Cloud continued its profitable trajectory, achieving an operating income of $900 million USD.

“But in addition, we expect YouTube overall and Cloud to exit 2024 at a combined annual run rate of over $100 billion.”

Google Cloud is expected to grow significantly in the upcoming years. In the Q1 earnings call the management outlined that it expects for 2024 a significant growth for it and YouTube.

Useful lives estimation changes

Alphabet Inc. has periodically reassessed the useful lives of its servers and network equipment, leading to changes that significantly impacted depreciation expenses. In January 2021, the estimated useful life of servers was extended from three to four years, and certain network equipment from three to five years, reducing depreciation expense by $2.6 billion and increasing net income by $2.0 billion that year.

Further revisions in January 2023 adjusted the useful life of servers to six years and extended certain network equipment to six years as well. Effective from the beginning of fiscal year 2023, these changes are projected to reduce depreciation expense by approximately $3.4 billion for the full year 2023 for assets in service as of December 31, 2022.

I am uncertain whether the Cloud business would be that profitable like today without these changes and the resulting reduction in depreciation charges.

YouTube

YouTube has emerged as the hidden gem of Alphabet, capturing nearly 10% of screen time in the US. This achievement is absolutely stunning. YouTube has experienced significant development in recent years. In 2023, YouTube's ad revenues increased by $2.3 billion compared to the previous year, reaching $31.5 billion.

Regarding subscriptions, which are becoming increasingly vital for YouTube, the management announced that in Q1, YouTube surpassed 100 million Music and Premium subscribers globally, including those on trial. Additionally, YouTube TV now boasts over eight million paid subscribers.

YouTube will continue to play an important role in the future.

Stock repurchases and Stock based compensation

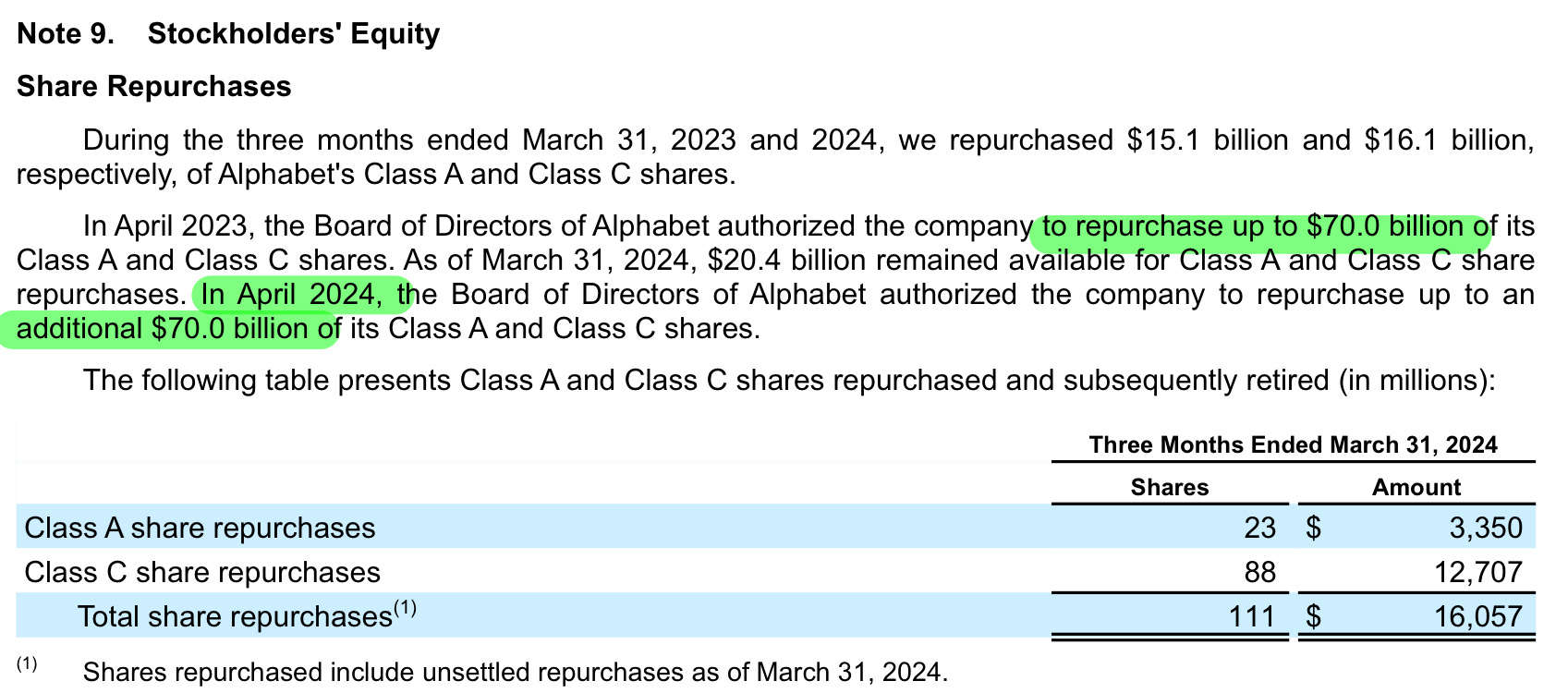

Alphabet Inc. has been actively repurchasing its Class A and Class C shares over the past few years. In the last three years the company repurchased $171.8 billion worth of shares.

