#66 Uber Technologies

Are the chances greater than the risks?

Dear Readers,

Thank you for being here and showing interest in my work! Your support means the world to me. If you enjoyed this article and would like to see more, please consider subscribing and giving it a like—it really helps grow our community of investors. Thank you for your continued support!

Please read the disclaimer at the end of this article. This is not an investment advice!

About Uber Technologies

Uber Technologies, Inc., commonly known as Uber, is a global leader in mobility services, offering ridesharing, food delivery through Uber Eats, and freight logistics via Uber Freight. Headquartered in San Francisco, California, the company operates in over 70 countries and has become one of the most recognized brands in the tech and transportation industries. Uber’s mission is to create reliable, affordable, and scalable solutions to help people and goods move more efficiently.

Uber was founded in 2009 by Garrett Camp and Travis Kalanick, with the idea born from a simple frustration: the difficulty of finding a taxi. The concept came to Camp during a trip to Paris in 2008, where he envisioned a service that could connect passengers to available drivers via a smartphone app. After returning to the United States, Camp invested $250,000 of his own money to develop a prototype for what was initially called UberCab.

Camp teamed up with Kalanick, a seasoned entrepreneur who had previously sold his startup, Red Swoosh, for $19 million. While Camp was the visionary behind Uber’s original concept, Kalanick played a crucial role in scaling the business, leveraging his operational expertise to drive Uber’s rapid global expansion. Together, they launched UberCab as a luxury black car service in San Francisco in 2010. The service was met with immediate success, prompting the team to rebrand as Uber in 2011 and broaden their offerings beyond high-end rides.

Garrett Camp, a Canadian entrepreneur, brought a background in innovation and tech, having previously co-founded StumbleUpon, a popular web discovery platform. Known for his low-profile approach, Camp focused on product strategy and development, shaping the core of Uber’s technology. Travis Kalanick, on the other hand, became the public face of Uber. With a reputation for aggressive leadership and ambition, Kalanick drove Uber’s expansion into new markets and its entry into industries like food delivery and logistics. Despite his significant contributions, Kalanick’s tenure as CEO was marred by controversies over workplace culture and business practices, leading to his resignation in 2017.

Together, Camp and Kalanick laid the foundation for a company that has transformed transportation and logistics worldwide. Today, Uber continues to innovate and expand, offering a range of services that cater to millions of customers and businesses globally. Its journey from a simple idea to a multinational corporation highlights the power of technology and vision in reshaping traditional industries.

History

Uber Technologies, Inc. has grown from a small startup to a global leader in mobility services, encompassing ridesharing, food delivery, and freight logistics. Founded in 2009 by Garrett Camp and Travis Kalanick, Uber began with the simple idea of revolutionizing urban transportation by using technology to connect passengers with available drivers. This idea emerged during a trip to Paris in 2008, where Camp struggled to find a taxi. Back in San Francisco, he teamed up with Kalanick to create a platform initially called UberCab, which launched in 2010 as a luxury black car service. The service gained quick popularity due to its convenience and cashless payment system, prompting the company to rebrand as Uber in 2011.

From its early days, Uber expanded rapidly in the ridesharing market. It started in major U.S. cities like New York and Chicago and went international in 2012, launching in Paris. UberX, introduced in 2012, marked a turning point by offering affordable rides in regular cars, making the platform accessible to a wider audience. Over time, Uber added services like UberPool for shared rides, Uber Black for luxury options, and UberXL for larger groups. The company’s proprietary algorithms for dynamic pricing and ride matching were key to its success, ensuring efficient operations and scalability in urban markets.

In 2014, Uber ventured into food delivery with UberFRESH in Los Angeles, later rebranding it as Uber Eats in 2015. Leveraging Uber’s existing driver network and logistics platform, Uber Eats quickly expanded globally, partnering with local restaurants and global chains like McDonald’s. By 2018, it had become a major revenue driver for the company, especially during periods of reduced ridesharing demand. The service introduced innovative features like live order tracking and exclusive restaurant partnerships, solidifying its position as a leading food delivery platform.

In 2017, Uber entered the logistics market with the launch of Uber Freight, applying its technology to connect shippers with carriers in the trucking industry. The segment grew steadily, expanding to Europe in 2019 and gaining a significant boost with the acquisition of Transplace in 2021, enhancing Uber’s freight management capabilities.