In April 2023, the Board of Directors authorized an additional $70.0 billion for share repurchases, with $36.3 billion remaining available for repurchases as of December 31, 2023. Despite these substantial buybacks, a significant portion of these repurchases serves primarily to offset the dilution caused by the company's share-based compensation programs.

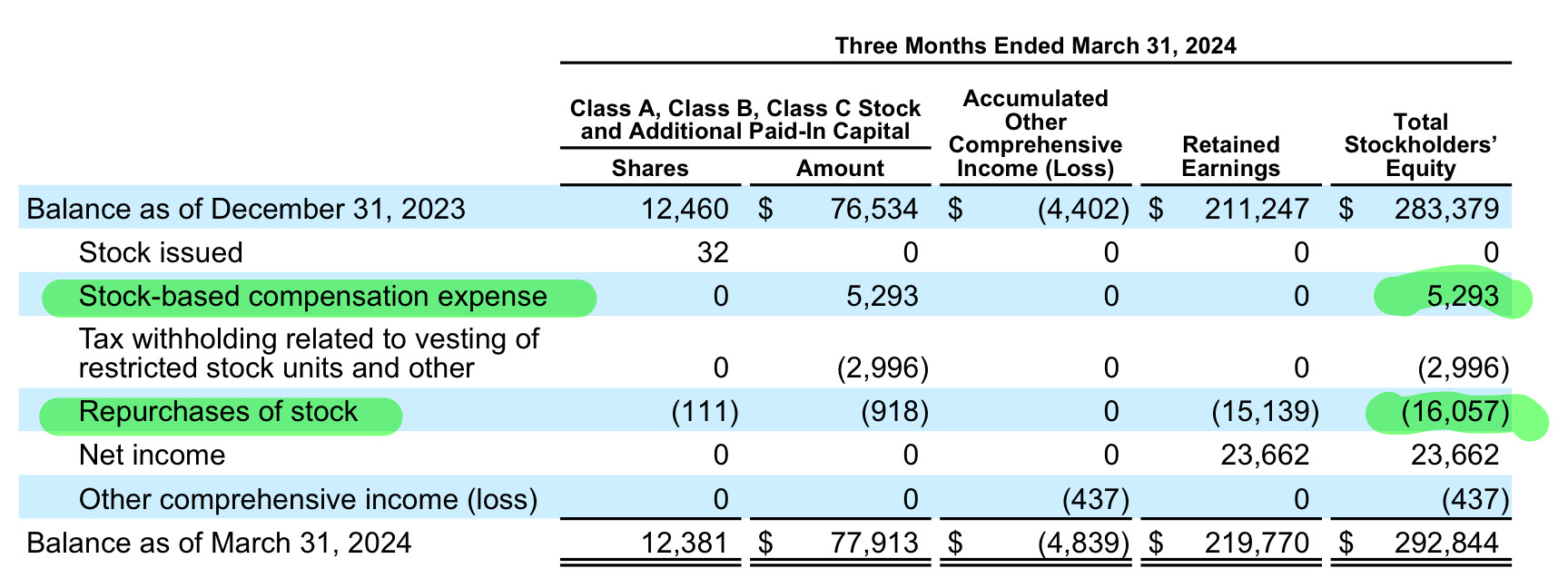

Alphabet's share-based compensation (SBC) has been increasing annually, reflecting the company's reliance on stock awards to attract and retain talent. For the years ended December 31, 2021, 2022, and 2023, the total SBC expense was $15.7 billion, $19.5 billion, and $22.1 billion, respectively. This trend highlights Alphabet's significant use of stock-based compensation, which, while beneficial for employee retention and motivation, contributes to shareholder dilution.

While Alphabet's stock repurchase program might appear to be a strong commitment to returning value to shareholders, it's essential to recognize that a substantial part of these buybacks is effectively neutralizing the dilution from stock-based compensation.

In the first quarter of 2024, nearly one-third of the stock-based compensation expense offset the impact of stock repurchases. As an investor, I am concerned that Alphabet is allocating a significant portion of its free cash flow to stock repurchases that merely counteract the dilution from stock-based compensation. This approach diminishes the potential value added to shareholders through these buybacks.

Employee numbers

Over the past few years, Alphabet Inc. has seen a significant increase in its number of employees. In January 2023, Alphabet announced a significant workforce reduction initiative, targeting a reduction of approximately 12,000 roles. This decision was part of a broader effort to re-engineer the company's cost base and optimize its operational efficiency. The company expected to incur employee severance and related charges between $1.9 billion and $2.3 billion, the majority of which were recognized in the first quarter of 2023.

However, these workforce reductions and cost optimization strategies come with immediate financial impacts, primarily through severance and exit charges, which the company needs to balance against its long-term strategic goals and operational efficiency. At least it seems to be somehow successful, reducing the headcount from 191k in Q1 2023 to about 181k now.