Despite its rapid growth, Uber faced challenges. In 2017, leadership controversies led to the resignation of Travis Kalanick, who was replaced by Dara Khosrowshahi. Under Khosrowshahi’s leadership, Uber focused on improving its public image and governance while navigating regulatory battles worldwide, particularly over driver classification as independent contractors versus employees. These challenges were compounded by intense competition from regional players like Lyft in the U.S., Grab in Southeast Asia, Didi in China, and Bolt in Europe.

Uber went public in 2019 with one of the largest IPOs in tech history. However, its debut was overshadowed by investor skepticism about its path to profitability. The COVID-19 pandemic in 2020 further disrupted Uber’s core ridesharing business, causing a sharp decline in demand. However, the pandemic boosted food delivery, and Uber Eats became a critical revenue driver during this period.

To recover and grow, Uber diversified its offerings, introducing grocery and alcohol delivery, convenience store partnerships, and subscription plans like Uber One, which bundled benefits across its services. Strategic acquisitions, such as Postmates in 2020, consolidated Uber’s position in the food delivery market. The company also invested heavily in operational efficiency, reducing costs by divesting non-core ventures like autonomous vehicles and flying taxis.

In 2023, Uber achieved its first annual operating profit of $1.1 billion, marking a significant milestone. This profitability was driven by increased demand for rides as pandemic restrictions eased, continued growth in Uber Eats, and enhanced cost efficiency. Uber’s use of dynamic pricing, its diversified revenue streams, and investments in advertising and subscription models contributed to its success.

Uber’s journey reflects relentless innovation and adaptation. From its origins as a luxury car service in San Francisco, it has grown into a global platform operating in over 70 countries and offering a range of mobility and delivery solutions. Despite regulatory challenges, leadership changes, and intense competition, Uber has transformed the way people and goods move, solidifying its position as a leader in the mobility and delivery industries.

Business Model

Uber operates on a platform-based business model that connects service providers (drivers, couriers, and restaurants) with customers seeking rides, food delivery, or freight transportation. This asset-light model allows Uber to operate without owning the vehicles or inventory used to provide its services, focusing instead on acting as an intermediary. The model relies heavily on technology, dynamic pricing, and a global network to maintain scalability, efficiency, and customer satisfaction.

At its core, Uber’s platform facilitates transactions between users and service providers. In ridesharing, passengers use the Uber app to request rides, which are fulfilled by independent drivers who use their own vehicles. Similarly, in food delivery through Uber Eats, customers place orders from participating restaurants, and couriers deliver the meals to their doorsteps. For logistics, Uber Freight connects shippers with carriers for freight transportation.

A significant strength of Uber's business model is its dynamic pricing mechanism, often referred to as surge pricing. This algorithm adjusts fares based on supply and demand in real time. During high-demand periods, such as peak hours or inclement weather, prices increase, incentivizing more drivers to come online while managing customer demand. This feature ensures service availability but has also drawn criticism for steep price hikes during emergencies.

Uber generates revenue through service fees charged on each transaction. For ridesharing, this fee is typically a percentage of the fare paid by the rider, with the rest going to the driver. In Uber Eats, the company charges both restaurants and customers for its services, collecting delivery fees and a commission on each order. In Uber Freight, the company earns a margin by matching carriers with shippers, though its profitability in this segment is more challenging due to tighter competition and operational costs.

The model is supported by advanced technology. Uber’s app integrates machine learning algorithms for efficient ride and delivery matching, real-time tracking for customers, and data analytics to improve route optimization. This technology-driven approach reduces inefficiencies and enhances the user experience. The company also leverages its data to predict demand patterns, optimize driver allocation, and fine-tune pricing strategies.

Another cornerstone of Uber's business model is its scalability. Since it does not own the core assets like cars or delivery vehicles, Uber can quickly expand to new markets with minimal capital investment. This asset-light strategy also reduces the risks associated with owning and maintaining physical assets. However, it depends heavily on a reliable network of independent drivers and couriers, which exposes the company to regulatory risks regarding worker classification. Legal battles over whether these service providers should be classified as independent contractors or employees pose a significant threat to Uber’s cost structure and profitability.