From an ethical standpoint, it is undeniably sad when people lose their jobs. However, from an investor's perspective, it is crucial to question the necessity of such a large workforce at Alphabet and scrutinize how efficiently their work time is being utilized.

AI race

Alphabet is heavily investing in AI infrastructure and research, positioning itself as a leader in the AI race. The company is integrating AI capabilities into an increasing number of its products. However, it currently appears that their offerings lag behind the models developed by OpenAI and Microsoft. Despite this, I believe that in the midterm, Alphabet's models will improve significantly and become valuable tools. Nonetheless, it remains challenging to predict the actual financial benefits and returns from these substantial investments at this time.

“The significant year-on-year growth in CapEx in recent quarters reflects our confidence in the opportunities offered by AI across our business.”

Wiz Acquisition

Alphabet is in advanced negotiations to acquire the cybersecurity start-up Wiz for $23 billion, as reported by the Wall Street Journal. This would mark the largest acquisition in Google's history, surpassing the $12.5 billion spent on Motorola's mobile division in 2012.

Founded in 2020, Wiz develops popular cloud security software and has grown rapidly, reaching $100 million in annual revenue within 18 months. The company is now aiming for $1 billion in annual revenue and recently raised $1 billion from investors, valuing it at $12 billion.

Google's move to acquire Wiz is seen as a strategic play to strengthen its position in the cloud market, where it currently holds an 11% market share, trailing behind Amazon Web Services at 31% and Microsoft Azure at 25%. Wiz's technology and rapid growth could provide Google with a significant boost in this competitive sector.

Wiz has 950 employees and serves major clients, including nearly half of the Fortune 500 companies in the US. The company's headquarters and sales operations are based in New York, with technology development in Israel.

This is even more interesting given the recent crashes caused by Crowdstrike's update problem.

Stock valuation

Base Case Assumptions

In my valuation model, I assume that Alphabet's ad services will continue to contribute significantly to its revenue growth and profits. Additionally, I anticipate that the Google Cloud business will become increasingly profitable over time. However, I do not expect any substantial contributions from the "Other Bets" segment within the five-year planning period of the DCF model.

Revenue Growth

In the DCF Model, a five-year detailed planning period is used, projecting a 9.7% Compound Annual Growth Rate (CAGR). This trajectory anticipates Alphabets revenue to reach 505 billion in FY 2028.

EBIT Margin

In the last twelve months, Alphabets EBIT margin was 30.5%. For the DCF Model, I have normalized this margin to an average of 28.4%.

Normalized Net Income Margin

Based on the EBIT margin, the Last Twelve Months (LTM) Normalized Net Income margin stands at 25.9%. Moving forward, it is estimated to stabilize around 23.4%.

Free Cash Flow

My Free Cash Flow assumptions include a Net Capex ratio as a percentage of sales (Net Capex = Capex - Depreciation) of 7.1%, reflecting the average of recent years. Working Capital, expressed as a percentage of sales, is determined by the average Working Capital over the past years, calculated at 6.3% of net sales. The Free Cash Flow estimation does not adjust for stock-based compensation. This results into a normalized free cash flow margin of about 17%.

WACC

The Weighted Average Cost of Capital (WACC) is set at 8.0%.

Results

Based on these assumptions, Alphabets equity value is estimated at $1,563 billion. Dividing this by the current number of shares, we derive a fair value per share of $127. In comparison to its latest stock price of $177 the stock appears still significantly overvalued.

Adjusting the WACC to 8.5% would lower the fair value per share to $114, while a decrease in WACC to 7.5% would increase it to $142 per share.

Scenarios

Bull Case Scenario:

In an optimistic scenario, assuming a CAGR for revenue of 10.1%, an EBIT Margin of 31.5%, and a normalized net income margin of 23.9%, the fair value per share would be $159. In this scenario the stock appears to be also overvalued.

Bear Case Scenario:

Conversely, in a pessimistic scenario with a CAGR for revenue of 7.7%, an EBIT Margin of 26.2%, and a normalized net income margin of 22.9%, the fair value per share would be $125. In this scenario the stock also appears to be overvalued.

P/E and EV/EBIT

To further validate the valuation estimate, let's examine my preferred metrics: forward EV/EBIT and P/E. Considering the five-year historical averages of 19.95x for EV/EBIT and 24.49x for P/E, the current valuation of 19.98x EV/EBIT and 22.88x P/E indicates a fair valuation or even a slight undervaluation.

I believe my DCF model is very conservative. I typically err on the side of caution in my valuation models, aiming to incorporate a sufficient margin of safety. Even my bull case appears somewhat conservative compared to market expectations. From my perspective, I would conclude that the stock is currently overpriced.

Conclusion

Alphabet is one of the greatest businesses ever founded. I believe the company will continue to thrive for a long time due to its market leadership position in the internet.

Although the company's financials and substantial competitive moat clearly indicate a "buy," the greatest risk in investing is overpaying. Even for an outstanding business like Alphabet, it is possible to pay too much.

Thank you once again for being here and for your interest! If you enjoyed my analysis, please consider leaving a "like" and subscribing. Your support means a lot!

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is invested in this stock.

Great breakdown! Learned a lot from this!