Uber has diversified its revenue streams beyond ridesharing and food delivery to mitigate risks and capture new market opportunities. It offers premium ride options like Uber Black for higher-end customers, Uber Pool for cost-conscious riders, and subscription plans like Uber One, which bundle benefits across its services. The company has also entered adjacent markets, including grocery and alcohol delivery, micro-mobility (bike and scooter rentals), and logistics through Uber Freight.

Despite its innovative model, Uber operates in highly competitive and cost-intensive markets. Margins are thin, particularly in food delivery, where competition is fierce, and promotional discounts are common. The company’s success depends on its ability to maintain a balance between user affordability, driver satisfaction, and operational efficiency.

Scalability

Uber’s business model is inherently scalable, driven by its platform-based approach, advanced technology, and asset-light strategy. Unlike traditional transportation companies, Uber does not own the vehicles used for ridesharing, food delivery, or freight logistics. Instead, it acts as an intermediary, connecting users with service providers—drivers, couriers, and carriers—via its mobile app. This allows Uber to expand rapidly into new markets with minimal upfront investment.

One of the key factors enabling Uber’s scalability is its reliance on technology. Uber’s platform is built on advanced algorithms and machine learning, which optimize ride matching, pricing, and route efficiency in real time. For example, its dynamic pricing mechanism adjusts fares based on demand and supply, ensuring availability while maximizing revenue. These features make it easier for Uber to handle increased demand during peak times or in high-density areas without needing to invest in additional physical infrastructure.

Uber’s scalability is further amplified by its network effects. As more users join the platform, more drivers are attracted to meet the demand, creating a positive feedback loop. This cycle strengthens Uber’s position in existing markets and accelerates its growth in new ones. Additionally, Uber leverages its global presence to deploy standardized technology and processes across diverse regions, making it highly adaptable to different market conditions.

The company’s diversified service offerings also contribute to its scalability. Uber has expanded beyond ridesharing to include food delivery through Uber Eats, freight logistics with Uber Freight, and even grocery and alcohol delivery in some regions. These services often use the same core infrastructure, such as the driver network and logistics platform, allowing Uber to enter new sectors without significant additional costs.

However, scalability does present challenges. Uber’s reliance on independent contractors means it must continuously attract and retain a large pool of drivers and couriers. In regions where driver supply is constrained, service availability and scalability can be impacted. Additionally, regulatory hurdles, such as debates over driver classification as employees versus contractors, can increase costs and limit Uber’s ability to scale in certain markets.

Despite these challenges, Uber’s asset-light model and technology-driven operations ensure that it can rapidly adapt to changing demands and expand its services efficiently. By integrating multiple offerings under one platform and leveraging data to optimize operations, Uber has demonstrated a unique ability to scale its business while maintaining a focus on innovation and customer experience. This scalability remains a cornerstone of Uber’s long-term strategy, positioning it as a leader in the mobility and delivery industries worldwide.

Market Position

Uber is one of the largest and most influential companies in the global mobility market, encompassing ridesharing, food delivery, and freight logistics. Its market position and popularity are shaped by its innovative business model, global reach, and ability to adapt to diverse customer needs. However, the company also faces significant challenges from competition, regulation, and market dynamics.

In ridesharing, Uber holds the title of the largest platform in the world, operating in over 70 countries and more than 10,000 cities. It commands approximately 70% of the U.S. ridesharing market, where its closest competitor, Lyft, holds most of the remaining share. Globally, Uber captures around 25% of the ridesharing market, with competition from regional players like Bolt in Europe, Didi in China, and Grab in Southeast Asia. Despite this competition, Uber's brand recognition is strong, and in many parts of the world, the name "Uber" has become synonymous with ridesharing.

In food delivery, Uber Eats has become one of the largest platforms globally, rivaling DoorDash, Grubhub, and regional competitors like Deliveroo and Zomato. In the U.S., Uber Eats holds a significant market share, second only to DoorDash, which dominates over 50% of the market. Internationally, Uber Eats has a strong presence in Europe, Australia, and parts of Latin America. This segment has grown rapidly, especially during the COVID-19 pandemic when delivery services became essential, and it now accounts for more than 40% of Uber’s total revenue.

Uber Freight, the company's logistics arm, connects shippers with carriers and has also seen significant growth, particularly in the U.S. While it is a substantial player in the freight brokerage market, it faces tough competition from established firms like C.H. Robinson and Convoy. In 2023, Uber Freight generated over $5 billion in revenue, although it continues to face profitability challenges due to market fluctuations.

Uber’s popularity is driven by several factors. The company’s app is user-friendly and integrates multiple services, from ridesharing to food delivery and package logistics. Its existing driver network and logistics technology ensure reliable and efficient service. Innovations like Uber Pool, Uber Black, and Uber Reserve cater to various customer needs, while loyalty programs like Uber Rewards and Uber One enhance customer retention. Additionally, Uber’s brand recognition and global availability make it a reliable choice for users worldwide, particularly international travelers.

Regional variations in popularity reflect local market dynamics. In North America, Uber is the clear leader in both ridesharing and food delivery. In Europe, it competes with players like Bolt and local taxi services, adapting its model to meet regulatory demands in countries like Spain and the Netherlands. In Asia, Uber has a strong presence in countries like India and Japan but faces stiff competition from Grab and Ola. Although Uber exited China in 2016 by selling its operations to Didi, it retains a stake in the company. In Latin America, Uber dominates markets like Mexico and Brazil but contends with competitors such as Cabify. In the Middle East and Africa, cities like Cairo, Dubai, and Johannesburg have shown growing demand for Uber’s services.

However, Uber’s market position is not without challenges. The company faces intense competition from both regional giants and local players. Regulatory pressure is a significant hurdle, particularly regarding driver classification and labor laws. Safety concerns and criticisms over data privacy and driver treatment have also impacted its public perception. Moreover, Uber’s services are discretionary and sensitive to economic downturns, which can reduce demand during periods of lower consumer spending.

Despite these challenges, Uber retains several competitive advantages. Its vast driver and customer network creates efficiency and reliability, while its ability to integrate multiple services under one platform strengthens its ecosystem. The company also invests heavily in innovation, including autonomous vehicles and sustainability initiatives, which could position it for long-term success.

In summary, Uber is a dominant force in the global mobility market, leading in ridesharing and maintaining a strong presence in food delivery and logistics. Its popularity stems from convenience, brand recognition, and its ability to adapt to local and global market conditions. While challenges from competition, regulation, and public perception remain, Uber’s innovative approach and strategic investments ensure its continued relevance and influence in the industry.

Risk of being an employer

One of the most significant risks to Uber’s business model is the potential reclassification of its drivers from independent contractors to employees. This issue strikes at the heart of Uber's operating structure and has far-reaching financial, operational, and strategic implications. The company's asset-light model relies on drivers being classified as contractors, allowing Uber to avoid expenses associated with employee benefits such as health insurance, paid leave, retirement contributions, and payroll taxes. If drivers were reclassified as employees, Uber's costs could increase dramatically, threatening its profitability and scalability.

Uber has long maintained that its drivers are independent contractors. This classification provides drivers with flexibility to set their own schedules, work for multiple platforms, and choose when and where to work. However, critics argue that this flexibility comes at the expense of fair pay, job security, and access to benefits. Labor advocates and governments worldwide have pushed for drivers to be classified as employees, which would entitle them to benefits and protections under employment laws.

If drivers were reclassified, Uber would face substantial financial burdens, including:

Employee Benefits: Health insurance, paid time off, and unemployment insurance.

Payroll Taxes: Contributions to Social Security, Medicare, and other mandatory taxes.

Administrative Costs: Additional resources required to manage driver schedules, compliance, and human resources.

Minimum Wage and Overtime Compliance: Ensuring all drivers receive minimum wage and overtime pay, even during periods of low demand.

Court Decisions and Legal Developments

The debate over driver classification has played out in courts and legislatures across the globe, with notable decisions in several jurisdictions:

United Kingdom (2021):

The UK Supreme Court ruled that Uber drivers should be classified as "workers," a category that sits between contractors and employees. This ruling entitled drivers to benefits such as minimum wage, holiday pay, and pensions, though it stopped short of granting full employee status. Uber subsequently adjusted its operations in the UK to comply with the ruling.

California, USA (2019–2021):

California passed Assembly Bill 5 (AB5) in 2019, which tightened the rules for classifying workers as contractors. Under AB5, Uber drivers would likely be classified as employees.

Uber and other gig economy companies sponsored Proposition 22, a ballot measure exempting them from AB5. Proposition 22 passed in 2020, allowing Uber to maintain contractor status for drivers in California while providing limited benefits. However, a California court later ruled Proposition 22 unconstitutional, and the case remains under appeal.

Netherlands (2021):

A Dutch court ruled that Uber drivers are employees under Dutch labor laws and are entitled to the same protections as taxi drivers. The ruling required Uber to pay compensation for failing to comply with employment laws.

Spain (2021):

The Spanish Supreme Court ruled that gig economy workers, including Uber Eats couriers, are employees. This decision prompted Uber to adjust its operations in Spain, including offering employment contracts in some cases.

These rulings highlight the regulatory and legal uncertainty Uber faces globally. In some regions, the company has been forced to adapt its business model, while in others, it continues to challenge unfavorable decisions.

Financial Preparation for Worst-Case Scenarios

Uber has proactively taken steps to mitigate the financial impact of potential driver reclassification:

Legal Contingency Funds:

Uber sets aside reserves in its financial statements to cover potential liabilities arising from lawsuits and legal settlements. These funds provide a buffer against unexpected costs.

Cost Management:

The company has streamlined its operations, reducing expenses in non-core areas and focusing on efficiency. Divestments, such as selling its autonomous vehicle division, have helped Uber concentrate resources on its core businesses.

Dynamic Pricing Adjustments:

Uber’s ability to implement dynamic pricing allows it to pass some increased costs onto customers. In the event of reclassification, ride and delivery prices could be raised to offset additional labor expenses.

Diversification of Revenue Streams:

By expanding into adjacent markets like food delivery (Uber Eats), logistics (Uber Freight), and grocery delivery, Uber has reduced its dependence on ridesharing, which is most vulnerable to reclassification risks.

Lobbying and Legislative Advocacy:

Uber has invested heavily in lobbying efforts to influence labor laws. For example, the company spent over $200 million campaigning for Proposition 22 in California, the most expensive ballot measure campaign in U.S. history.

Global Adaptation Strategy:

In markets where reclassification becomes unavoidable, Uber has shown flexibility by introducing hybrid models that provide some benefits while maintaining as much operational flexibility as possible.

Worst-Case Financial Implications

Analysts estimate that a widespread reclassification of drivers could increase Uber’s costs by 20–30% globally. For example, in the U.S. alone, this could translate into an additional $500 million to $1 billion annually. If similar rules were implemented globally, Uber’s annual costs could rise by $2–3 billion. These expenses would likely erode Uber’s thin profit margins and potentially push the company back into significant losses after only recently achieving its first annual profit in 2023.

The risk of driver reclassification represents one of the most significant challenges to Uber’s business model. While the company has prepared financially through contingency funds, cost optimization, and diversification, the potential for increased costs and regulatory compliance remains a serious threat. Court decisions in key markets like the UK, California, and the Netherlands have forced Uber to adapt, but the ongoing legal battles and regulatory uncertainties make this an enduring risk. To sustain its operations and profitability, Uber will need to navigate these challenges with strategic flexibility, financial discipline, and continued innovation.

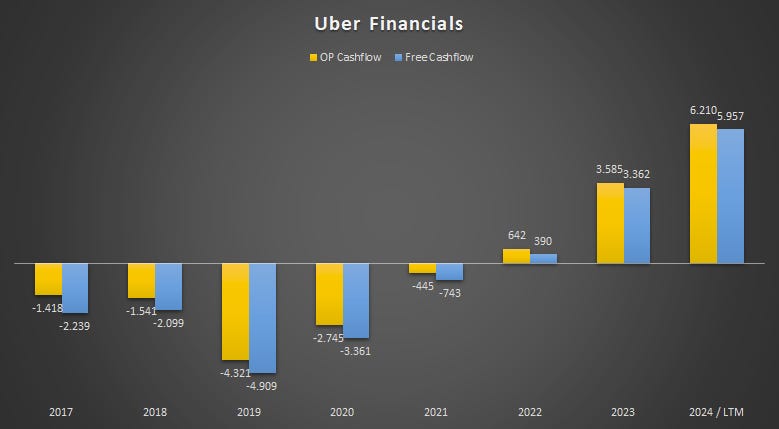

Key financials

Uber has achieved impressive growth in net sales, with a compound annual growth rate (CAGR) of nearly 27% since 2017, showcasing a robust growth trajectory. Although the company reported negative operating and net income until 2022, Uber turned profitable in 2023 and has been steadily increasing its profits since then, marking a significant milestone in its financial performance.

Uber has demonstrated strong cash flow generation since 2022, solidifying its position as a robust cash generator. Over the past twelve months, the company has produced nearly $6 billion in free cash flow. Since free cash flow closely aligns with operating cash flow, this performance highlights Uber’s asset-light business model, which requires minimal capital expenditures (CapEx) to sustain its operations and growth. This efficiency underscores the scalability and financial resilience of Uber's business approach.

Since 2023, Uber has achieved profitability, marked by positive operating and net margins, as well as improvements in key financial metrics like Return on Invested Capital (ROIC) and Return on Assets (ROA). Additionally, the company maintains a low Net Debt-to-EBITDA ratio, and its interest obligations are well-covered, reflecting a strong and stable financial position.

Segment Financials

The Mobility segment is the largest contributor to net sales in 2024, accounting for 57% of total revenue, followed by the Delivery segment with 31% and the Freight segment with 16%. The majority of Uber's revenue is generated in the U.S. and Canada, with the EMEA region (Europe, Middle East, and Africa) ranking as the second-largest revenue source.

When it comes to profitability, Uber primarily reports an "Adjusted EBITDA" metric, which, while not my preferred measure of profitability, is the only one available to assess the performance of each segment. Currently, the Mobility segment, mirroring its dominance in net sales, contributes the largest share, accounting for 73% of Uber's total Segment Adjusted EBITDA, with a margin of 26%. The Delivery segment shows a margin of 17%, demonstrating solid profitability, while the Freight segment remains in a loss-making position, highlighting ongoing challenges in this area.

Stock Valuation

Base Case Assumptions

The base case assumes that Uber will maintain its position as the dominant ridesharing company, continuing to expand into new markets. While the previously mentioned risk of being required to classify drivers as employees is unlikely to fully materialize, I believe that in some countries or specific situations, Uber may need to adjust its model to provide drivers with basic employment rights. This would likely create some margin pressure, but I do not foresee a worst-case scenario where Uber's entire business model is fundamentally disrupted.

In my projections, I have not factored in autonomous driving or other future technologies due to the high level of uncertainty surrounding their development and adoption. However, Uber’s platform scalability remains a key strength, allowing the company to improve margins over time despite potential challenges. This scalability, combined with its established global presence and operational efficiency, supports the long-term sustainability of its business model.

Revenue Growth

In the DCF Model, a five-year detailed planning period is used, projecting a 10.1% Compound Annual Growth Rate (CAGR). This trajectory anticipates Uber‘s revenue to reach about $67 billion in FY 2029.

Normalized Net Income Margin

I project a normalized net income margin of approximately 10.8% over the next twelve months, with a gradual improvement to 11.8% over time. Once this level is reached, I expect the margin to stabilize, reflecting a mature and efficient operational model.

Free Cash Flow

My Free Cash Flow assumptions are based on a Net Capex ratio (Net Capex = Capex - Depreciation) of 1% of sales, consistent with the average of recent years and reflective of Uber's asset-light model. Working Capital, expressed as a percentage of sales, is derived from the historical average, calculated at 17.8% of net sales. The Free Cash Flow estimate does not account for adjustments related to stock-based compensation. These assumptions result in a normalized Free Cash Flow margin of approximately 13.9%, highlighting Uber’s strong cash generation capabilities.

WACC

The Weighted Average Cost of Capital (WACC) is set at 8.0%.

Results

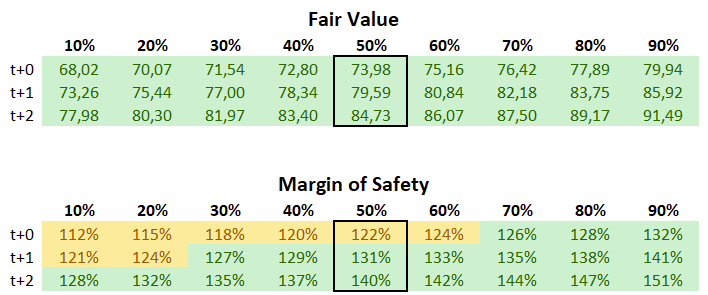

Based on these assumptions, Ubers’s equity value is estimated at $156 billion. Dividing this by the current number of shares, we derive a fair value per share of $74. In comparison to its latest stock price of $61 the stock appears undervalued.

Adjusting the WACC to 8.5% would lower the fair value per share to $67, while a decrease in WACC to 7.5% would increase it to $84 per share.

Scenarios

In the two tables below, I present my estimated fair values for the stock under three key scenarios: baseline, bear case, and bull case, providing a range for comparison. These estimates are derived from my Discounted Cash Flow (DCF) valuation, reflecting varying assumptions about growth rates, margins, and other key factors.

The baseline scenario corresponds to the 50% column, representing the most likely outcome. The 90% confidence interval represents the bull case, while the 10% confidence interval reflects the bear case, with intermediate scenarios filling the remaining columns. This framework offers a comprehensive view of potential outcomes based on different assumptions.

The second table presents the margin of safety, calculated as the ratio of the estimated fair value to the current share price. To make this more visually intuitive:

Margins of safety above 125% are highlighted in green, indicating that the stock meets my personal margin of safety threshold.

Margins between 100% and 125% are marked yellow, suggesting a moderate level of safety.

Margins below 100% indicate potential overvaluation and are marked red.

This approach provides a clear and systematic way to evaluate the stock's fair value and its attractiveness based on risk-adjusted scenarios.

Conclusion

Uber Technologies, Inc. stands as a global leader in the mobility, food delivery, and logistics sectors, with a proven track record of growth and innovation. Over the years, the company has transformed transportation and logistics through its asset-light, technology-driven business model, achieving significant scalability and efficiency. Since turning profitable in 2023, Uber has continued to strengthen its financial position, delivering robust cash flow and improving key metrics like operating margins, ROA, and ROIC.

While regulatory risks, such as the potential reclassification of drivers as employees, remain a concern, Uber has demonstrated its ability to adapt by diversifying revenue streams, managing costs, and leveraging its global platform. The likelihood of a full-scale reclassification appears low, though some margin pressure may arise from adjustments in specific markets. However, Uber’s scalability and operational efficiency should enable it to maintain profitability and improve margins over the long term.

From a valuation perspective, my analysis suggests that Uber’s stock is currently undervalued, with a fair value estimate of $74 per share based on a DCF model. Even under varying assumptions for growth rates, margins, and discount rates, the stock offers a margin of safety, particularly in the base and bull case scenarios. This reflects the company’s strong fundamentals and the resilience of its business model.

In summary, Uber’s dominant market position, scalable platform, and ongoing profitability improvements make it an attractive investment. While challenges persist, the company’s ability to innovate, adapt, and generate cash flow underscores its potential for long-term growth and shareholder value creation.

Thank you once again for being here and for your interest! If you enjoyed my analysis, please consider leaving a "like" and subscribing. Your support means a lot!

Disclaimer: The information provided in this publication is for educational and informational purposes only and does not constitute financial advice. The content is solely reflective of my personal views and opinions based on my research and is not intended to be used as a basis for investment decisions. While every effort is made to ensure that the information is accurate and up-to-date, the writer makes no representations as to the accuracy, completeness, suitability, or validity of any information in this post and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All readers are advised to conduct their own independent research or consult a professional financial advisor before making any investment decisions. The author is not invested in the mentioned stock.

Great piece, thank you for sharing! One note about legal contingencies. Although Uber adjusted its operations subsequent to UK ruling, Uber has a dispute with UK tax authorities regarding the application of VAT.

Based om the 10-Q disclosure: "As of March 14, 2022, we modified our operating model in the UK, such that as of that date Uber UK is a merchant of transportation and is required to remit VAT. Uber UK is remitting VAT under the Value Added (Tour Operators) Order 1987 (“VAT Order 1987”), which allows for VAT remittance on a calculated margin, rather than on Gross Bookings. We have received multiple assessments from the HMRC disputing our application of VAT Order 1987 for the period of March 2022 to March 2024, totaling approximately $1.4 billion (£1.1 billion) for unpaid VAT."

Uber did not record a contingency for this dispute. Moreover, in order to appeal Uber had to pay the assessment and recorded this payment as other receivable. If Uber loses the appeal, they will have to reverse the receivable and record the loss through the P&L. Francine McKenna and I wrote about this:

https://deepquarry.substack.com/p/what-do-numbers-tell-us-about-ubers